Private equity has a significant opportunity to create financial and societal value through sustainability. PE firms that invest in improving the management and quality of companies to enable increased valuation multiples can also bring sustainability to their value creation tool box. Unfortunately, many PE firms do not yet know how to identify, create or capture that value.

Our research into both PE firms (GPs) and institutional investors (LPs) finds that most are focused solely on identifying major red flags during due diligence and collecting a few ESG reporting metrics once an investment is made.

Our assertion that sustainability drives value is based on our Return on Sustainability Investment (ROSI™) research across industries that has identified nine mediating factors that drive better financial performance when companies embed sustainability into corporate strategy: operational efficiency, risk mitigation, improved employee productivity and retention, innovation, sales and marketing, customer loyalty, earned media, and better supplier and stakeholder relations.

For example, Investindustrial, a leading European PE firm, uses sustainability strategies and ROSI™ to build more sustainable companies that attract higher valuations at exit. One such acquisition is Neolith, a pioneer in the technical sintered stone sector which, under Investindustrial’s ownership, developed sustainable design criteria that eliminated silica in the formulation of products. This innovation helped the company access new markets, and also reduced operating costs due to less use of energy and water and increased use of recycled materials.

On the LP side, one European investor collects the portfolio companies’ ESG reporting metrics, runs them through an analysis that includes benchmarking, and provides the analysis to the portcos to help them improve their sustainability performance.

Based on desk research, interviews with 35 GPs and LPs, and webinars with several hundred PE practitioners, we assessed the approaches used to assess sustainability across the investment cycle, with the aim of uncovering value creation approaches. We interviewed impact-oriented GPs as well as ESG integration GPs (the majority). We should note that our generalized findings focus on the challenges but there are GPs and LPs with sophisticated value creation approaches (many in Europe).

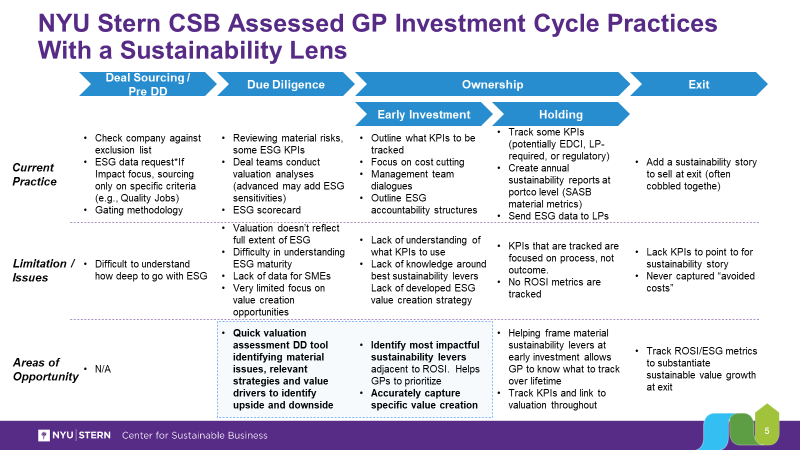

GPs look for red flags but not upside value creation

GPs struggle with approaching sustainability as a strategic value driver, instead they tend to approach it as a reporting issue. As we reviewed their environmental, social and governance, or ESG, practices during the investment cycle, we found significant opportunities for improvement during the due diligence phase and during the 100-day holding period as well as at exit (see Figure 1).

Figure 1:

During due diligence, due to a lack of data and expertise, most assessments looked solely at whether there were any major ESG risks to avoid. This means that GPs are missing the financial upside of tackling a risk that might drive improved performance (e.g. converting a problematic chemical process to green chemistry thereby reducing cost and opening new markets). They are also missing the strategic value drivers associated with a company that performs well on a material sustainability topic and how an investment could build competitive advantage (e.g. a manufacturing company has developed processes that reduce water use by half, thereby reducing cost, regulatory risk, and creating market access).

We also found challenges for the GPs and the portfolio companies after investment. During the 100-day holding period, when the GP is working with the portfolio company to set strategy and priorities, there is generally minimal focus on sustainability value creation other than a basic assessment of ESG materiality and setting up a few ESG reporting metrics to track.

Managing to ESG reporting metrics primarily through a risk lens does NOT drive value, based on other NYU Stern Center for Sustainable Business research, which finds that ESG reporting metrics are output- and process-based versus outcome- and performance-based. For example, many metrics focus on the existence of a policy, which does not drive change or value creation (e.g. the existence of a DEI policy does not mean the company necessarily has a more diverse employee base that is driving higher productivity and retention).

To improve sustainability and financial performance, the company needs to have key performance indicators as well as indicators that will track and monetize the intangible and financial benefits of the sustainability strategies and investments. That way, at exit, the GP can have a well-grounded sustainability narrative with financials. Our assessment of the investment cycle found that GPs were receiving interest in the sustainability narrative at exit but struggled to provide critical financial backup because they were not tracking it.

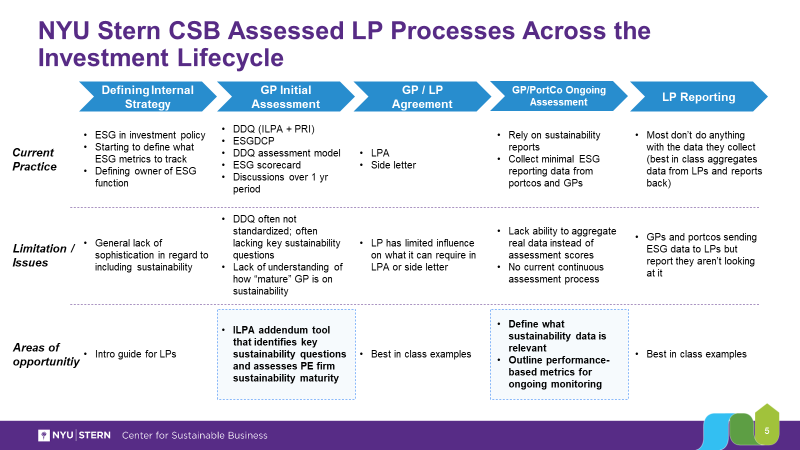

LP due diligence and ESG engagement is very basic

LPs have two major touchpoints with GPs during the investment cycle (see Figure 2) – the first during due diligence to take on the GP and its fund(s) and the second if and when they ask for/review ESG reporting metrics on the fund or portfolio company’s performance.

Figure 2:

Just like GPs, LPs tend to approach sustainability as a reporting and compliance issue, or at best risk mitigation, not value creation. During due diligence, most LPs use a 500-question questionnaire based on ILPA and PRI guidance, sometimes with ESG Data Convergence metrics added or other individualized metrics (approximately 20% of the questions are related to ESG topics). GPs often have to respond to dozens or more of these questionnaires. Both LPs and GPs report that the questionnaire responses are rarely discussed.

The LPs investment policies may include ESG requirements or they may issue a side letter with ESG requirements, primarily focused on ESG reporting requests. Many LPs will ask for ESG reporting metrics on an annual basis, either at the fund level or the portfolio company level. Both LPs and GPs report that after receiving the reports, there is little or no outreach from the LP to the GP about the data. Again, because the ESG reporting metrics tend to be process- and output-based, there is no real evidence of sustainability improvements to track, nor are there metrics presented that demonstrate how financial performance aligns with the sustainability performance.

Conclusion

Many GPs and LPs are at the beginning of the sustainability value creation journey, which creates a lot of opportunity for improving societal impact and growing financial returns. This is the first of three articles, which summarizes our overall findings for a second phase of research into private equity and sustainability value creation. The first phase of NYU Stern Center for Sustainable Business research into PE culminated in a report entitled “The Road to Responsible Private Equity,” which we reported on in ImpactAlpha last year.

The following two articles will describe the sustainability value creation tools we have developed for General Partners and Limited Partners. We will be unveiling the tools at an NYU Stern CSB conference on PE and sustainability value creation on December 12. Through our media partner, we are offering 20 exclusive tickets to ImpactAlpha subscribers. The first 20 people to use code ImpactAlpha2023 at the registration link here will get a special discount and access to this invite-only event.

________________________________________________________________________________________

Note: NYU Stern would like to thank Arthur D. Little, which provided us as a pro bono secondment to support this research, Investindustrial, which provided grant funds and expertise, and ClimateWorks which also provided a grant for the tools we are developing.

Tensie Whelan is Clinical Professor for Business and Society and Founding Director of the Center for Sustainable Business at NYU Stern.

Florent Nanse is a Principal and ESG lead at Arthur D. Little.

Julien Marchese is a Researcher at the Center for Sustainable Business at NYU Stern, and formerly a consultant for Arthur D. Little.