ImpactAlpha, February 2 – India’s impact investing market has witnessed tremendous growth over the past few years, moving beyond financial inclusion into emerging sectors such as agriculture, technology for good, healthcare, education and livelihoods. But there’s a missing-link in the market: growth-stage capital from impact funds.

The presence of such funds is crucial to sustain the evolution and maturity of the Indian impact investing ecosystem given the growing demand for impact capital in the growth stage and beyond. As impact enterprises mature it is crucial that they remain focused on their core impact thesis and do not alter their business model to one that relegates social impact to an ancillary agenda. The presence of growth stage-focused impact funds can incentivize impact enterprises to minimize their mission drift as they strive to become financially and operationally optimal when scaling up.

Also, on the supply side, large limited partners, both globally and in India, are increasingly interested in credible private sector opportunities that have strong ESG and impact credentials. For impact investors, participating in such opportunities in India can provide a robust foundation for scalable growth with returns thereby creating a strong business case for combining financial upside and social impact.

India’s maturing impact market

Analysis conducted by the Impact Investors Council shows that equity investments in Indian impact enterprises reached an all-time high of $7 billion in 2021. More than $13 billion has been invested over the last three years.

Impact investing dealflow in India has grown across ticket sizes since 2017. The number of later stage impact deals, however, went up by 80%, compared to a 40% increase in the total impact dealflow. Big ticket deals of more than $10 million have more than doubled in the past five years, and the number of deals topping $20 million have increased by a factor of 2.3x.

Clearly, a growing proportion of Indian impact enterprises are now scaling up, creating strong investment demand with a radically different risk-return-impact profile suited for growth-stage funds.

Growth-stage gap

Impact investors have traditionally led funding rounds for early-stage impact enterprises in India, while commercial investors have provided later-stage funding. This model has served the market well so far, but impact funds too can finance the transition of impact enterprises beyond early venture funding.

Specifically, we identify a significant untapped opportunity for impact funders in higher ticket deals of greater than $10 million.

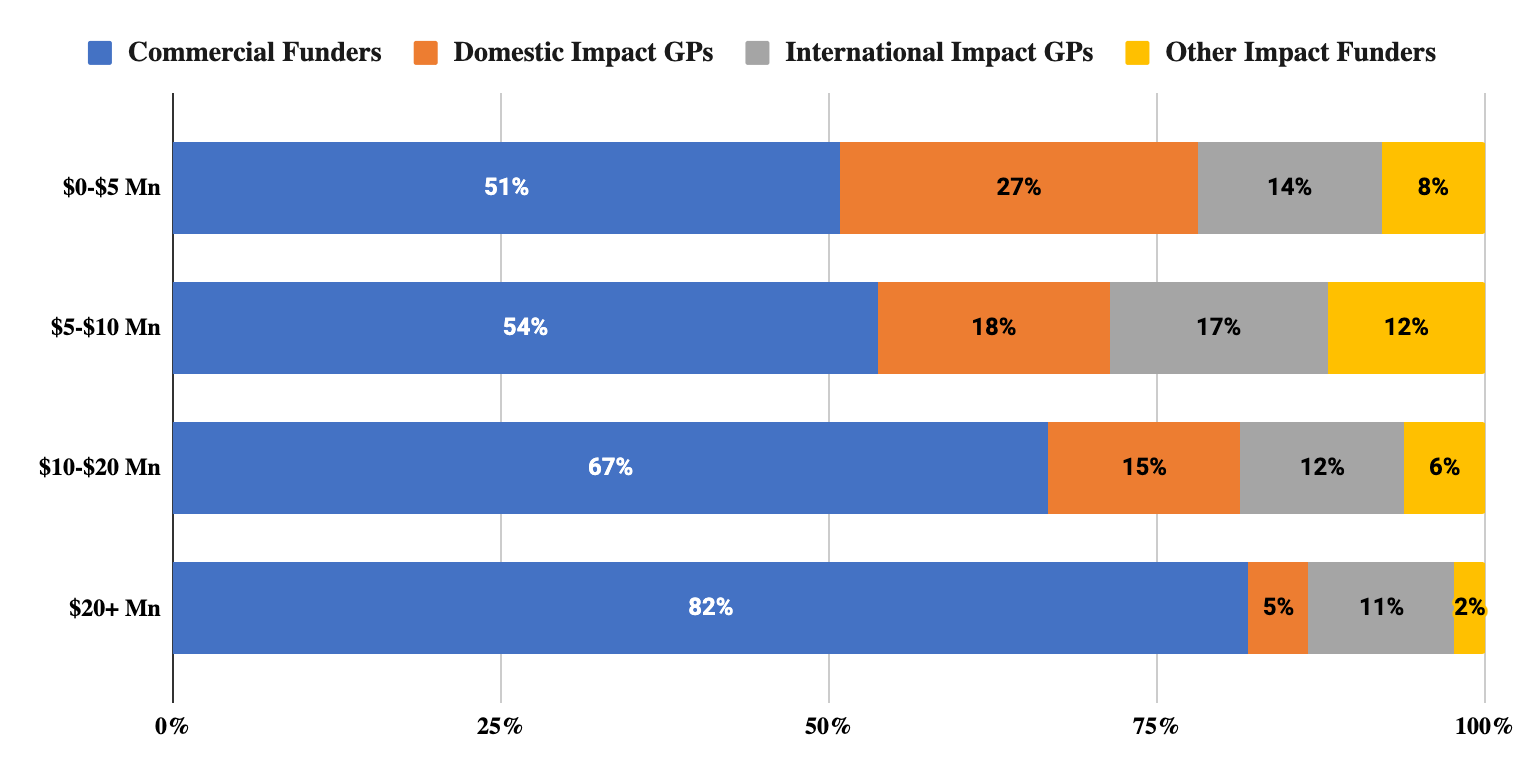

Our analysis of impact deal data in India shows that the share of capital contributed by impact funders falls sharply as the deal size increases. In small-ticket deals, impact investors comprise roughly 50% of total invested capital. In the largest deals – $20 million or more – less than 20% of investment capital comes from pure-play impact investors.

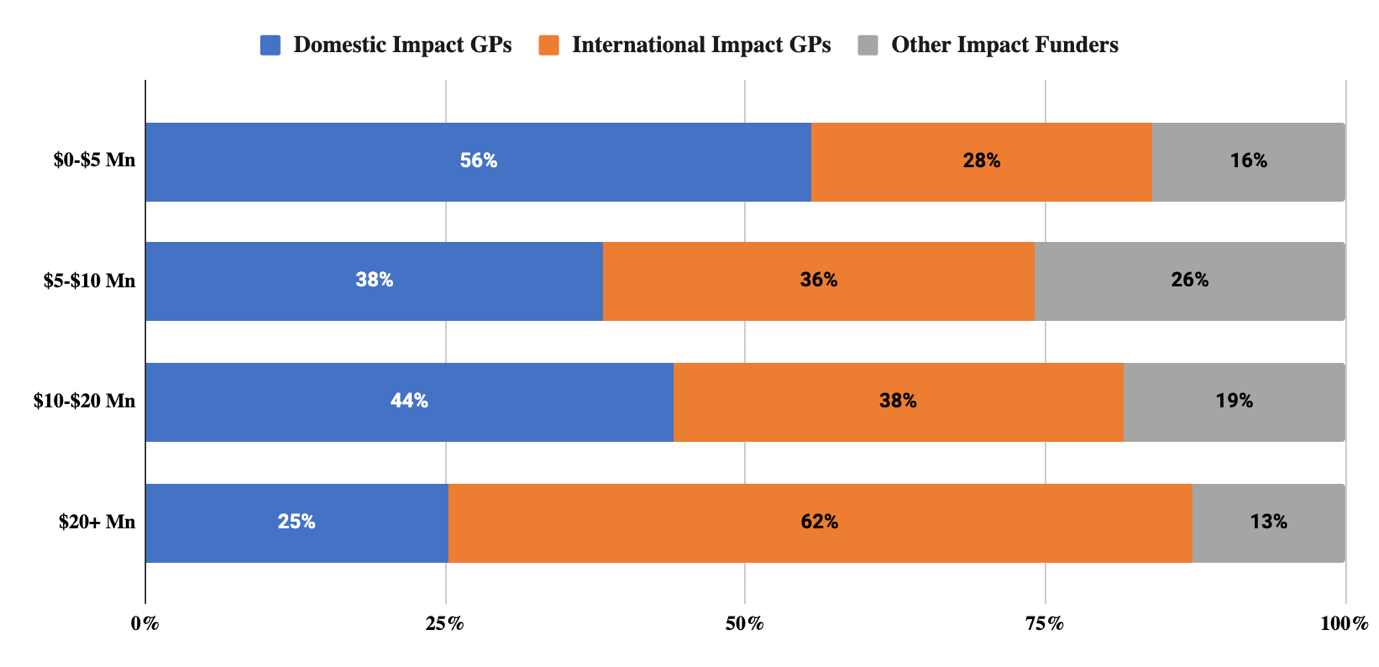

A more granular unpacking of impact investors’ funding reflects another insightful trend: India-based Impact general partners dominate small ticket, early-stage deals, but are present in just 25% of later-stage transactions. The limited impact funding in later stage deals comes from international impact GPs, development finance institutions and other investors.

This trend reflects, in part, the nature of Indian impact GP funding. Most funds are structured as early-stage venture investing platforms, restricting their ability to participate in larger deals. On the flipside, it also demonstrates a sizable market opportunity for investment with respect to growth-stage social enterprises, which are only partially supported by large global impact funds and DFIs. The bulk of the funding is covered by commercial investors.

Seizing the opportunity

Growth-stage companies represent a very different opportunity than early-stage impact enterprises. Their business models are more robust, their capacity to create social impact more proven, thus they are well positioned to provide more predictable financial and social impact performance.

Such companies therefore present an attractive investment case for impact-focused investors including:

- Domestic financial institutions, including commercial banks, financial institutions, alternate investment platforms that have the capacity to fund growth stage impact funds as LPs, or set up growth stage funds as an investment offering for their clients

- Domestic impact funds/GPs that increasingly need to service the financing needs of their maturing portfolio of social enterprises

- International impact/ESG funds that can take advantage of India’s robust and rapidly evolving social innovation ecosystem

- Government of India and large Development Finance Institutions (DFIs) that can set aside specific mandates and allocations for growth and maturing impact companies

India’s equity impact investing market is poised for sustained growth. As the nation looks to spend roughly $170 billion annually to finance the Sustainable Development Goals, the limited public sector resources mean that impact capital providers will have to play a greater role in plugging this funding gap.

India will continue to witness a proliferation of nascent impact enterprises. But with an increasing proportion of such ventures now maturing, the ecosystem requires more growth equity for the scaling up of operations and interventions across the country.

In order to leverage the promising potential of India’s burgeoning and rapidly evolving social innovation landscape, it is imperative to crowd-in asset managers that are able to finance larger impact deals.

Ramraj Pai is the chief executive officer of Impact Investors Council. Vedant Batra is assistant manager, and Rishi Dewan is an intern with the organization.