Just like you can learn a lot about a car by looking under the hood, you can learn a lot about an impact investor’s practices and processes by analyzing their impact management systems.

The Operating Principles for Impact Management (the “Impact Principles”) were introduced in April 2019 to help address the market’s need for a shared set of best practices for impact management. BlueMark was founded a few months later, in January 2020, to meet the market demand for an expert, third-party that could verify impact investors’ alignment with the Impact Principles.

To date, we have completed more than 35 of these impact practice verifications, and recently published our second annual ‘Making the Mark’ report with data and insights based on our first 30 verifications. The full report, “Making the Mark: The Benchmark for Impact Investing Practice,” has more than 40 individual data points on everything from how impact investors are setting impact objectives to how they manage ESG risks in their investment portfolios. By analyzing each data point as part of a larger overall picture, we identified three major themes that show where the impact investing industry is today and what key developments will define the market’s future.

Key Learning #1: Impact investors have work to do to deliver on their good intentions

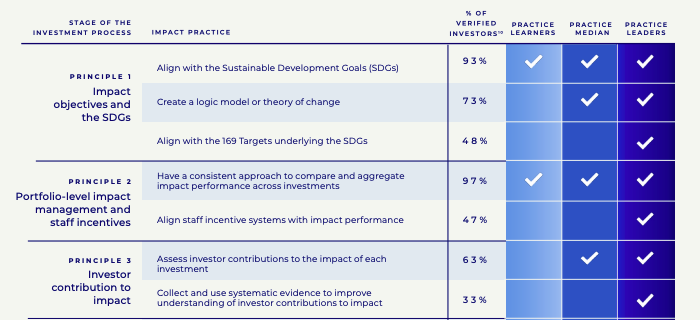

In BlueMark’s inaugural 2020 Making the Mark report, we highlighted that investors’ impact management practices are often less robust at later stages of the investment lifecycle. BlueMark’s first 30 verifications reaffirm this pattern. Impact investors in our sample typically excel at establishing credible strategic impact objectives aligned to the Sustainable Development Goals (SDGs) and at assessing impact at the portfolio level (corresponding to Impact Principles 1 and 2).

Caption: This image provides a snapshot of BlueMark’s Practice Benchmark Dashboard, which shows the key practice indicators associated with Practice Leaders, the Practice Median, and Practice Leaders.

However, while most impact investors evaluate potential (ex ante) impact performance and ESG risks in due diligence and subsequently monitor impact and ESG performance (Principles 3-6), the majority of investors still have room to improve on assessing their contribution to investees’ impact and on following up with investees on impact underperformance, among other areas. Verified investors struggle most to ensure impact endures at and beyond exit (Principle 7) and to consistently adapt their processes based on lessons learned (Principle 8).

Given that impact investing has only emerged as a mainstream investment approach in the last few years, it’s reasonable to expect that some investors may lack experience with the latter stages of the impact investment lifecycle. This should improve as more impact investors become familiar with best practices for many of the more nuanced aspects of impact management.

Key Learning #2: Strengths and challenges vary by investor type

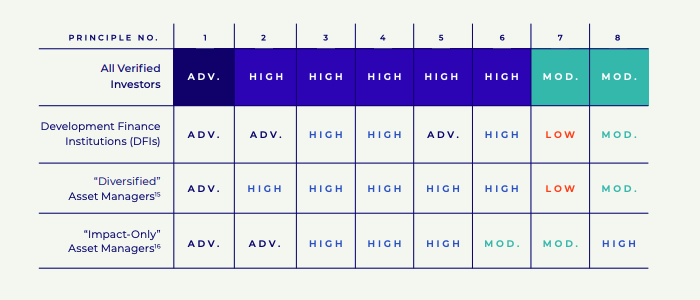

We also found evidence that shows how different investor types have different strengths and areas for improvement when it comes to impact management.

For example, based on our research sample, development finance institutions (DFIs) tend to have more robust ESG risk and performance management systems (Principle 5), while specialized asset managers that invest only in impact strategies often have stronger practices to ensure impact is sustained beyond exit and to apply lessons learned from reviewing impact performance (Principles 7-8). These “impact-only” managers tend to be less consistent in comparing expected and actual impact performance (Principle 6), though, while “diversified” managers pursuing impact as one of multiple investment strategies are less likely to align staff incentive systems with impact performance (Principle 2).

Caption: This chart shows the median rating by impact investor type based on BlueMark’s analysis of investor alignment with the Impact Principles. BlueMark’s proprietary rating system uses a four-party scale (Low, Moderate, High, Advanced), providing a shorthand way for impact investors to assess where in the investment process they excel and where they have room for improvement.

These differences suggest that there are opportunities for impact investors to learn from one another and collaborate in addressing shared challenges.

Key Learning #3: New and smaller managers can be leaders in impact management

The largest (by AUM) and most experienced (by track record) impact investors aren’t necessarily the best.

This finding is based on a regression analysis of BlueMark’s first 30 verifications designed to see if there was any correlation between investor type and overall alignment to the Impact Principles. The results showed that there are no significant correlations between the size of the firm (i.e., overall AUM), the size of the firm’s impact portfolio (i.e., impact AUM), or that firm’s tenure (i.e., years making impact investments) and that firm’s level of alignment with the Impact Principles.

In our experience, neither being a veteran nor a large impact investor equates to having a more sophisticated impact management system. In fact, the opposite may sometimes be true. Newly formed impact investment firms may have the advantage of not having to conform to a legacy investment management system and can instead focus on developing a best-in-class impact management system from the start. Meanwhile, small or niche impact investment firms may have an advantage in being able to better focus on maximizing the impact of a small number of portfolio companies rather than being spread thin trying to manage dozens or even hundreds of companies.

We will reflect back on these key learnings in future research to see how the impact investing market is developing. In the meantime, read the full ‘Making the Mark’ report for additional key takeaways and data points on how impact investors are approaching impact management.

Christina Leijonhufvud is the CEO of BlueMark, Tideline’s new verification business. She manages all aspects of business strategy, new product development, and external relations, and has directly led 30+ impact verification assignments across investor types and asset classes.