ESG begins at home. As increasing numbers of investors are looking for environmental, social and governance investment opportunities, asset managers are directing more and more capital to ESG-focused funds. However, as the expectations of investors evolve, managers are likely to find that making ESG-friendly investments is not enough.

More than ever before, investors are focused on ESG attributes of asset managers themselves, including managers’ records on diversity, equity and inclusion (DEI). And just as the SEC has followed investor interest in sustainability with climate change disclosure regulations, asset managers should prepare for the possibility of SEC-mandated disclosures relating to DEI.

A notable step in this direction was taken in July 2021, when the SEC Asset Management Advisory Committee’s Subcommittee on Diversity and Inclusion recommended, among other things, that asset managers disclose data relating to racial and gender diversity within their workforce, officers, ownership and board, as well as the DEI considerations, if any, SEC-registered investment advisers serving as allocators or consultants incorporate into their fund recommendations.

The issue has drawn the attention of Congress as well. In December 2021, the House Committee on Financial Services released a report recommending that certain financial institutions be required to disclose data regarding the use of women and minority-owned asset management firms. In April 2022, the Senate proposed legislation that would direct the Department of Labor to survey best practices for increasing diversity in the asset management industry.

Managers should make it a priority to get ahead of these developments while DEI is still emerging as a priority for investors and regulators.

Building an infrastructure to respond to DEI queries and expectations of investors and regulators cannot be accomplished overnight, and managers who are unprepared when facing DEI disclosure requirements risk playing “catch up” indefinitely. Managers should also brace for greater scrutiny of their DEI efforts, even if such disclosures are not mandated.

Diversity and inclusion infrastructure

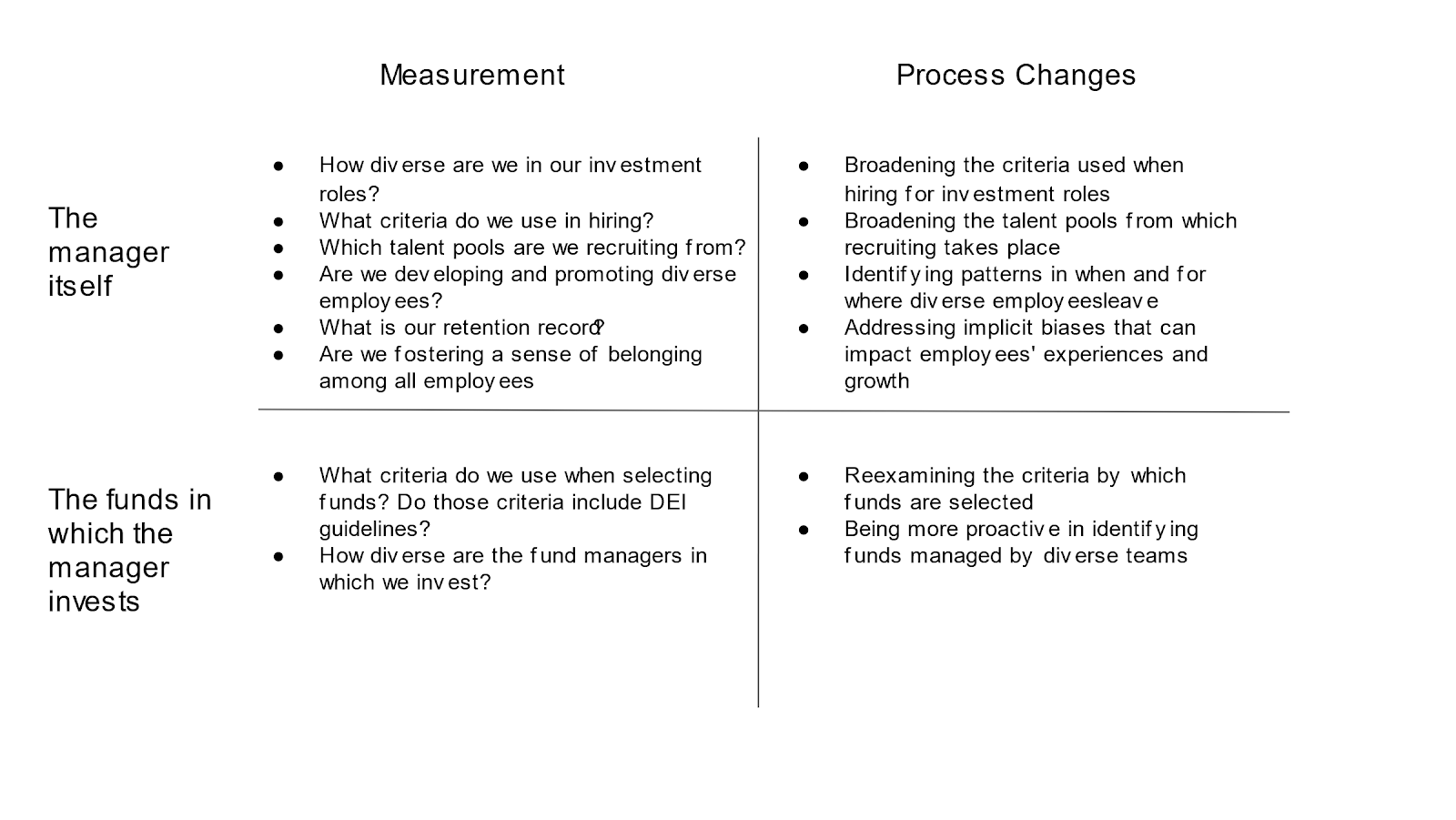

Managing the process of building a DEI reporting infrastructure and addressing areas for improvement can be made easier by mapping the components involved. An asset manager needs to examine both itself as an organization and how DEI factors are incorporated into its investment and allocation decisions. More likely than not, that measurement will identify areas where changes to current processes could be explored. These components can be represented in the following matrix:

What gets measured gets managed

While it is tempting to focus on process improvements when considering DEI issues, it is critical for managers to first gather reliable data to accurately identify where improvements are needed and, then, whether progress is being made.

A data-driven approach to addressing diversity and inclusion at the firm level is all the more important given the industry-wide figures, which show investment management in a time of flux on DEI. Recent industry surveys have shown, for example, that while approximately 16% of the executive ranks of U.S. asset management firms were members of racially-underrepresented groups in the industry and 25% were women, only 1.4% of assets under management in the United States were entrusted by investors to firms owned by women or people of color.

But numbers tell only part of the story. DEI data collected by asset managers must be both quantitative and qualitative. It is not sufficient to know how many diverse personnel are in each role – managers also need to know whether professionals from underrepresented groups have effective sponsorship and development, are being given increasing opportunities for direct client contact, and are not limited by implicit biases at the organizational or client level.

Further, the measurement phase needs to include an assessment of the decision-making guidelines that shape workplace diversity, such as criteria used in hiring and promotion, and recruiting efforts targeted toward diverse candidates. Gathering this information in a systematic way not only shows where the organization is, but encourages it to confront gaps and shortcomings.

Similar data collection is needed regarding DEI factors in investment and allocation. Of the funds to which the manager allocates, what percentage are minority- or women-led, or have substantial diverse representation through their ranks? Similar questions can be asked of companies in which the investment manager takes an equity stake. Finally, managers should review the factors that determine how allocation and investment decisions are made.

This level of information gathering goes beyond the disclosure proposed by the SEC’s DEI Subcommittee, but it is arguably what would be required for a manager to understand its level of DEI engagement, to interact meaningfully with regulators and investors regarding its DEI metrics, and to set goals and adjust practices.

But while most firms track the racial and gender composition of their workforces, fewer systematically track factors like mentoring and client-facing opportunities, or external metrics such as the racial and gender composition of funds to which assets are allocated.

Allocation: Where DEI is elusive

Once managers have connected the necessary data, they can begin to ask questions, identify areas for improvement and assess possible changes to their processes.

The roadmap for each manager will be different. However, the proposed recommendations by the SEC’s DEI subcommittee highlight one area likely to address a critical concern held by many managers: whether incorporating DEI into investment decisions is a prudent fiduciary exercise.

The SEC’s DEI subcommittee says it is, and recommends that the SEC issue guidance that a manager’s fiduciary obligations do not require it to exclude funds solely on the basis of AUM or length of track record (lower levels of which often correlate with women and minority-managed funds) — and that doing so could actually run contrary to an asset manager’s fiduciary duty, as research has consistently shown that diverse management teams do as well as, if not better than, non-diverse teams.

The subcommittee undoubtedly made this recommendation precisely because of the role that fiduciary duty concerns have played in limiting the assets allocated to funds run by diverse leaders.

On its face, disqualifying from allocation those managers that are too small or too new seems a justifiable risk mitigation measure. However, the argument can also be made that such a filter allows allocating managers to fulfill their fiduciary duty by relying on easily quantifiable attributes—AUM and years managing—instead of attributes that are more relevant but harder to measure, such as quality of investment thesis and robustness of deal flow.

Indeed, while many managers are taking steps to bolster diversity and inclusion among their executives and leadership, there is still hesitancy to do so when it comes to investment allocation. Yet it is clear that the asset management industry cannot achieve genuine diversity and equality unless that diversity and equality extends to the actual allocation of investment capital.

The leadership necessary

Improvements in diversity and inclusion in any organization often require day-to-day changes in how an organization runs its business, manages resources and rewards employees. Those changes, in turn, require buy-in from the top and champions at sufficiently senior levels.

As managers undertake better reporting of DEI metrics and look for ways to strengthen DEI in their firms, it will be important to ensure that these efforts are supported both in human resources and within the investment function itself.

Managers that take these steps are likely to find themselves ahead of investor and regulatory expectations and thus able to differentiate themselves from their peers on an issue of increasing importance.

Taleah E. Jennings is a litigation partner at Schulte Roth & Zabel LLP.