Five years ago, we co-led a research project exploring the value of classification in impact investing, with the goal of making it easier to invest for impact across a portfolio.

At the time, the publicly traded and privately owned parts of the market were using different terms. Definitions of “sustainability”, “ESG”, “SRI”, and “impact investing” were still in flux. And the field was growing, making it harder, not easier, to compare apples to apples when making investment decisions about risk, return, and impact.

As more people managing larger portfolios wanted to turn to impact, we feared that without more rigorous ways to classify intentions and performance around impact, they would be understandably nervous to step in. The multi-stakeholder research led to at least two important developments:

- The coining of the term “impact classes.” Like asset classes, impact classes are a way to group investments with similar characteristics, but by impact traits instead of financial ones.

After engaging with dozens of investors, it became clear they believed that robust segmentation in impact investing was essential to market clarity (by simplifying terms), market efficiency (by creating a common taxonomy), and market assurance (by creating observable and comparable clusters). - The creation of the Impact Management Project. A natural outgrowth of the research, “the IMP” was incubated by Bridges Ventures. Nearly five years later, after conferring with hundreds of organizations to develop consensus about measuring and managing impact, the IMP is now established as a pillar of best practice.

The five dimensions of impact clarify that what, who, how much, contribution, and risk are key attributes that underlie every impact investment. And the IMP’s “ABC” categorization system, which organizes enterprises and investments by their impact strategy, has been thoroughly vetted globally and is currently being integrated, thanks to the IMP’s structured network collaborative, into the major impact ratings, standards, and certifications.

Fast forward to late 2020 and the importance of classification has become clearer still. ESG investing, now accounts for about 1 of every 3 dollars professionally managed in the US, with 42% growth since 2012, according to the USSIF’s 2020 report released last month. Globally, the GIIN has reported annual growth of assets under management for impact investing ranging from 30-50%.

Clearly, more investors are looking for impact, upping the temptation and risk of “impact-washing”. And impact investing products are increasingly being offered by diversified rather than specialized investment managers, making differentiation all the more critical.

In our view the Impact Management Project’s use as a means for classification in impact investing will become ubiquitous in 2021, for individual funds and across full portfolios.

ABC framework for your strategies

As our predilection for the IMP suggests, classification begins with an investor’s strategy for creating intentional impact, using the “ABC” framework: “Avoiding” harm in order to mitigate negative social or environmental effects; “Benefiting” stakeholders in order to favor more socially and environmentally sustainable business practices; or “Contributing” to solutions that address identifiable social and environmental challenges.

The ABC framework is not intended to replace the current terminology preferred by the market: “negatively screened”, “ESG integration”, “thematic” or “impact” investments. In fact, these terms align relatively neatly with the ABCs.

Negatively screened investments might reject companies that do overall harm to people and planet or are unrated by the ABC framework. Investments that integrate ESG factors to start to avoid or reduce some of their harmful impact can fall into the “A” category. Investments that are working to create positive benefits for stakeholders, such as thematic investments in specific solution areas, would fall into the “B” category, and investments working toward a measurable impact outcome for which the population or environment is currently underserved would be in the “C” category. If used carefully and accurately, these known terms are a solid place to begin.

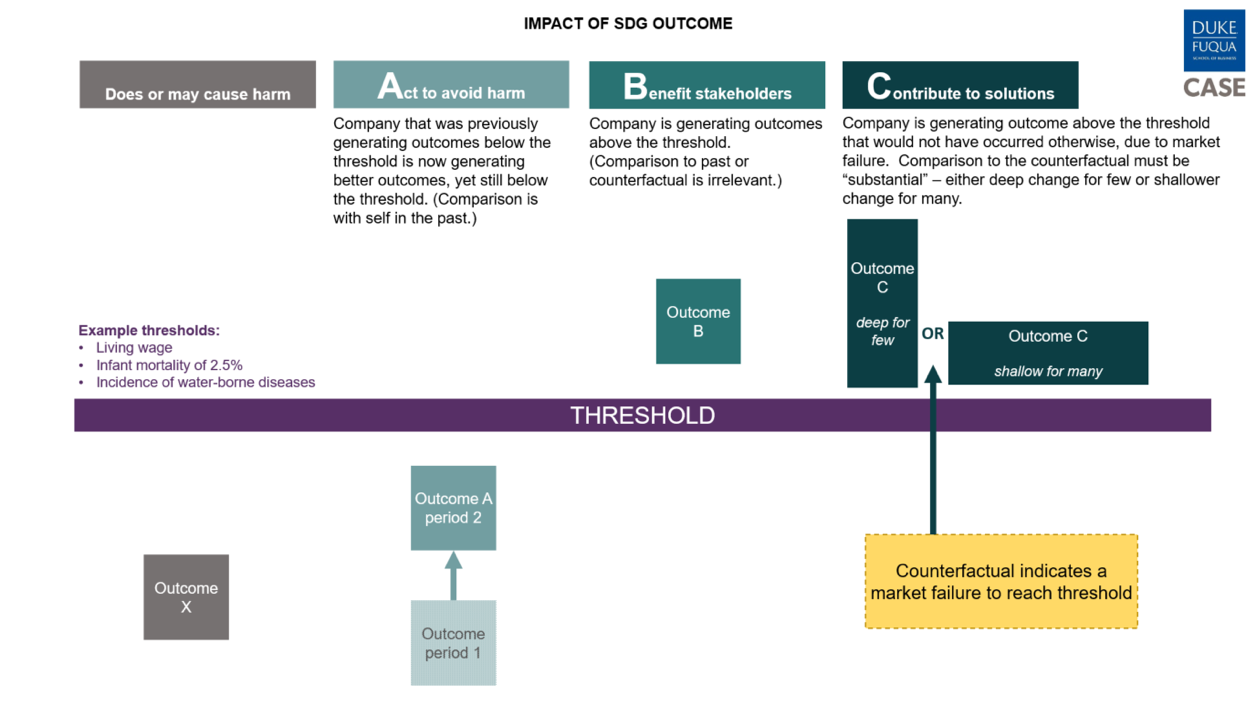

The tens-of-trillions of dollars of “impactful” investments being tracked by USSIF collectively and individually include elements of “A”, “B”, and “C”. The key to market rigor, authenticity, and integrity is the ability to scrutinize each investment with precision, by specifying exactly what impact goals are intended for each of the social or environmental outcomes the enterprise or investor intends to create. This can be seen in the chart below, developed by CASE at Duke in collaboration with the UN Development Program and the IMP.

Different outcomes within the same company or asset can be categorized as Does or May Cause Harm, Acts to Avoid Harm, Benefits Stakeholders, or Contributes to Solutions. The categorization depends on how the outcome compares to a threshold between harm (below the line) and benefit (above).

For example, Tideline was recently working with a large agriculture fund to help fortify its impactful investment strategy. The fund reduces harm by mitigating emissions in production, benefits stakeholders by engaging deeply with the rural communities that form the backbone of its workforce and supply chains, and contributes to solutions by investing in innovative land conservation and preservation technologies. Yet the balance of effort is weighted toward avoiding harm and so the manager appropriately classifies the fund as having an “A” impact thesis.

Sustainable Development Goals for your outcomes

In order to make the “A” classification above, Tideline and the agricultural fund manager needed to understand the range of social and environmental effects at play. This is where the second key framework comes in: the UN Sustainable Development Goals (SDGs).

The SDGs define outcomes that are valued around the globe. Market leaders are identifying the key SDGs and underlying SDG “targets” that an investment strategy touches, and assigning each of these goals to an ABC classification, in order to clarify the different ways in which a fund is impactful — whether by avoiding harm, benefiting stakeholders, or contributing to solutions.

In the case of the large agriculture fund Tideline had supported, there were eight targets across five SDGs. The fund advanced five of these targets primarily by avoiding; two by benefiting; and one by contributing. Once the analysis was complete, the totality of the fund’s efforts came into clearer focus, along with the most appropriate fund-level label.

The U.N. Development Programme is setting clearer expectations for how investors wanting to align with the UN SDGs can use impact classifications as part of their work. They have included the ABC framework in their new SDG Impact Standards, which will be the basis for a new UN seal for SDG-enabling investments in the future. (Tideline worked with UNDP in 2018 to conceive of SDG Impact.) Some tools:

- CASE at Duke is working with UNDP and the IMP now to develop a video-based online training, to be available next year, to help any enterprise and investor up their game in impact measurement and management, from strategy-setting, to management, reporting, and governance. A first video on the five dimensions is available here.

- The Impact Classification System allows investors to self-classify their assets by SDG goal and ABC impact thesis and share those classifications with others.

Classification for the market, not marketing

Managers should not fear classification. We were at pains to make three points five years ago and will make them again now.

First, the ABC framework is not a value judgement. The ability to “avoid”, “benefit”, or “contribute” is more a function of the market and investment strategy than it is the manager. What matters is an investor’s ability to accurately discern and describe the full scope of its positive and negative impacts, across the ABC continuum. Classification is not about the “race to C”, even as we believe most investors can and should be doing more to maximize the impact potential of their specific strategies. Frankly, if more companies avoided harm through their operations, we would likely need fewer “C” investments. And large companies can create significant impact at scale by avoiding harm. We actually want to see more “A” class enterprises and investments.

Second, classification can help enormously with expectation-setting around impact measurement and management. An “A” fund requires different impact data than a “B” or “C” fund and its approach to impact management and reporting should therefore be different. For a “C” fund, investors are right to expect a higher level of practice excellence, benchmarking against others, and regular assurance.

Third, classification creates a roadmap for investor diligence. It is thrilling to see so many new funds labeled “impact” coming to market. But investors should apply the same level of diligence to their analysis of impact as they do to financial bona fides.

Impact performance-based decision-making

There will always be disputes about an investment’s proper classification – but also innovation in the methods for resolving those disputes. Toniic’s Tracer presents a fund or company’s self-classification, right alongside a classification that has been crowd-sourced from its investors. BlueMark’s “mandate verification” service is effectively a form of classification assurance. Disputes about classification are a good problem to have in impact investing. It means we are debating the nuances of an investment’s real impact, which is a profound sign of progress.

Classification is ultimately about a step-change in the maturity of impact investing. The biggest opportunity will arise, we believe, when more enterprises and investments classify their key outcomes in a trusted way, and then those classifications are used as the basis for decision-making and operational performance improvement.

At that point, the field will stop asking “is that an impact investment?” and start asking “how well did it do?” And most importantly, “What do we need to change to do better?”

Ben Thornley is a co-founder and managing partner at Tideline, where he leads the firm’s strategic advisory practice in impact investing. Cathy Clark is faculty director at the Center for the Advancement of Social Entrepreneurship (CASE) at Duke University’s Fuqua School of Business and founding director of the CASE i3 Initiative on Impact Investing.