Know what you own. A group of community development financiers is taking the lead on climate disclosure to clean up their loan portfolios.

Three community development financial institutions – Coastal Enterprises, Inc., Partner Community Capital, and Self-Help Credit Union – last year collaborated to calculate and disclose the greenhouse gas emissions associated with their loan portfolios. The group used a methodology developed by the Partnership for Carbon Accounting Financials, a membership organization founded by fourteen Dutch financial institutions via a Dutch Carbon Pledge at the Paris Climate Summit in 2015.

Because CDFI loan portfolios differ from those of commercial banks in both scale and complexity, the three CDFIs recognized there would be value in sharing resources and solutions throughout the carbon accounting process. Their collaboration resulted in the creation of a step-by-step working guide that financial institutions, particularly CDFIs, can use to understand the initial steps needed in the GHG accounting journey.

Climate impact

The emissions associated with CEI’s portfolio as of September 30th, 2020, were 12,641 tons of greenhouse gases, which is the equivalent of driving 2,724 gasoline-powered vehicles for a year. This represents estimated emissions across 343 companies with a total outstanding loan balance of $45.9 million. The top five sectors, in order of emission intensity (tons of CO2e emitted per $1 million dollars invested), are agriculture and food systems; energy; forestry; fisheries and aquaculture; and small and medium enterprises, such as restaurants and general stores. (Read CEI’s full PCAF disclosure online.)

The results of the exercise surprised us at times and showed how necessary it is to take a nuanced approach in interpreting and comparing data. First, portfolio emissions differ among CDFIs, as each invests in industries and geographies that are unique to their business models and local economies. However, the comparative emission intensity among the three CDFIs is relatively modest when compared to large, commercial banks, as CDFIs generally do not invest in the most heavily polluting sectors related to oil, gas, and mining.

That is exactly why we collaborated to adapt the PCAF model for CDFIs. A “farm” business in a traditional big bank’s lending portfolio versus a CDFI portfolio is different. Our use of sector-specific estimates from PCAF’s database don’t account for the size of the business (e.g., numbers of acres of farmland), the fuel type of the farm (e.g., many of CEI’s farms run on solar energy), or the use of synthetic fertilizers and pesticides (e.g., many of CEI’s farms are organic and have limited use of these products). Comparing the natural-resource based businesses in CEI’s portfolio to businesses financed by large financial institutions is like comparing apples and almonds.

Accounting to action

PCAF is a global initiative led by financial institutions committed to developing a common standard for disclosing and reducing greenhouse gas emissions from their loan and investment portfolios. Over 250 financial institutions, representing more than $71 trillion in assets, have joined the open-access partnership since its inception in 2015. In 2019, CEI participated in a cohort to adapt the European PCAF methodology to the North American market and has been joined in our disclosure commitment by five other CDFIs; Clearwater Credit Union, the New Hampshire Community Loan Fund, Partner Community Capital, Self-Help Credit Union, and the Vermont Community Loan Fund.

The PCAF initiative aims to align the current investment practices of the financial industry with the growing need for climate action. The movement for financial institutions to disclose their climate impacts has been steadily growing, evidenced most recently by the U.S. SEC proposal for public companies to provide specific climate-related information in their registration statements and annual reports. By disclosing the greenhouse gas emissions that lenders are accountable for through their financing, investors can incorporate this information into their decision making. Further, from a broader portfolio perspective, lenders can identify sectors where targeted financial products or technical assistance could encourage business owners and project developers to incorporate plans for greenhouse gas emission reductions into their business practices.

As financial institutions gain a greater understanding of the carbon impact of their borrowers, they can serve as catalysts for a transition away from fossil fuels and other carbon-intensive sectors. As mission-driven lenders, CDFIs can demonstrate leadership among financial institutions and other community development organizations in addressing climate change. This is a first step. The partnership ultimately aims to facilitate the alignment of the financial industry with The Paris Agreement and reach net zero emissions by 2050.

“The growing global membership of PCAF is an opportunity to put pressure on the largest financial actors in the world to make cleaner investment decisions and commit to transparent climate disclosures,” says CEI’s Keith Bisson. “This disclosure establishes a baseline for us to understand our portfolio and Maine’s small business economy, and how we intersect with both as we deepen our mission impact in addressing the climate crisis. It’s an opportunity to hold ourselves and all lenders accountable for our investments and, together, move towards a low-carbon future.”

As CEI considers how to use the information from this exercise, a starting principle is the impact investing adage: know what you own. This knowledge will inform new strategies and approaches, such as due diligence with an environmental lens. It is informing our thinking about sectors we should prioritize in terms of supporting climate adaptation and resilience. In some ways it is fortuitous that the higher emitting sectors are those in which CEI has deep history and expertise. We intend to develop a scorecard with industry specific benchmarks, and eventually provide businesses with advisory services to reduce their carbon footprints, through steps such as equipment upgrades and introducing sustainable business practices into their daily operation.

Climate leadership

The CDFI industry is increasingly recognizing the urgency of the climate crisis. Individually and collectively, CDFIs are using their economic development expertise to implement climate-conscious approaches to underwriting, reporting and asset management. By integrating carbon accounting, CDFIs can better explore, develop, and initiate incentives (such as interest rate deductions) for environmentally responsible practices in the private business sector. Additionally, as businesses look to decarbonize their operations, CDFIs can provide patient capital and business advice that is tailored to local industry.

As the impact investment movement gains momentum, investors in CDFIs, such as large institutional banks, will expect CDFIs to comply with these new standards of environmentally responsible investing. Shareholders are insisting on greater reporting of a company’s environmental, social and governance (ESG) impact as part of their investment decisions. CDFIs can be leaders, demonstrating to our investors that community development lenders are first-movers on climate-positive investment and disclosure practices.

Portfolio emissions

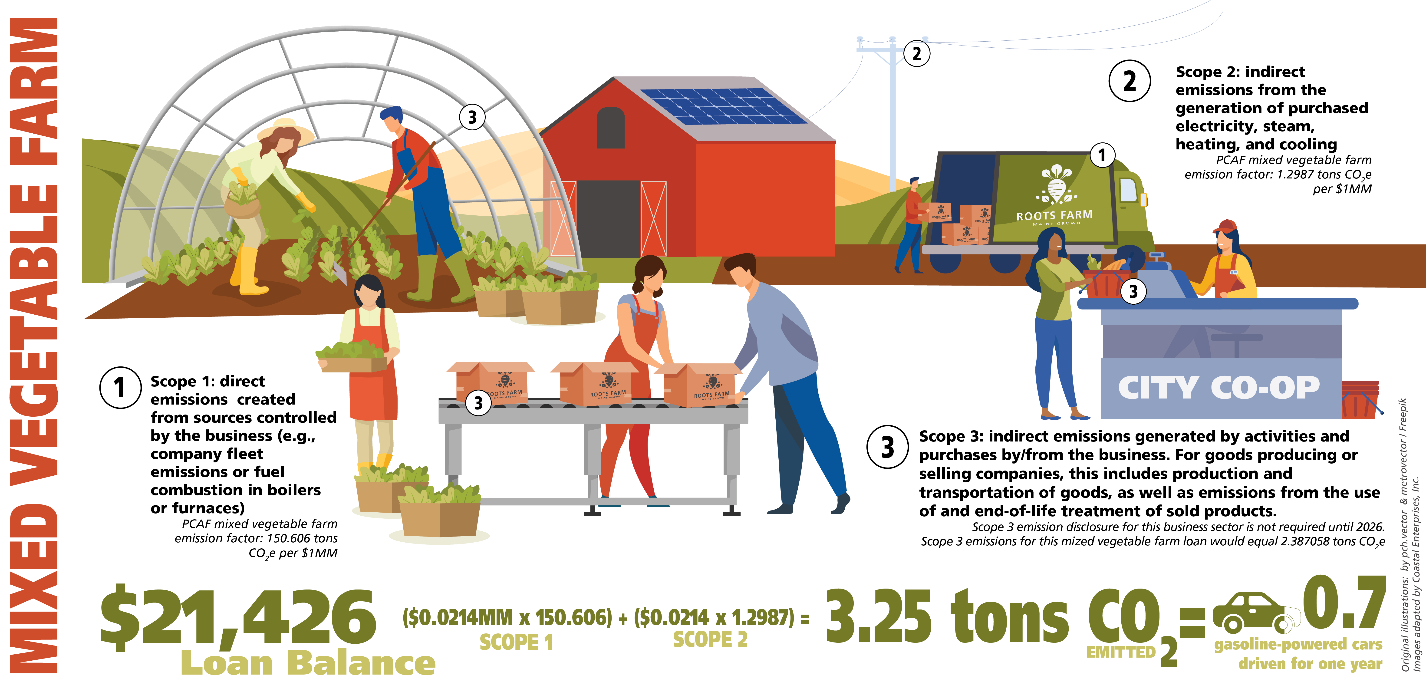

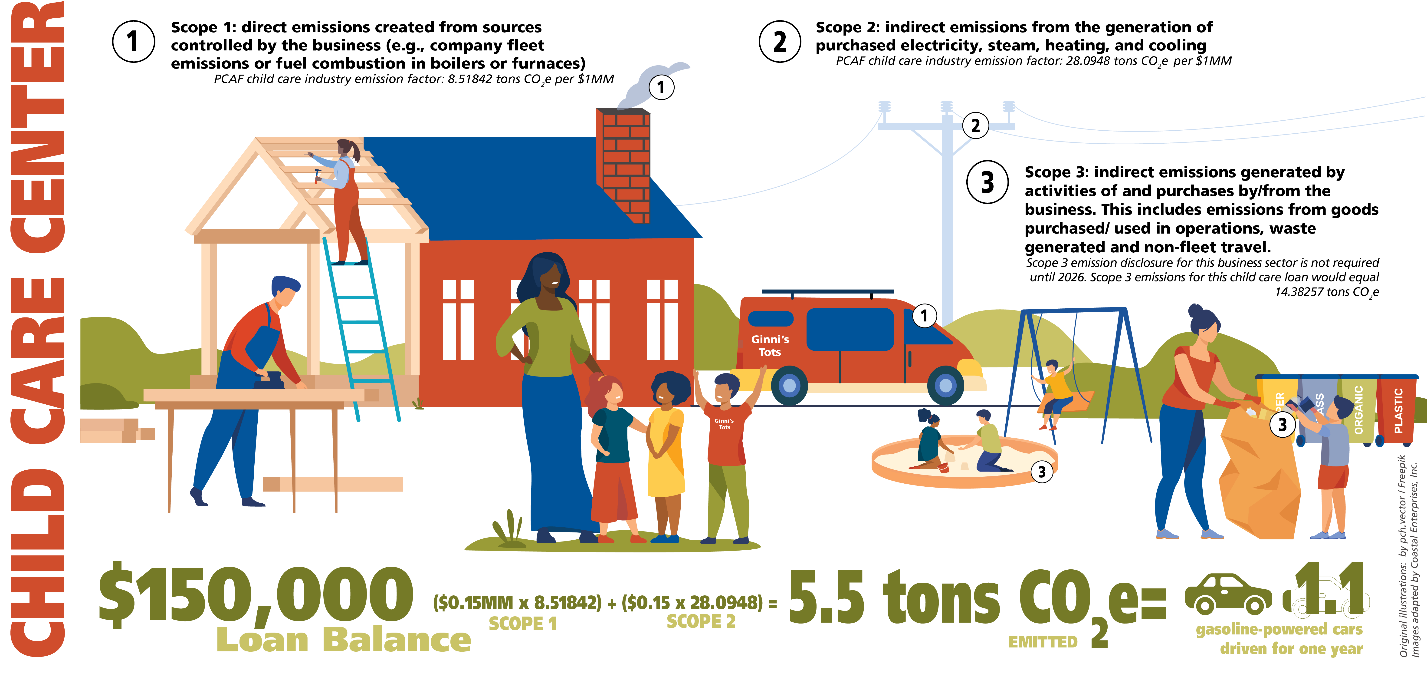

The following infographics walk through the greenhouse gas emissions calculation for two of CEI’s portfolio companies – a child care center and a mixed vegetable farm in Maine. These emissions are calculated using the PCAF methodology and rely on emission estimations based on the borrower’s business sector (NAICS code). The total CO2e emissions attributed to the financing of these companies are typical for our small business portfolio, where two thirds of CEI’s deals result in less than 5 tons of emitted CO2e.

Linnea Patterson is environmental lending specialist at CEI