To achieve stated climate goals, the U.S. government is embarking on what should be the largest coordination of private and public capital aimed at environmental and social equity in history. This is the vision of the Greenhouse Gas Reduction Fund (GGRF) and already we are witnessing a myriad of innovative ideas come to the fore. But in order for them to flourish, they will need to drive down a road built by bonds. We suggest it be a road that every state and local government, pubic school system, affordable housing organization, power utility, sewer system and healthcare provider already drives on when it needs to go to the bank.

In combating climate change, the focus has often been on the immediate financial resources available, such as the $27 billion allocated to the GGRF. While this sum is substantial, it pales in comparison to the multi-trillion challenge, and opportunity, at hand. The municipal market, with its $4 trillion valuation, emerges not just as a potential solution, but as a critical leverage point for accelerating and scaling up climate initiatives across the country.

The Environmental Protection Agency this week announced the slate of entities that will take on the responsibility of shepherding these dollars into thousands of green projects across the country. This is a significant start, but it represents just a fraction of the investment needed. A green future will require a strategic shift towards larger, more established financial mechanisms and coordinated efforts amongst stakeholders.

The GGRF is structured in a way that emphasizes the local features of smart green investments (read: Community Development Finance Institutions) with an expectation that private capital mobilization will magnify impact into the trillion dollar threshold. To best attain success when it comes to climate goals, a massive shift in behavior, policy, development, construction and capital flows needs to occur. Those with the privilege of managing taxpayer’s’ dollars of the GGRF should consider how to leverage a marketplace that few really understand – and hopefully improve upon how it currently operates.

Bridging gaps

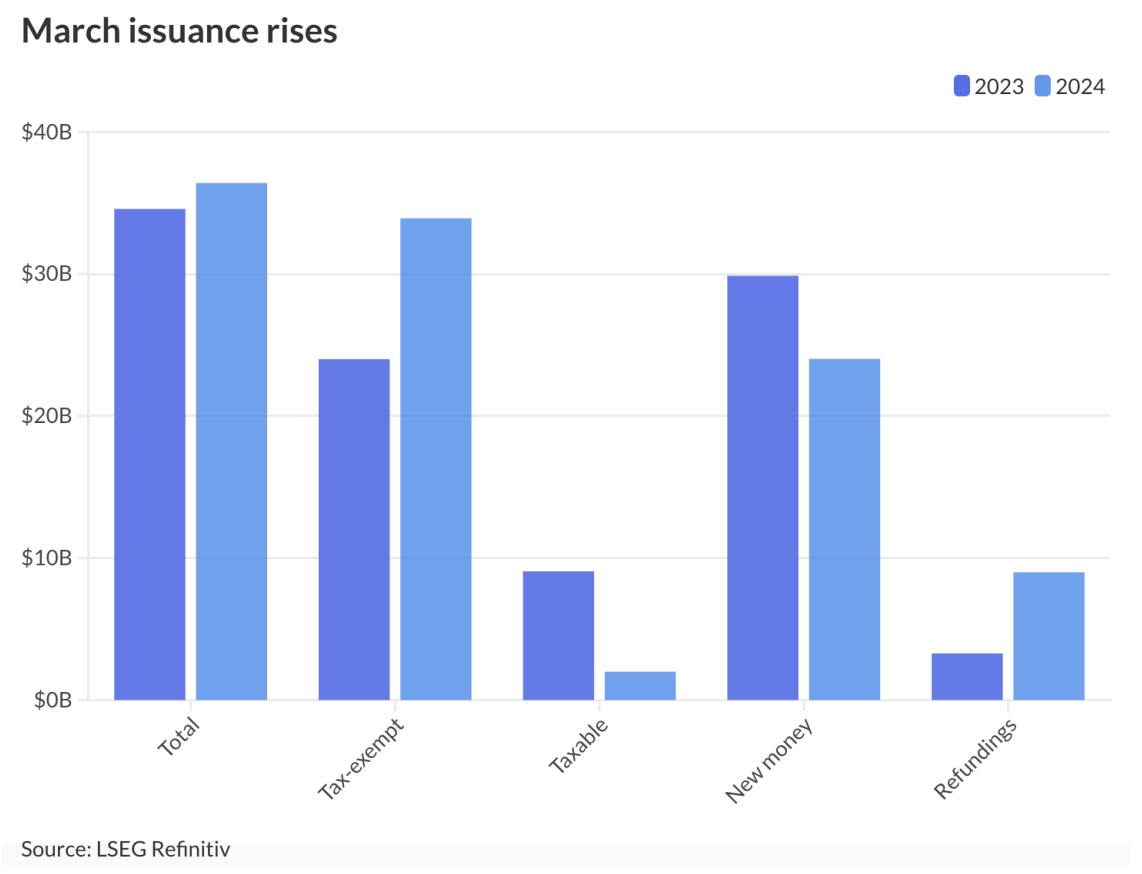

The municipal bond market, historically the backbone of funding for affordable housing, schools, and infrastructure, stands out as a prime candidate for this pivot. If muni’s fund our roads, why not our EV charging infrastructure? If munis fund our schools and affordable housing, why not fund making them greener? They can, with the right investment in funding vehicles, connect together these funding sources to create the necessary leverage for our national green infrastructure challenges. In this sector, $27 billion is less than a month of issuance (see figure below).

A stroll down the lane of what what could be for muniland:

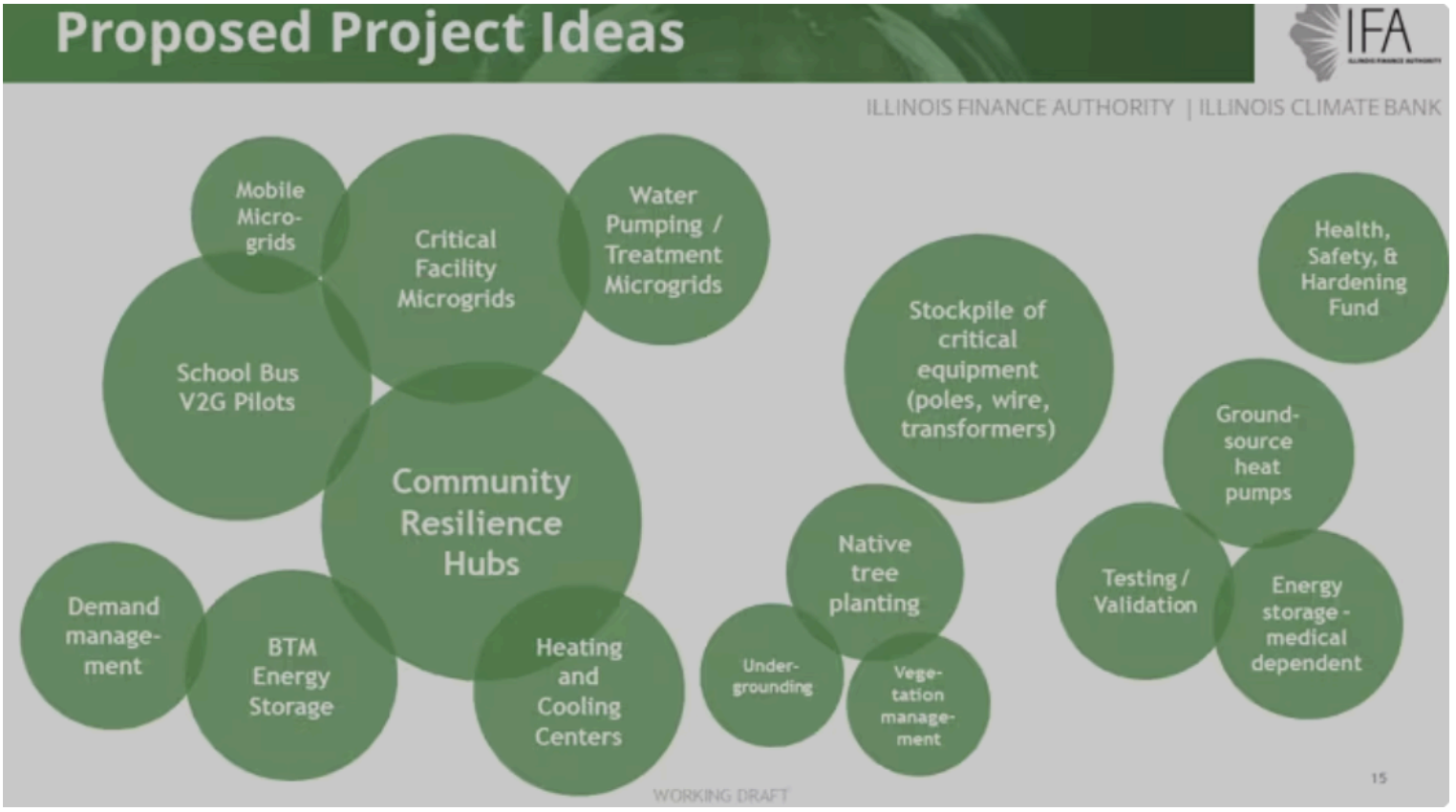

It is expected that in each region, CDFIs will begin to originate green loans in qualified sectors (such as greening buildings, homes and transportation, and developing distributed clean energy). Imagine then, if every CDFI in, say, California or Illinois, went on to sell these loans to the California iBank, Illinois Climate Bank or even CalHFA for affordable housing programs, and then they in turn access the muni market with these streams of income. This would create a massive supply of capital for decarbonization, while allowing those closest to the projects determine what subsidy was needed, rate buy-down, project cost buy-down, etc., while creating a standard methodology for decarbonization.

Or, perhaps a state conduit entity that specializes in K-12 financing – like the Virginia Public School Authority – were to coordinate with GGRF awardees and put together a greening plan for all the local school systems in the state that want to participate. In such an instance, all participating schools could respond to a tailored RFP to indicate where in the green program they match and from there, the conduit would pool these indications into a security to be issued into the muni market.

These examples (of which permutations are plenty) underscore one key takeaway: the critical need for an organized central legal entity to facilitate large-scale green loan programs. Whether a climate bank, bond bank or financing authority of a state or jurisdiction, creating a hub for pooling loans either originating from the top or at the grassroots level, would magnify capital for GGRF eligible projects. This approach offers several advantages:

- Scale: by pooling loans, the state entity can raise much larger sums of capital compared to individual CDFI loans.

- Streamlined and Standardized Process: standardizing the loan application process through a single entity simplifies participation for local projects.

- Expertise: the state/local entity can leverage its existing knowledge of municipal bond issuance and financial management.

- Familiarity: utilizing the established municipal bond market provides a familiar and well-understood financing mechanism for local governments.

Leveraging standards

A crucial first step involves the widespread adoption of standardized underwriting practices within the municipal bond market (perhaps akin to the Trust Indenture Act of 1939). This standardization would enable the creation of novel decarbonization financing structures that seamlessly integrate with the broader fixed income financial ecosystem, encompassing both municipal finance and the mortgage-backed security market.

Like Fannie Mae or Freddie Mac or state housing finance agencies, these entities aggregate standardized loans from diverse originators, facilitating access to the bond markets and securitization channels essential for scaling up investments in renewable energy and energy efficiency initiatives. As such, we need to green existing products we are originating, not create new systems of access to capital. The exciting news about the awarding of GGRF funds is what each of the coalitions brings to the market.

The Coalition for Green Capital serves as an example of an organization attempting addressing these knowledge and financing gaps. By potentially leveraging its substantial resources and established connections with state and local governments, as well as green banks across the nation, the Coalition can play a vital role in facilitating information exchange and bridging the financial chasm faced by municipalities. This collaborative approach is crucial for empowering local governments to harness the necessary leverage within the municipal market.

Same for Climate United, which, among others, brings together Calvert Impact’s with its history of securitization, Community Preservation Corp. and its long track record of originating mortgage-backed securities, and the Vermont Municipal Bond Bank, which has for decades created economies of scale in access to the municipal bond market. Climate United’s close link to scaled capital markets will also let it help create the necessary leverage.

Power Forward Communities, comprised of Rewiring America and its focus on single-family market transformation, Enterprise Community Partners and the Local Initiative Support Corporation, both rated CDFIs, round out the talented group of awardees. Enterprise helped pioneer building efficiency standards through its Enterprise Green Communities Criteria and has guided billions of municipal green affordable housing finance dollars.

Other components in the Greenhouse Gas Reduction Fund, such as the Clean Communities Investment Accelerator and the Solar For All program, also offer opportunities for strategic partnerships that will be better optimized if they take a path that focuses on standardizations. These collaborations would enable the originators to leverage the expertise and market access possessed by the established financial institutions, ensuring necessary leverage and liquidity for the originated loans.

The vast existing network of over 50,000 municipal issuers underscores the potential for leveraging the existing municipal finance infrastructure. Rather than advocating for the creation of additional issuers, the focus should be on establishing a well-organized system for loan origination, program design, and efficient integration with established capital markets. Ultimately, a standardized and streamlined system of origination is paramount to ensuring the long-term success of clean energy community finance initiatives, eliminating the pricing premiums often associated with illiquidity.

The adoption of standardized underwriting practices and working through conduit entities offers a compelling opportunity to unlock vast reserves of private capital within the municipal finance system. With that said, it will require an emphasis on this direction from the federal government. Without it, we may end up with thousands of green, yet siloed projects across the country, not a trillion dollar green wave.

Editor’s Note: Community Finance Brief is a newsletter from Matt Posner of Court Street Group, occasionally syndicated on ImpactAlpha.

Matt Posner is a principal at Court Street Group.

James McIntyre is the chief strategy officer at Inclusive Prosperity Capital.