Editor’s note: ImpactAlpha contributing editor Imogen Rose-Smith, a longtime senior writer for Institutional Investor, contributes a bi-weekly column on the policies, practices and strategies of the largest asset allocators, including pensions, foundations, and endowments. As Imogen says, she’s “tracking what investors do, not just what they say.”

ImpactAlpha, Aug. 28 – Things are not alright.

The devastating wildfire on Maui is the kind of horrific tragedy the U.S. and Europe experienced in past centuries when infrastructure was shit, health and safety measures minimal or non-existent. Indeed, Maui’s more than 115 wildfire deaths (nearly 400 remain missing) is the most since the 1918 Cloquet fire in Minnesota and Wisconsin killed 453 people.

The Lahaina fire was ready to be sparked when the dry environment combined with the winds of Hurricane Dora. But the local infrastructure still sucks. And health and safety measures inadequate. Maui County last week sued Hawaiian Electric Co., claiming $5.5 billion in damages and alleging both failure to maintain the grid and failure to shut it down in the face of a red flag warning from the National Weather Service.

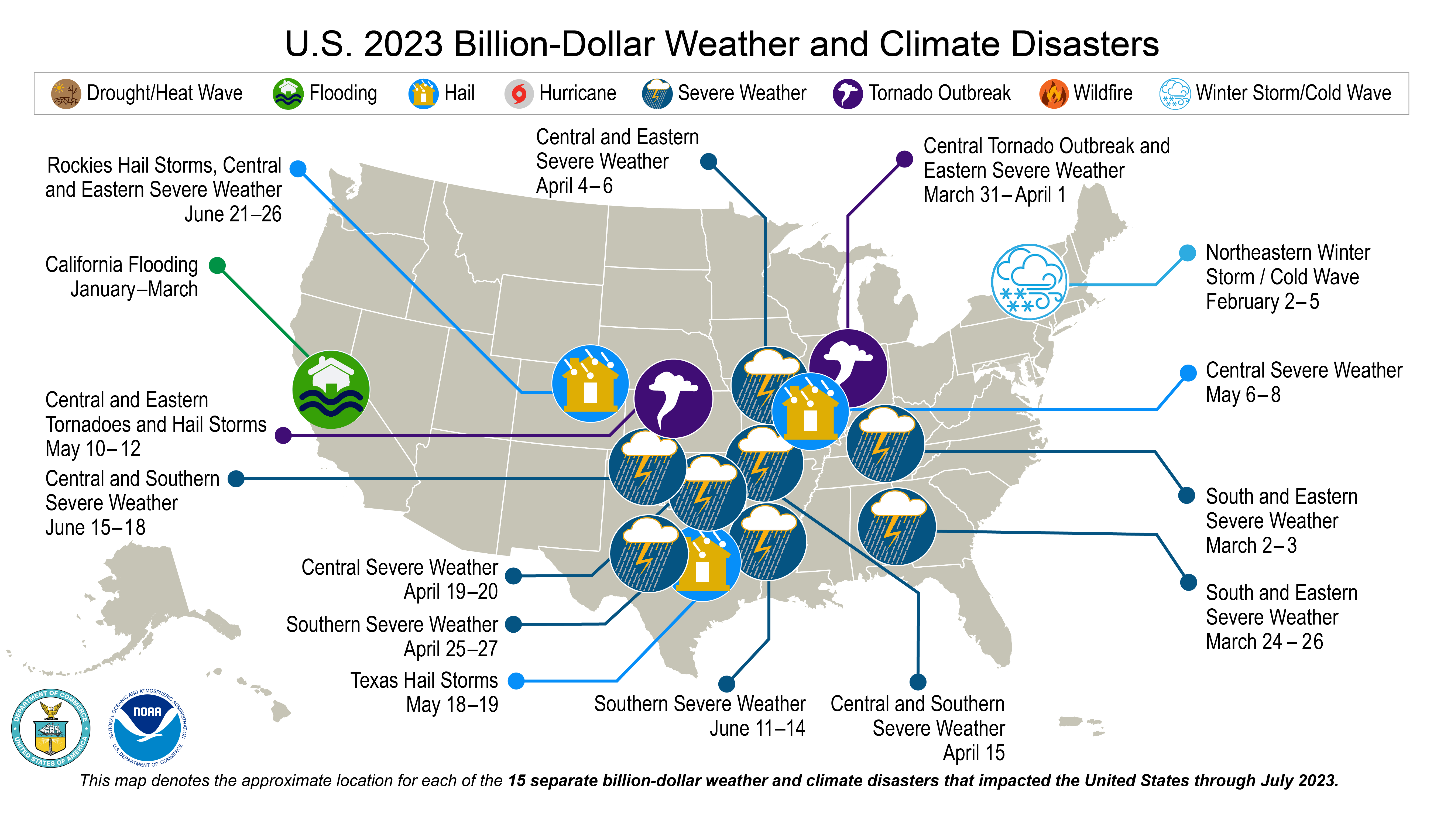

Climate catastrophes are happening right now. Even before the Maui fires, 2023 had seen 15 weather and climate-related disasters with more than $1 billion in damages, a new record.

And as the UN and myriad others warned us, it is disproportionately the poor and the socially, and economically vulnerable who bear the brunt. Maui residents fear that the fire already has set off a land grab, with the development of more luxury and high end properties, raising the cost of living even higher and pushing out workers, Native Hawaiians and other local residents.

Leaders in business, finance, and investment have slow-walked their response, to say the least, to the escalating climate catastrophe. While the world is literally burning, many still assume business is as usual and remain deaf to the urgent need for action.

Wall Street’s willful ignorance

Speaking of tone-deaf, almost at the same time Maui was burning, Goldman Sachs CEO (and part-time DJ) David Solomon was getting in trouble for, um, being a bit of a dick. Or, as New York magazine asked, “Is David Solomon Too Big a Jerk to Run Goldman Sachs?” The article describes the “mutiny” against the pugnacious chief of what was once – but maybe no longer – the world’s most prestigious global bank.

One of the charges against Solomon (aka DJ D-Sol) was his attitude toward a group of student climate change activists at his alma mater, Hamilton College. The students allege the CEO was rude and dismissive of their concerns when they approached him at a trustee event earlier this year. Solomon chairs the board of the Clinton, New York-based liberal arts college.

The magazine scoops that, after their March encounter with Solomon, the students penned a letter to the university paper describing their version of events, and expressing their disappointment and displeasure with the CEO. According to New York, at least one of the students “left the encounter in tears.”

The students allege that Solomon “laughed and told us he’d be dead in 30 years, so climate change would be our problem anyway. Yet, later in the conversation, he asserted his optimism for the future of society and our planet. His willful ignorance continued, with seemingly no intention to actually learn or genuinely engage with us beyond belittling us. When we brought up the topic of climate justice, he didn’t know what it was.”

At least in the eyes of these students, the CEO of a major investment bank seems oblivious to the seriousness of the climate crisis and its social implications.

That by many accounts Solomon is a jerk makes the story resonate. And his supposed attitude toward climate is reflective of major institutions, asset owners and business leaders, that have yet to catch up to what climate change is doing and what needs to be done in response. We see that not just in this one encounter, but in how institutions more broadly are responding, or not, to cries for climate justice.

Put simply, we need a step-change in our thinking with regards to how and where we invest our capital. It is not enough to think about the clean energy transition as an investment and capital markets opportunity for the future. We need to factor the enormous social and economic costs of climate change today.

Failing infrastructure

It may not be the role or responsibility of institutional investors to bear the burden of those costs – or at least not all of them. But they sure as hell better be aware of such costs and do their part to reduce and mitigate them. We all pay the price for the destruction wrought by climate change. It is the ultimate tragedy of the commons, even as it is inevitably the poorest and most vulnerable among us who pay with their lives.

Today, most institutional capital does not even address our toughest social and environmental problems. Financing solutions in affordable housing, sustainable food and reliable renewable energy is hard. It seems easier, and seemingly better, to make money elsewhere. But investors should start opening their minds to the possibility of providing solutions, or else the tragedies and the inequalities will keep compounding.

In Lahaina, the situation has been compounded by the legacy of colonial capitalism, crumbling infrastructure, the diversion of water resources and the chronic shortage of affordable and family housing.

According to a 2023 report from Aloha United Way, just under half of all households in Maui County, which includes Lahaina, are below the ALICE threshold, for Asset Limited, Income Constrained, Employed. The number of households below this threshold increased 15% between 2019 and 2020.

“We’ve been really trying to call attention to the fact that it really just takes one emergency to tip someone over into poverty, and that tipping point for us was the pandemic,” Aloha United Way’s Kimo Carvalho told Maui News. And that was before the fire.

The more than 2,200 structures that burned included homes housing multi-generational families, and affordable housing units. An 86-unit affordable housing complex that was destroyed had only opened in December. We’ve previously discussed in this column Maui’s chronic, and ongoing, fights over water (see, “Sustainability is at risk when asset managers are the judge, jury and executors of the ESG agenda”).

It is tempting to try and find a silver lining of hope in this current disaster. To say that now, with this focus on Lahaina and the federal dollars that are surely coming, is a chance for Maui to build back better and stronger (see, “In Maui, investing in future resilience and community stewardship after the fires”).

Certainly there is an opportunity for impact investments in interesting projects across Hawaii, in everything from agriculture to solar and broadband development. Hana Ranch on Maui, an experiment in regenerative agriculture, was purchased by Bio-Logical Capital back in 2014 for $9 million, it is currently on the market for approximately $75 million, if anyone’s interested. You’d have Oprah as a neighbor!

Having spent some time working on driving investment into Maui, I have a sense of how challenging it can be to make progress. The politics and red tape are legendary. Costs are high. And the challenges, environmental and otherwise, are immense. We need to be realistic about what it will take to make a difference in money, time, patients, and true community engagement.

And it’s not as if we’re even done with disasters. As this endless summer nears its end, we are staring down the barrel of a new hurricane season, not to mention peak fire season as wildfires continue to burn. People in whole swaths of the U.S. and elsewhere still are experiencing record-setting heat.

Climate justice

The students at Hamilton College are hardly outliers. Environmental activists, having been largely successful in their push for fossil fuel divestment at college endowments, are focusing more of their attention on environmental and social justice.

When the fossil fuel divestment movement started in earnest around a decade ago, the idea was to encourage institutions to divest from the fossil fuel industry (predominantly equities) and invest in the renewable economy. The so-called stranded asset risk argument helped make the case against holding fossil fuels. For various reasons, the investment part of divest-invest has been far harder to implement.

In May of last year, students at Harvard issued “Whose University? The Case for Reinvestment at Harvard.” In addition to divesting from fossil fuels (which Harvard has broadly said it will do), the students argued that the university should reinvest the funds from its $53 billion endowment in funds, such as for affordable housing and renewable energy, to “repair the harm it has caused in the past.”

The gist is Harvard has done bad things – as a gentrifier, by not paying taxes, through investments it has made in the global South. Now the university should make amends by investing funds from its endowment in positive ways.

Is the argument going to fly? No. But watch for Harvard and other universities to start to tout their impact investments and, more broadly, the impact of their investments. Meanwhile, Hamilton College has not yet divested the fossil-fuel holdings in its $1.3 billion endowment.

DJ D-Sol in da house

A Goldman spokesperson told New York magazine the encounter didn’t go down as the students say it did. Solomon has enormous respect for the students and “he did not and would not say things to offend them. We strongly dispute the claims that he did,” Goldman spokesman Tony Fratto told Bloomberg.

Solomon won the CEO role at Goldman in part by seeming to advance the cause of female employees and more junior staffers at the investment bank, according to numerous outlets and recounted in The Times. That effort has since gone somewhat pear-shaped for Solomon during and after the COVID pandemic, as junior bankers have complained about long hours. Goldman was forced to settle complaints of gender bias and that the firm had created a toxic work environment for women.

Still, it seems weird that the Hamilton students who were in the room with Solomon should claim to be offended if they were not. They are in a position to know if they felt offended or disrespected. Why would they make this up?

Maybe Solomon just offends everyone. One of my favorite anecdotes in the New York article relates how the bank’s “image specialist” (what a job!) suggested that, to make Solomon appear more approachable, he walk the floors of Goldman’s offices and actually talk to people.

It did not go well. Solomon apparently would “stomp” around and only approach the people he knew personally, scaring even them. Aren’t investment bankers supposed to be charming? I guess only to corporate CEOs.

Granted, it is the job of major investment bank CEOs to be conservative (if not jerks). And it is the job of student activists to be annoying, overly sensitive, and keen to take on Wall Street. By complaining about their conversation with Solomon the students were literally sticking it to The Man.

I understand the value of divestment as an activist tool. But let’s be clear: it makes no practical difference (from a capital markets perspective) to the companies under attack. On the other hand, an institution can divest their equities – which is mostly what we are talking about – from the fossil fuel industry, or not, and have little meaningful impact on their portfolios’ performance.

And I also understand the arguments for engagement with companies, even oil companies. The record shows its effectiveness is often limited.

So while the divest – engage debate leaves me flat, what gets my goat is how one-dimensional, condescending and paternalistic the arguments against divestment are, effectively telling the activists not to worry their pretty little heads and to let the titans of finance do their jobs. Because there are real economic reasons for investors to be concerned about climate change.

Increasingly, there is also a financial case for investors to care about climate and social justice. If we don’t start putting our money where it needs to go – to rebuild essential infrastructure, and support vulnerable communities – our social bonds will snap. If you thought the Covid bailouts were costly…

Puerto Rico’s debt

Lahaina, of course, is not the first marginalized community in the U.S. to be deviated by the impact of climate change. We are still dealing with the fall out of Hurricane Katrina in New Orleans and the surrounding area 18 years (and four presidents) later. The rebuild was not equal for all. Now comes the dramatic sea rise that is leaving New Orleans even more vulnerable to future storms. And like much of the rest of the country, New Orleans has a chronic affordable housing crisis.

Institutional investors, by and large, do not help communities build back better. Sometimes they can make things worse. Like when they invest in Puerto Rican debt.

A November 2022 post from the U.S. Government Accountability Office charts the slow recovery of Puerto Rico to the damage caused when Hurricane Irman and Maria hit in 2017. The GAO said that Puerto Rico’s government estimated that “it would need $132 billion from 2018 through 2028 to repair and replace the infrastructure damaged by the hurricanes.” But the GAO finds that very little of the federal funds that have been made available to the American have even been spent.

Puerto Rico’s debt burden and tax regime have their own specific history, and obviously the commonwealth is not a U.S. state. Still, one has to wonder: is this Maui’s future? One where the rich are comfortable in their own bubble, with their power generators and their $500 meals, and the poor get left further behind? And the debt piles up, because we can’t afford to fix what is broken.

Bloomberg this month ran an interesting, albeit depressing, article, “Hedge Fund Paradise Hides Puerto Rico’s Crisis In the Making.” It described how tax incentives and other factors have hedge fund managers, in particular John Paulson, flocking to Puerto Rico. But 40% of the island’s population is living in poverty, an affordability crisis that is compounded by the influx of wealthy residents and a fragile power grid managed by Prepa, the local electricity company which has already once filed for bankruptcy.

“That has Puerto Rico teetering on the edge of another possible fiscal crisis, exacerbated by Prepa’s debt burden and rising electricity rates that have led to protests in the streets,” Bloomberg writes. The commonwealth itself had to restructure its debt in 2022, after filing for bankruptcy in 2016.

“No bondholder ever forced the government to issue bonds,” complained one particularly cynical investment manager who holds Prepa debt. Now, he says, “It’s all about how bondholders are asking for too much.”

But neither did any community ask for such atrocious mismanagement. Plenty of banks, including Goldman Sachs, made money underwriting Puerto Rican debt. Local residents are dealing with the consequences.

The problem is institutional investors, in the fulfillment of their fiduciary duty, put money not where it needs to be invested, but where they are going to get the best risk-adjusted return. As a result, we are not investing in the social infrastructure and glue that we need to.

Climate horizon

It turns out that DJ D-Sol (sorry, it never gets old for me) does know a little something about climate justice and the clean energy transition. Or at least his spinmeisters want us to think so. Last November, Goldman Sachs and Bloomberg Philanthropies announced its first blended finance investments through their Climate Innovation and Development Fund for sustainable transport in India and Vietnam.

In the release, Solomon touts the ability of the fund, managed by the Asian Development Bank, to bring in private capital “to accelerate the decarbonization of mass transportation in India and Southeast Asia and make further progress in the journey of climate transition.” Note: this is philanthropic capital from both Goldman and Bloomberg.

Catalytic philanthropy is all well and good. But not sufficient. The energy industry alone needs to spend $1 trillion more than it does now each year to provide decarbonized, affordable energy. “In solving such a complex problem lies enormous opportunity for our clients,” Solomon said in Goldman’s sustainability report last year.

But Goldman and many others are not yet willing to put the full force of the capital markets, or our investment dollars, into the solutions needed, arguably including risky investments in frontier markets.

In the same sustainability report, Goldman said it is over halfway toward meeting its 10-year pledge to mobilize $750 billion in sustainable finance. But its Horizon Climate fund, which closed in January at $1.6 billion, is at this late date the firm’s first direct private markets strategy dedicated to climate and environmental solutions. The fund’s $1.6 billion is just over one-tenth of 1% of the $1.5 trillion in assets managed by Goldman Sach Asset Management.

We are going to need all that money, and more, if we are going to successfully transition to a clean energy economy and prevent tragedies like Lahaina. And to insure that when they do happen, we build back better and stronger for everyone, not just for the very rich.

Imogen Rose-Smith is a contributing editor at ImpactAlpha. A longtime senior writer for Institutional Investor, she was most recently a fellow in the Office of the Chief Investment Officer of the University of California. Catch up on all of Imogen’s Institutional Impact columns.