Hundreds of professional investors and fund managers are now using one of the many variations of revenue-based finance (RBF)—structured exits, royalty finance, and so on. Yet despite growing adoption of these structures, investors face significant open questions, such as “Are these deals equity or debt?” It’s common to see investors take different views on very similar structures, and many legal and accounting professionals are not certain of the right answer.

How we classify RBF structures matters because equity and debt have markedly different tax and accounting requirements. Getting the accounting or tax treatment wrong can completely change the economic viability of a deal, which means any uncertainty in these areas could stifle adoption of these new structures. That would be too bad because RBF is one of most effective ways for underserved entrepreneurs to raise the capital they need to fuel growth while meeting investor needs.

Given the growth of these new structures, why is there confusion over how to account for them? For reasons that are ancient history to investors, tax rules in most governments are generally assumed to classify a structure as either equity or debt, which leads to uncertainty when investment structures do not clearly fit one of those two categories. When a structure is a hybrid, like convertible bonds, often the accounting question is something like “What part of this is equity and what part is debt?” However, most investors don’t know the rules for taxing hybrid structures and instead treat investments as if there is always a binary choice: a structure is either equity or debt.

We do not have a good vocabulary for talking about the idea that early-stage investors who think of themselves as equity investors might invest in a way that gets treated as debt for tax purposes. Just because investors think of themselves as equity investors does not mean tax authorities will always agree.

To illustrate this confusion, consider two investors using the same basic structure: an RBF agreement that requires the company to pay the investor R% of revenues until a total dollar amount of payments is a multiple M of the initial investment.

Our first investor thinks of herself as a debt investor, so we will call her Ms. Debt. As a debt investor, she invests only in companies with secure and predictable cash flows. She is concerned mostly about credit risk and does not look to capital gains as part of her investing strategy. She invests in companies that have a lot of seasonality, so she likes the fact that revenue-based investment structures help the companies manage their seasonality better than traditional debt structures. She typically invests for a target IRR of about 8% and adjusts the revenue percentage and investment multiple to get to that target IRR. For example, in a recent deal she accepted 3% of revenues and a multiple of 1.5x.

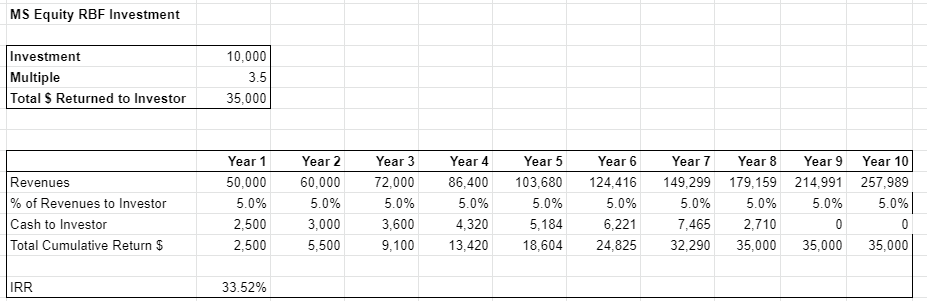

Our second investor, Ms. Equity, considers herself an equity investor and expects equity-like returns with a target IRR of greater than 30%. Ms. Equity is happy to take on a lot more risk than Ms. Debt and, prior to using RBF, thought about investing primarily as a way to generate capital gains. She now invests using RBF in companies that have a lot of growth potential but have not yet established enough financial history to attract debt investors. In a recent deal, she accepted 5% of revenues and a return multiple of 3.5x to get to her target IRR.

Both Ms. Debt and Ms. Equity just used essentially the same investment structure—so is that structure equity or debt? The answer to the question is to realize that we are making a mistake if we think that our intent always matches up with the accounting and tax rules we have to follow. We should think about the investor’s intent as a separate question from how the structure will be accounted for.

If Ms. Equity is used to thinking about equity deals, she may have structured her RBF deals using mandatory equity redemptions, intending to account for those redemptions as some mix of return of basis and capital gains. That makes sense to her, as she invests for capital gains. But that does not mean the tax authorities will agree.

In the United States, where many RBF investors work, there is a tax treatment specifically for contingent payment instruments called the Non-Contingent Bond Method created under § 1.1275-4(b) of the Income Tax Regulations. It appears that both Ms. Debt and Ms. Equity are subject to that tax treatment regardless of their intent. The IRS is likely to look at the underlying nature of the investment and determine that it is a debt instrument that should be accounted for as a contingent payment instrument.

What happens if the IRS tells Ms. Equity that despite her intent and equity-like returns she was actually using a debt instrument under the law? The Non-Contingent Bond Method accounting is complicated, but Ms. Equity may have to pay income taxes a lot sooner than she expected to and may even have to pay more in taxes in the early years of the investment than she receives in income.

If Ms. Equity ends up getting taxed as a debt investor, it’s not the end of the world or a barrier that should prevent her from investing. The problem occurs when Ms. Equity does not know this tax treatment exists before finalizing deal terms.

RBF structures can satisfy the economic needs of both equity and debt investors, so from the investor perspective, we should consider them a third category that can have a mix of equity and debt risk-return characteristics.

Perhaps someday tax authorities will agree. Meanwhile, RBF investors should be aware that how these structures are treated for tax purposes will depend on where in the world you work and the specific qualities of each deal structure. Instead of waiting for someone to get audited or for the IRS to clarify the on their own, the best solution may be to commission a well-designed private letter in favor of increased adoption of RBF. Until then, word to the wise: Always check with your accountant before signing off on terms.

John Berger, CFA, is director of operations and impact solutions for Toniic, a global community of investors committed to putting capital to work for social and environmental good.