Investors focused on societal impact are often concerned with corporate treatment of workers.

To assess job quality performance across a portfolio, they generally rely upon environmental, social, and governance (ESG) reporting metrics. Unfortunately, our research has found that current ESG reporting metrics do not capture indicators of whether a company is providing quality jobs. Critical job-related metrics such as the share of employees making a living wage, cost of turnover, or value of benefits are rarely tracked or reported.

Yet, investors, regulators, and the managers themselves rely on that incomplete data to make decisions that have a significant impact on employees, society, and the bottom line.

Sustainable Jobs

A strategy and set of practices to develop what we define as quality, sustainable jobs enables a firm to be profitable while creating value for its employees at all levels, beginning with basic needs (such as living wage), and including higher order needs such as equity, retirement benefits, and career development.

With this definition in mind, we explored which material jobs metrics are tracked and publicly available through six ESG data providers (MSCI, Refinitiv, Sustainalytics, Bloomberg, ESG Book, and DiversIQ). We categorized more than 1,000 metrics or indicators from the social category, although on average, less than 20% of “S” metrics were relevant for assessing sustainable jobs.

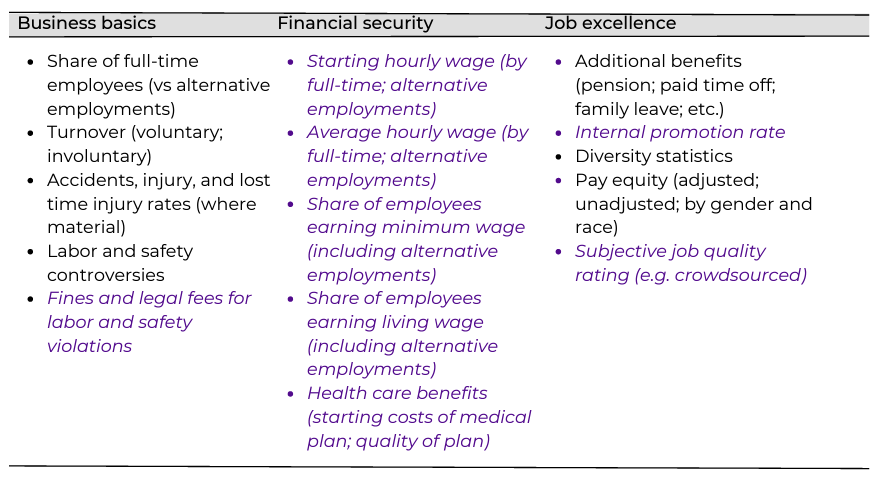

Table 1 contains key metrics across the three job dimensions. Those that are italicized are rarely, if ever, tracked by ESG raters. The rest are available only when companies voluntarily report them. The lack of measures to track wages is a glaring omission. This gap is complicated by the fact that accounting standards in the US do not require reporting on wages, and thus the data is not included in accounting reports.

However, even those metrics that are reliably collected tend to be poorly reported or not reported at all. For example, there is often binary reporting on the existence of a diversity, equity, and inclusion policy (i.e. does the company have a DEO policy), instead of reporting on diverse representation performance. Only half of the S&P 500 report turnover metrics, often without distinguishing between regretted or non-regretted. These insufficient or wholly missing figures make any assessment of quality jobs opaque.

Table 1: Types and Coverage of Quality Jobs Metrics (italics indicate no or limited reporting).

Improving disclosure

There is increasing regulatory scrutiny of corporate reporting on human capital in the European Union and the United States. In the US, most current mandatory human capital disclosures, such as found in Regulation S-K, are principle-based and qualitative, such as a description of human capital resources. There are some exceptions, for example, the CEO pay and median employee pay ratio in the annual proxy statement, or fatalities and violations of mine-safety operations which are quantitative.

Some US agencies require recordkeeping, such as injury and illness incidents, but these records may not be publicly available. While there are new proposals on how to modernize human capital reporting, the latest development is laws that require salary transparency in job posting by some states, most recently New York and California.

Improving disclosure and reporting is important, but needs to be accompanied by a more sophisticated assessment of the financial impacts of current problematic labor practices versus more sustainable practices. Does underpaying fast food workers in an industry that has turnover rates of more than 100% make financial sense when we track the financial impacts of replacing employees just after they have been trained? What about factoring in the negative customer reactions to disgruntled employees? What about the cost of theft by employees who feel undervalued?

On the upside, how much does a company’s positive reputation with workers improve its overall prestige, productivity, and ability to recruit the best employees?

Here are our recommendations for investors:

- Ask standard setters, rating agencies and corporates to track and publish these priority metrics:

- living wage performance;

- regretted and non-regretted turnover; and

- depending on the industry, metrics such as injury rates, % of workers who are outsourced or “contingent,” training investments, benefits package, etc.

- Ask corporates to track and disclose the costs of regretted and un-regretted turnover, including productivity losses, training time, recruiting costs.

- Ask corporates to report on employee related expenditures (wages, benefits, etc) as investments rather than costs with related tracking of financial performance in terms of worker retention and productivity. Also ask corporates to report on wage/benefit equity across race, gender, etc.

More detail on our research can be found in the full report.

______________________________________________________________________________________

Ulrich Atz is a Research Fellow with NYU Stern Center for Sustainable Business. Tensie Whelan is Clinical Professor and Founding Director, NYU Stern Center for Sustainable Business.