ImpactAlpha, April 6 – The municipal bond market has barely begun to grapple with the risks posed by climate change, despite an escalating climate crisis.

Exhibit A: trading of bonds issued by the seven states impacted by the drying up of the Colorado River show no evidence that investors see them as any more risky than bonds in states with more secure water supplies.

The muni market has long been complacent, assuming someone — the federal government, typically — will bail it out, said Thomas Doe of Municipal Market Analytics, or MMA. It’s one thing when dealing with extreme events like hurricanes, wildfires, and floods. But climate change is creating chronic problems, not just singular events, he noted.

“The key for municipal participants is to be aware of this issue,” said Doe. There “may not be time enough to avert the economic and social stresses that are a consequence of the evolving climate.”

Doe’s comments came at a webinar titled “The Southwest Drought and Municipal Implications” produced by MMA. The market and credit analytics provider and its partners have been vocal about their belief that the $4 trillion muni market is largely ignoring climate risk.

State and municipal budgets face increasing strains from climate-change-driven weather extremes, as White House economists point out. That includes ballooning costs for public insurance plans and rebuilding damaged infrastructure, and a decrease in property taxes and other revenues.

“In areas with local declines in tax revenue and rising climate change costs, municipal bankruptcies may be increasingly likely,” notes the report from the Council of Economic Advisors.

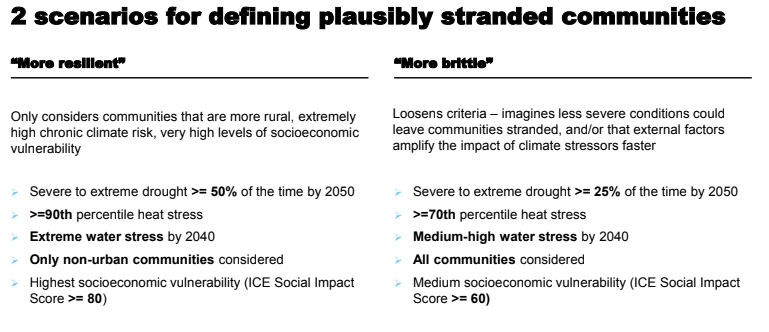

Stranded communities

Climate-driven migration also looms over the muni market. In recent decades, Americans have migrated from high-tax states to low-tax ones, noted Evan Kodra of ICE Data Services. The states that have drawn the most population are often the ones at greatest risk from a changing climate, facing drought, extreme heat, or sea level rise that could make parts of them uninhabitable.

When will climate out-migration begin? Kodra asks. How will those tax bases be stabilized? Will there be stresses to the areas that start to receive climate migrants?

Kodra’s team has developed models for what climate change could look like for the US. In one scenario, much of the Southwest U.S. will be in a drought twice as bad as the current one by 2050. Chronic risks will be uninsurable, he said.

Sources: ICE Data Services,Municipal Market Analytics

What will “stranded” areas look like? Kodra shared two possible scenarios (see chart). In the “more resilient” model, as many as 2.3 million people, and $23 billion of outstanding municipal bonds, would be affected. In a “more brittle” outcome, 63 million people might be at risk, along with as much as $626 billion of debt.

Climate change outcomes will hit marginalized communities hardest, Kodra stressed. Rural communities, for example, face higher costs for water and energy infrastructure, and economically disadvantaged communities can’t borrow their way out of a crisis. There are also knock-on effects, including saltwater intrusion into drinking water, permanent inundation and “sunny day flooding,” power grid failures, dam failures, and more.

Reappraising risk

Credit ratings agencies like Standard & Poors and Moody’s have published general reports about climate risk.

“There hasn’t yet been a headline event that XYZ issuer has been downgraded because of climate risk or because of a lack of disclosure” about some particular risk, said Doe.

Ratings agencies have a critical role to play in focusing the attention of issuers on the benefits of planning for climate change and the risks of failing to do so, said MMA’s Lisa Washburn.

“Just having to answer analysts’ questions on the topic is important,” she said. “As an industry we have to be able to evaluate issuers that are being transparent and those that aren’t.

There are some precedents for the muni market adapting to big issues that require a reappraisal of risk. One example is the public pension crisis of the past two decades. Many state and local governments had enormous pension liabilities, and many weren’t able or willing to communicate the scope of those liabilities to investors or the public.

In 2021, the Government Finance Officers Association, an industry group, issued guidance around how muni issuers should address environmental risks. Left unaddressed were opportunities a changing climate might offer and how are governments taking advantage of them.

“I really would consider it a huge red flag and a statement on the quality of governance if issuers weren’t able to communicate the risks they’re facing on climate change,” said Washburn, “and what they’re doing to mitigate it.”