Editor’s Note: Community Finance Brief is a weekly newsletter from Matt Posner of Court Street Group, occasionally syndicated on ImpactAlpha.

Democratizing access to homeownership has the potential to offer a path to financial stability for millions of people. Despite considerable progress in consumer finance since the 2008 financial crisis, mortgage finance remains elusive to most low-to-moderate income Americans.

In this brief, we advocate for the introduction of Community Benefit Bonds – a form of impact securitization for mortgage assistance programs. These bonds would be supported by careful underwriting standards to ensure that low- to moderate-income individuals and other underserved prospective homeowners are the primary beneficiaries. Additionally, they could incorporate data-driven evaluation frameworks assessing broad social impact on the communities where these homes are situated. This approach emphasizes market-driven solutions rather than subsidized ones.

Credit, in its fundamental essence, facilitates the acquisition of goods without the immediate requirement of cash. This principle permeates all facets of contemporary economies and constitutes a pivotal element in housing finance within the United States. However, the existing framework for homeownership fails to adequately extend credit to individuals most in need of access. Lenders’ preferences are influenced by actuarial considerations, as discerned from credit patterns which indicate that specific segments of our communities either lack the capacity or exhibit reluctance to make timely payments. This observation finds support in delinquency data. Nevertheless, there is a growing assertion nationwide that certain segments of our communities possess the reliability to manage lines of credit effectively but lack the initial capital required for home down payments. This suggests inefficiencies in risk allocation within the market. Often, these segments correspond to individuals of minority ethnicity or those situated within the LMI strata of our economy.

Publicly-supported Mortgage Assistance Programs, or MAPs, have long proven that, if fully funded, can support those in the most need of access to affordable homes. And while these programs have grown under the Biden Administration, they are still limited in scope and mostly tied to annual appropriations of government bodies in this country. As a result, they exist at the fringes of the real estate industry. Further, so-called affordable lending programs by government-sponsored enterprises, or GSEs, are beginning to show that underwriting standards that mitigate down payment requirements are starting to have an impact, yet they still account for roughly 1% of all loans underwritten.

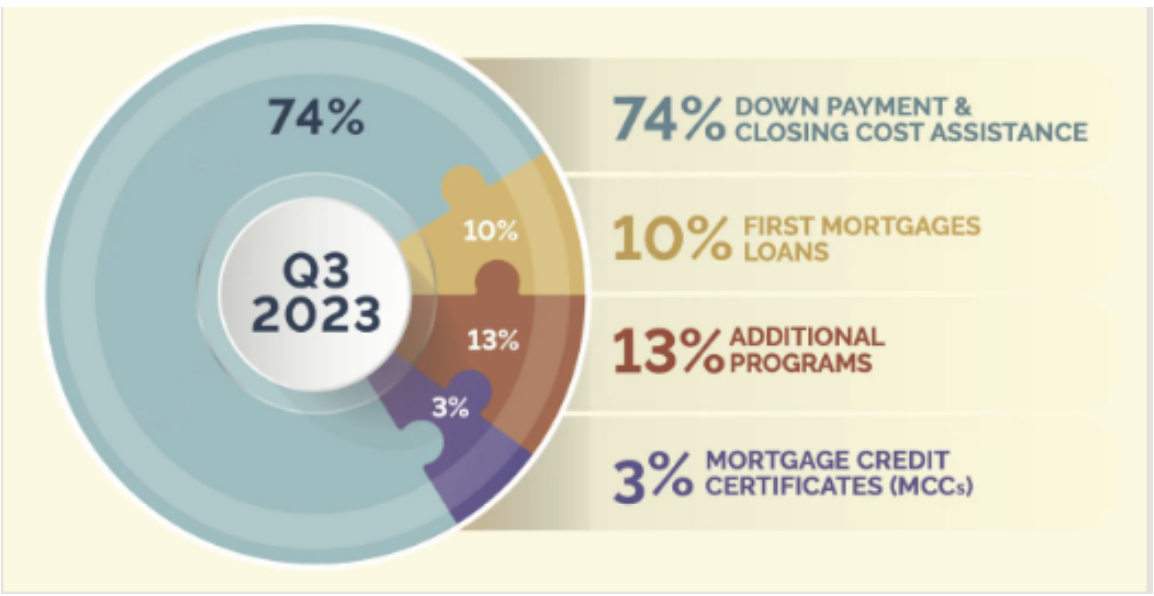

Community Development Finance Institutions, or CDFIs, are at a moment in time where concepts that have laid dormant after the 2008 financial crisis are proving that with proper diligence can cross homeownership hurdles. As discussed last week, City First Enterprises are actively facilitating support for low-to-moderate-income families through initiatives such as down payment assistance and secondary mortgage structures. These interventions effectively address liquidity challenges faced by aspiring homeowners.

Securitization, i.e., market forces, could help catapult these hitherto experimental concepts from the margins to the mainstream of the real estate industry and potentially into millions of homes. Community Benefit Bonds, or MAP bonds, make a compelling case to be considered impact securities. The target demographic for these financial instruments and the desired outcomes align closely with the criteria sought by impact investors. While additional research is warranted, initial evidence suggests that combining an underserved segment of the consumer finance realm with the increasing demand for impact asset classes could yield transformative outcomes.

Public programs and municipal bonds

Federal, state- and local-housing finance agencies have long led the way in supporting marginalized people in gaining access to assistance in owning homes. MAPs offer financial assistance to homebuyers who are struggling to come up with the funds needed for a down payment and come in various forms such as grants, forgivable loans, deferred payments loans or matching savings plans. These public programs are made more available to first-time home buyers, low-income families or limited to certain geographies.

Data consistently shows that these programs equate to reduced delinquencies and foreclosures. A 2023 National Low Income Housing Coalition report looked specifically at homeownership rates in areas of higher participation of public MAPs and found homeownership was higher for longer periods of time when public programs were consistently active in a community. Research by the National Council of State Housing Agencies consistently shows correlations between ownership and funding levels.

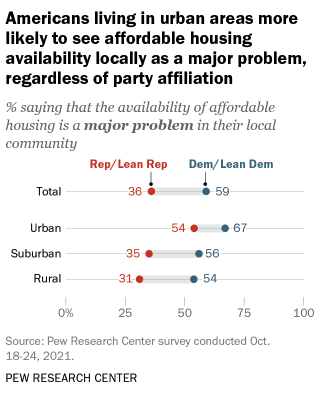

With that said, funding is consistently inconsistent. With the data not centrally located, we can look to federal government engagement as a proxy via the U.S. Department of Housing and Urban Development wherein only 1 in 4 eligible households receive financial housing assistance. At the state and local level, we can point to budget shortfalls, challenging home inventory, rising interest rates or challenges with applying tax credits as any of the number of issues that make efficiency within these organizations difficult (and underscore a need for better private solutions). The result of funding challenges is clear: 85% of respondents to a 2022 Pew poll said housing was a problem in their community (49% said it was a ‘major’ problem).

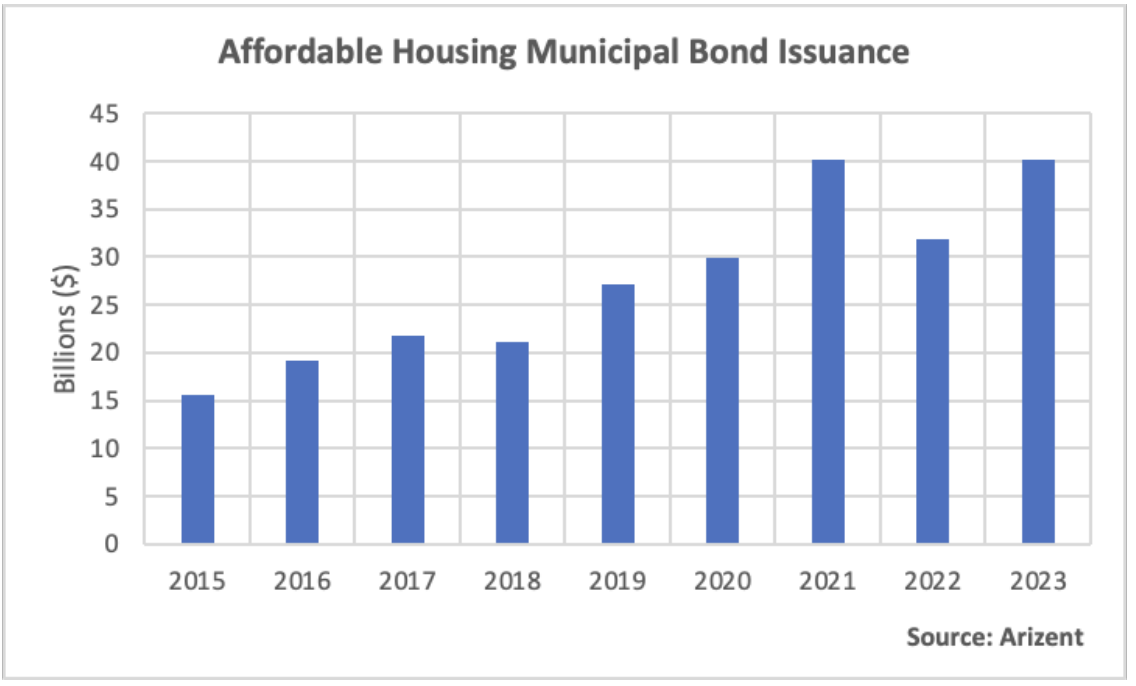

At the state and local level, municipal bonds are issued to support housing finance agencies to the tune of roughly $40 billion in 2023. These bonds can have various repayment structures but generally they rely on regular payments to mortgages of which a portion will go towards the bonds but also have state appropriations or dedicated taxes or fees of real estate transactions that can be dedicated to bond repayment. The bonds generally pay for construction of public housing and maintenance, rental assistance and MAPs.

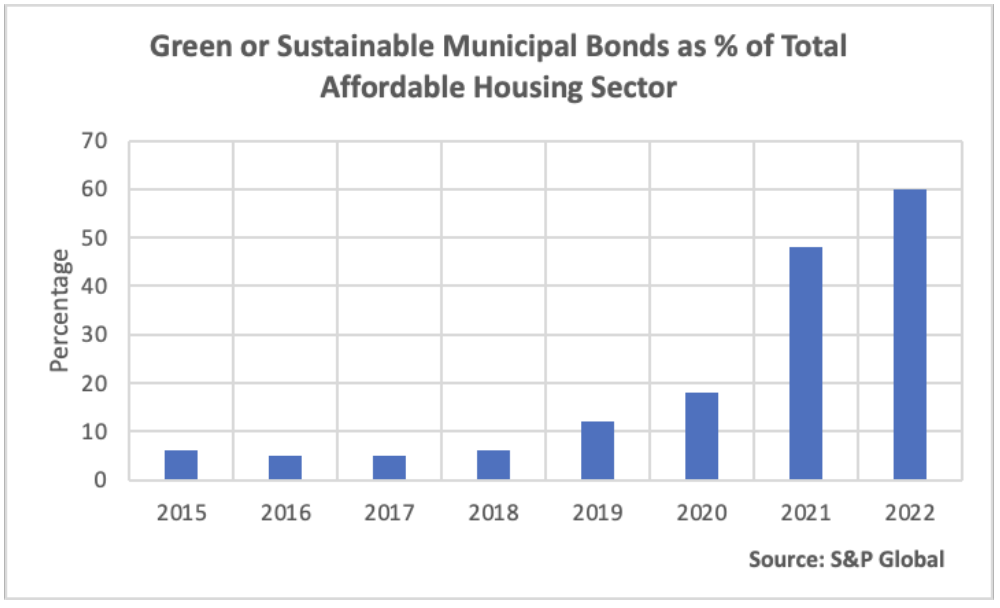

Further of interest is that housing bonds are leading the way as far as being labeled ‘green’ or ‘sustainable’ as state and local governments are marketing their programs to impact investors. Last year, 60% of all housing muni bonds issued were labeled impactful in one way or another. The point here is that a road has begun to be paved for MAP impact bonds, but it is still quite nascent.

With public programs being the primary way in which low-income and racial minority’s access support in homeownership, we would be remiss if we did not note that federal appropriations for affordable housing and community development increased by 34% from 2020 through 2023. Federal legislation under the Biden Administration has not only increased direct grant funding through various channels but has also encouraged the CDFI community to engage in semi-private solutions (they tend to have government or philanthropic support). This has led to the re-emergence of private MAP solutions all over the country.

Mortgage securitization

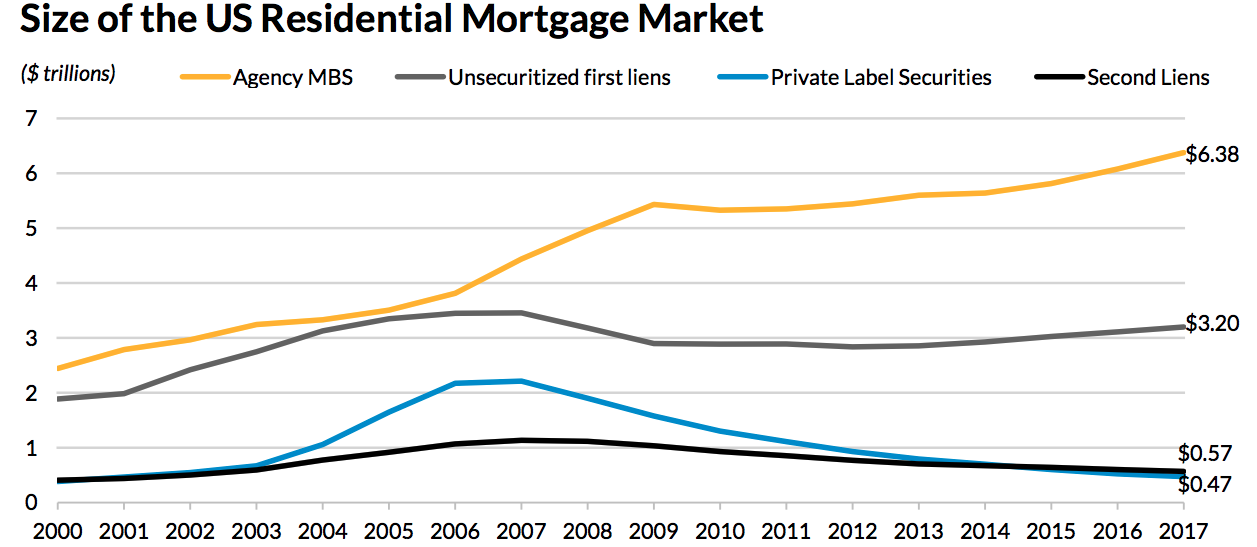

While public programs have consistently offered DPA and secondary mortgage solutions, after the 2008 financial crisis, the landscape shifted considerably. Seen as part of the real estate speculation problem that caused the housing bubble, secondary mortgages, either public or private, halved in size. Fifteen years later, there has been a modest resurgence in these offerings as a result of affordable-lending pilots from GSEs and most recently with the growth of CDFIs that are beginning to prove with more diligence, these are tools that can overcome the liquidity issues that plague LMI/minority homeowners.

Currently, secondary mortgages represent a marginal segment within the expansive landscape of the mortgage market. The principal factor contributing to the limited scale of the secondary mortgage market is the inherent difficulty in securitizing second mortgages, coupled with the absence of scalable enterprise initiatives. To effectuate the securitization process, which involves pooling together second mortgages, investors must exhibit a heightened risk tolerance and a deliberate impact goal, given that the lien does not provide comprehensive coverage for the underlying asset in question.

And with that said, the success of the housing market comes in its ability to scale through securitization, which allows for a much larger segment of our population to own homes. Part of this securitization is a series of standards and guardrails that have created an incredible boon to homeownership in the country since the 1950s. Through the mortgage securities market, individuals have increased access to credit (mortgage-backed securities expand access to mortgage credit), lower interest rates (mortgage-backed securities create a liquid market for mortgages), efficiently distributed risk (it is spread throughout a diverse investor universe) and perpetuated general economic growth as the housing market is linked to economic growth.

Yet, we continue to see major portions of our population left out of these gains in large part because of the challenges of upfront capital. The broad hurdles to a secondary mortgage market are:

- Regulatory constraints: The Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 established stricter regulations for the mortgage market, including limitations on risky lending practices. This has made it more difficult to securitize second mortgages, which are considered riskier than primary mortgages due to their subordinate lien position.

- Heterogeneity: Second mortgages come in a variety of forms, with different interest rates, loan terms, and borrower profiles. This heterogeneity makes it challenging to pool them into standardized securities that are attractive to investors.

- Limited (investor) demand: Institutional investors and bank portfolios, who are the primary buyers of mortgage-backed securities, have historically shown limited interest in second mortgage securities due to their perceived higher risk profile. This lack of demand makes it difficult to create a liquid market for these securities.

- Lack of standardized origination and servicing practices: Unlike the primary mortgage market, there is no established standard for originating and servicing second mortgages. This lack of uniformity makes it difficult to create a robust secondary market for these loans.

- Technological limitations: The technology infrastructure currently used for securitizing primary mortgages may not be readily adaptable to second mortgages, further hindering the development of a secondary market.

Secondary Mortgage (perceived) risk

Risk plays a critical role in hindering the expansion of well-designed secondary mortgage programs. Many worry about the credit risks associated with second mortgages, but there’s evidence to challenge these concerns, especially when borrowers meet strict lending standards. By carefully implementing these programs, we can see the flaws in our current system more clearly. Ongoing research on mortgage payment delays, especially among public housing residents and low-to-moderate-income individuals, highlights the increasing interest in academic and professional circles in exploring the effectiveness of down payment support, improving financial knowledge, and finding better ways to evaluate mortgage-related risks.

According to one study in the Journal of Housing Economics in 2018 examined the experiences of thousands of low-to-moderate-income (LMI) homeowners. It found that those who received assistance with down payments or closing costs repaid their mortgages at the same rate as those who didn’t receive aid. Essentially, helping LMI homebuyers overcome financial barriers and offering various support services showed that these borrowers perform just as well as similar borrowers who didn’t need assistance.

These findings challenge the idea that LMI households must make a substantial down payment to ensure they can consistently pay their mortgages over time. The evidence suggests that providing support for closing costs or mortgage assistance, such as a second mortgage, doesn’t necessarily increase the risk of repayment. Instead, it highlights the obstacles LMI families encounter when trying to become homeowners.

Further, the 2008 financial crisis can serve as an illustration of the paradox of LMI-labeled people compared to the rest of the population. There is no lack of research done on this topic but there are a few interesting themes to consider. First, it is largely documented that the credit boom from 2001 through 2006 was concentrated in the middle- to upper-income portions of our population, indicating that it was real estate speculation that led to the crisis, not a problem of LMI families over-borrowing.

And yes, while LMI do indeed default more than middle- to higher-income families, the role of financial literacy has been shown to have a significant impact on the ability for LMI to continue to stay up to date on mortgage payments. A 2010 Federal Reserve Bank of Atlanta study showed that individuals with the highest numeracy scores on a financial literacy example had foreclosure rates two-thirds lower than those with the lowest scores.

In 2019, the Journal of Economic Psychology examined the existing financial capability programs for public housing residents and found peer-to-peer education, culturally relevant curriculum and partnerships with financial institutions offer “a substantially higher percentage” of long-term on-time payment of rental agreements or mortgages and “significant positive effects” of any attempts at improving financial literacy of residents. The Institute for Research on Poverty quantified mandatory financial education on low-income individuals in a housing voucher program that resulted in improvements in financial behavior, increased savings account balances and increases in FICO scores as a result.

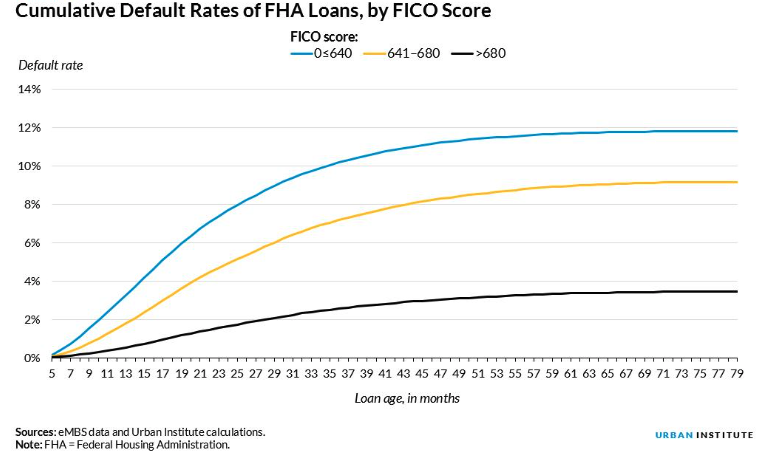

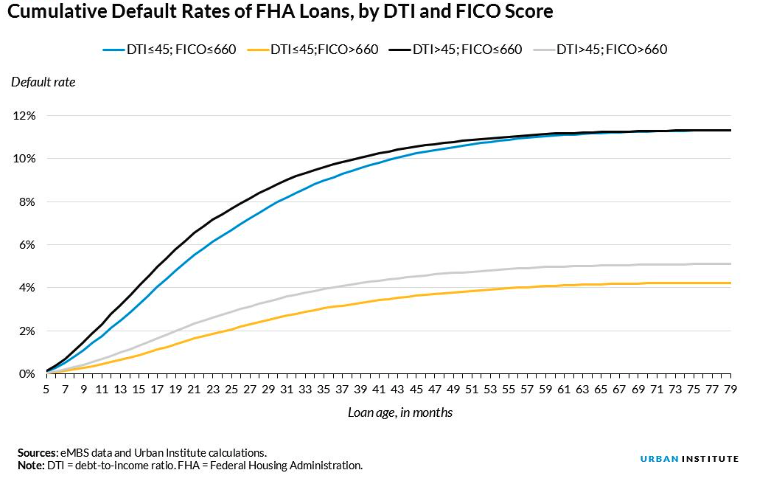

There is growing evidence that alternative methods for assessing creditworthiness can effectively support LMI borrowers and reduce reliance on traditional metrics like FICO score and debt-to-income (DTI) ratios (see figure, above, in regards to inconsistent FICO/DTI assessments and correlations of default risk). It is possible to make bad loans to people who cannot afford to live in these homes but if you can control for income, assess financial literacy and leverage non-traditional assessments such as rental history, other lines of credit, cash flow analysis and bank account data, to name a few, there can very well be a data-driven methodology to find such borrowers. In theory, there are millions of people who could afford to buy homes if such a financial tool were made available to them.

With the right selection process, and an enhanced monitoring and evaluation process for the bonds, such investors would appear. The data demonstrates that risk is more than what a FICO score or DTI ratio tells you.

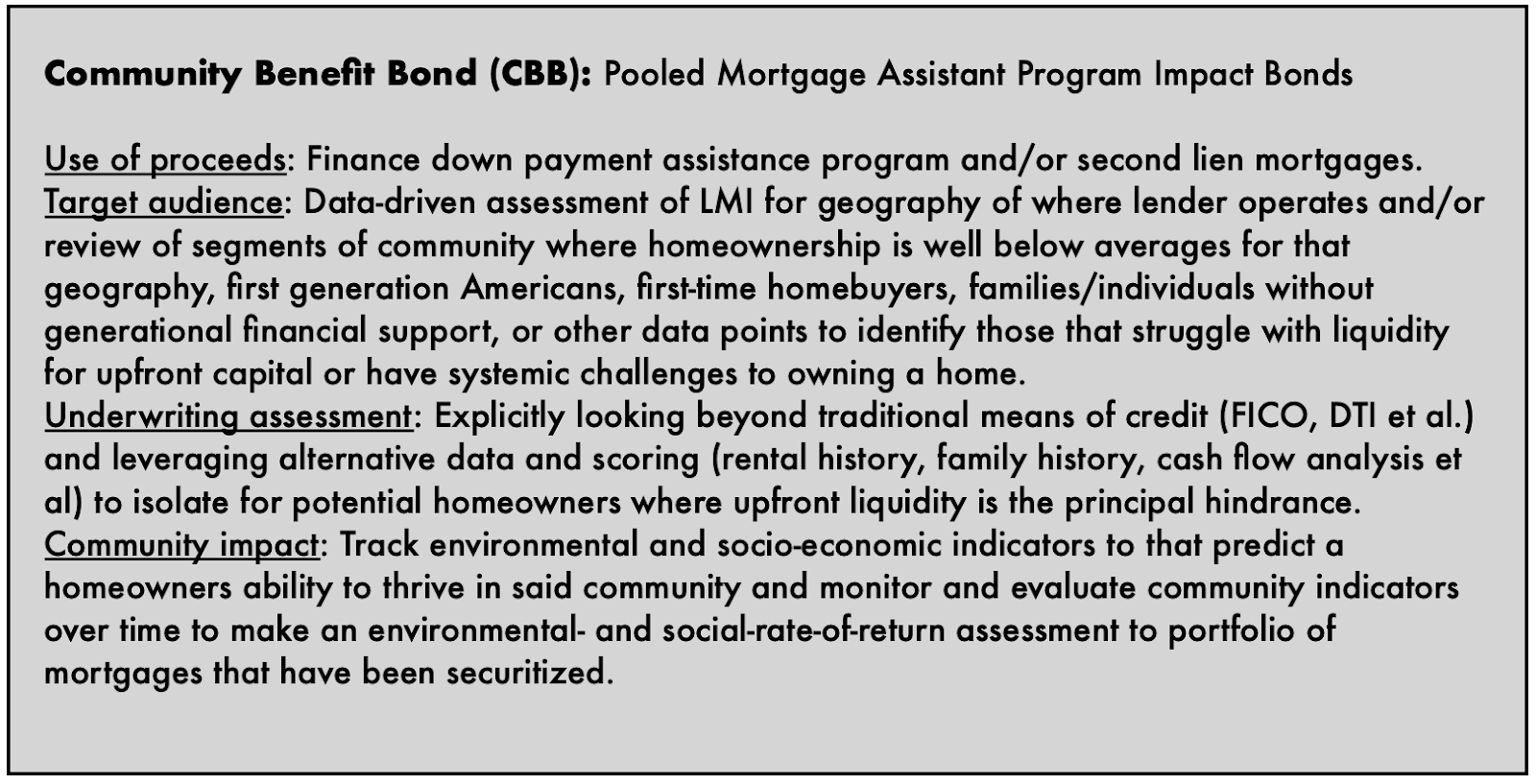

Community benefit bonds

In order to securitize MAPs into an impact security the portfolio of mortgages must: a) be clearly targeting parts of our population that are currently hindered from access to sustainable mortgage terms and b) be able to track in a data-driven way how these mortgages are adding value to a community.

We propose a better review of where affordable lending programs from GSEs are finding success and learning from the now dozens of pilots around the country wherein mostly CDFIs are seeing success in DPA and second lien financial tools to support segments of the population that will in fact, make mortgage lenders whole over the length of loans. Isolating for the right people and tracking how they fare over time through a holistic view on what community means may engage the trillion-dollar impact investment universe around the world.

While generally not a leader when it comes to bond innovation, the municipal bond market has already laid a path for CDFIs and others to follow. In the municipal bond marketplace, green or sustainable muni housing bonds lead the pack. It is not surprising that this would be the case as in these instances, use of proceeds from funds raised are direct and the pursuit of these projects is well within any number of international standards of what can be considered impact. These two elements are the two largest hurdles for impact and municipal securities in general.

Further, default rates for these bonds are tiny compared to other asset classes. In the last five years, there have been zero defaults by any state or local public housing finance agency. Between 1970 through 2022, housing defaults have totaled just $898 million, of which most were student housing projects associated with for-profit universities. These are very high performing mortgage bonds.

With the statistics proving out this can be scaled, the size of these markets are remarkably different. In 2023, the outstanding mortgage-backed agency-issued bond market in the U.S. was 44-times larger than the outstanding housing muni market, according to the Securities Industry and Financial Markets Association (SIFMA). The mortgage bond market in January 2024 saw $35.3 billion issued compared to the $1.7 billion issued the same month in the affordable housing municipal bond space, according to SIFMA and Arizent.

The $40 billion in municipal bonds focused on supporting the lowest socio-economic levels of our society in 2032 is nowhere near close to the size of the mortgage market, but it is still a figure that shows some depth for a potential CBB marketplace.. Given the need, municipal bonds could very well be a starting point for a way in which to offer more secondary mortgage solutions with impact criterion.

There have been several housing muni bond programs that have specifically supported second mortgages or down payment assistance in the Massachusetts Downpayment Assistance Program, the Texas Homeowner Assistance Fund, Florida Housing finance Corporate second mortgage loan program and the New York State Mortgage Agency downpayment assistance program – all of which issue muni bonds to support such efforts.

These are all congruous elements to consider when thinking about the potential for an impact bond focused on providing second mortgages. Their local focus downplays the true potential for scalability.

A new product, a Community Benefit Bond, aimed at scaling mortgage assistance operations could very well be offered to investors. Municipal bonds are novel as a scalable solution, but by no means a necessary facet. A taxable mortgage bond solution could be more palatable given the current rate environment but it would need to be issued with a public purpose in mind.

Key to this process would be the underwriting standards for such a program. Pilots such as that of CFE offer a glimpse of what is possible. If the diligence were in place, the output of information would be enhanced and allow for appropriate monitoring of use of proceeds from securities over time. Impact metrics could focus on the income and racial areas being addressed, but also a focus on location of borrowers would be paramount as this program could be considered a cornerstone for community building.

Scaling solutions with securitization

A new financial product to support a secondary mortgage market with intent is likely in the not too distant future. With pilot programs yielding promising, albeit small in scale, results and funding coming in from government, for-profit and philanthropic interests, the building of a new asset class of securities predicated on MAPs appears to be a likely next step.

Connecting the dots of what these financial products bring to communities, and leveraging data and transparency in the process of delivering them to potential homeowners will be at the heart of its success or failure. The efficacy of the programs should and can be offered to impact investors but those underwriting the loans on the ground floor need to collect better information so as to make a compelling argument for impact at the level for securities investors. Aside from the standard diligence in underwriting with an aim towards LMI and racial minority segments to ensure the products are being used for underserved portions of the community, underwriters should employ a more holistic understanding of the community wherein people are located.

That means tracking environmental considerations (asbestos, lead, proximity to superfund sites or other hazards of location) of where the homes are located. It should also offer information on public education, proximity to healthcare solutions, public transportation, personal economic growth considerations and broader socio-economic means in which to offer a data-driven view of what life in said community looks like. These are all data points that can be tracked over time for an impact investor to better understand their portfolio of mortgages.

These are corners of the marketplace that have not been fully explored and federal subsidies have shown to only work as perpetuating the current model that doesn’t solve for barriers to entry. Thinking outside the box of offering a known tool but to a wider audience could make for real change. Demonstrating the efficacy of such a program by monitoring and evaluating it over time, having robust underwriting processes and engaging community stakeholders will help bridge the income gap when it comes to owning a home in this country.

Matt Posner is principal at Court Street Group. Oswaldo Acosta is CEO and president at City First Enterprises.