(Editor’s note: This months’ examination of growth expectations and fiscal issues is the second in ImpactAlpha’s four-part series on the US economy. In his first Macro Impact column, contributing editor Robert Brown addressed the US’s “first-time ever” monetary conditions. Coming soon: implications for corporations and impact investors. Drop us a line about what you’re seeing and what you need to know.)

After a year of unrelenting skepticism from investors, the Federal Reserve now admits that they are closer to achieving their mission of slowing economic growth to tame inflation, and without sacrificing employment.

Maybe.

If the assessment is correct, the Fed will have executed the elusive soft landing. If not, we still could face a recession, albeit likely a mild one.

The key to the happy outcome is the surprising resilience and strength of the labor market, which is driving increases in real wages, including for low-income workers. Real income growth is now outpacing the growth in spending, a very favorable and historically unusual dynamic. The key takeaway: consumers appear positioned to continue to support the economy, even as infrastructure spending and other sectors sensitive to interest rates contribute incrementally less to total GDP growth.

At the same time, the services sector, which employs the highest percentage of low-wage workers, is driving record levels of US corporate earnings.

The tenuous and nascent dynamic provides a basis for at least faint optimism.

Consumer-driven growth

Let’s take a step back and analyze the sensational – the November update from the Bureau of Economic Analysis that revised upward nominal GDP growth in the third quarter to an eye-popping 8.3% annualized rate. Even when adjusted for inflation, real GDP accelerated a still robust 4.9%, significantly faster than growth in the second quarter of 2.1% and 2.2% in the first (fourth quarter and year-end numbers will be released at the end of March).

That strong performance for the US economy across the board was driven by a 3.1% growth rate in consumer spending, a 10.0% growth rate in investment spending and a 5.8% growth rate in government expenditures (largely due to an 8.4% increase in defense spending).

Those are annualized rates of growth; adjusted for the size of each sector, the contributions to the 4.9% real GDP growth were consumer spending (2.1%), investment spending (1.7%, which includes 1.3% for inventory restocking), and government spending (1.0%). There’s a bit of a shortfall in that math due to rounding.

From that top line 4.9% estimate, we should deduct the 1.3% contribution from inventory restocking. The resulting “core” growth rate of 3.5% is still strong but not as hot as the top line reading. If we focus strictly on domestic activity, we see that final sales to domestic purchasers grew at a still strong but less sensational 3.0%.

The continued strength of the US economy, combined with resilience in the labor market, provided the Federal Reserve with the confidence to announce that a rate cut is “on the table” for the Federal Open Market Committee. Markets cheered the development enthusiastically. Stocks rallied hard to the end of the year, with a particular strength seen in smaller cap stocks and risk-on assets. The S&P 500 was up 25% for the year. The Russell 2000 rose 16%, advancing strongly in the fourth quarter, after lagging large cap markets much of the year.

Looking ahead, two issues remain central to the aims of many impact investors: the implications for income and spending, as well as corporate earnings; and the tension between income-supported spending and interest rate-dependent investment spending.

Rising incomes

In the current macro environment, it is rational to expect that the strength of the consumer will overcome the evolving weakness in infrastructure spending. But that is not a given, as the consumer could quickly reverse sentiment – at the same time investment spending slows under the burden of higher interest rates.

Of the three components of the GDP accounting identity – consumption, investment and government – the primary driver, by a wide margin, is consumption activity. Nearly 70% of US GDP is the result of consumer spending, and the durability of the very strong consumption activity we saw in the third quarter, through September, is a key question for investors.

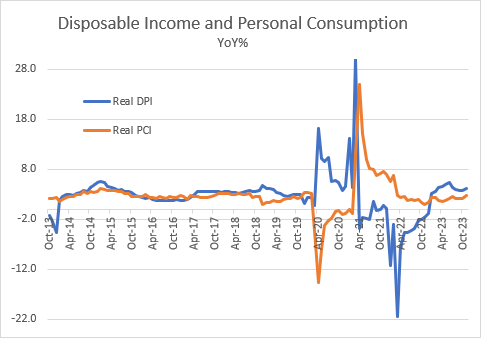

During the Covid recession, consumer spending fell dramatically, collapsing almost 15% in 2020, even as personal income accelerated by more than 30% annually due to government transfer payments made to taxpayers during the sharp recession (chart 1). The subsequent adjustment period was no less dramatic, as income dropped almost 20% annually when that excess income stopped.

As the economy normalizes, incomes are now outpacing spending growth – a very favorable dynamic and an historically unusual one. Through November, real disposable personal income had exceeded real spending for 11 months, and by a margin that appears to be ongoing.

There is also reason to be faintly hopeful about the composition and breadth of that income across all income segments.

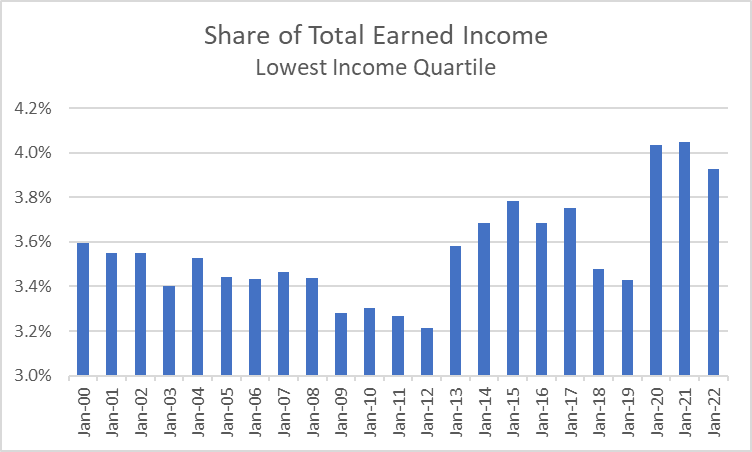

As of January 2022 (the latest available data), the share of total domestic earned income earned by the lowest-income quintile was 4.0%. That’s an unsettlingly small share, but higher than the 3.2% of a decade earlier (Chart 2). At the same time, the highest income cohort earned 47% of all income – an unsettlingly high share, but still lower than where it was a decade earlier, at 50%.

While those who have the most continue to out-earn by a wide margin those who have the least, it does appear that the lowest-income earners are gaining ground.

The wage inflation since the end of the Covid recession supports this dynamic: average hourly earnings for non-supervisory workers continues to grow above historic norms. The latest figures, as of the end of November, was $29.30 per hour, an increase of 4.3% annually.

Another important, though qualitative sign of the growing strength of labor is the rising strength of the union movement in the United States. We see this strength as an outcome of the labor market through the 3.7% national unemployment rate, which remains near post-war lows, as well as the near-record low level of continuing unemployment claims.

And, importantly, a strong labor market appears to be thriving alongside record corporate profits. Non-financial corporate profits in the third quarter of ‘23 were estimated to be $3.3 trillion annualized, 3.6% higher than the first quarter of 2023 and more than 30% higher than the pre-Covid crisis level of $2.5 trillion in 2019. The services sector, which employs more than 80% of the 134 million workers in the US, continues to drive profits growth, led by growth in retail trade, wholesale trade and information services.

More progress

This dynamic between income, consumption and profitability provides a hopeful signal for workers, as it supports a tighter labor market, particularly in those segments of the workforce where real wages had remained stagnant for too long.

To be sure, all is not well for the US worker. More progress is needed to return the US back to an economy which supports all levels of income earners with jobs that provide a living wage with dignity.

While wage gains appear healthy and sustainable, the line between healthy and “too hot” is a thin one. Wage-push inflation is still very much on the Fed’s list of concerns as they manage monetary policy toward normalization. An overheating labor market would almost certainly lead the Fed to lengthen the “pause” period, which could cause an adjustment in the path of economic growth.

And the ongoing strength in top-line GDP, driven by the consumer, must be balanced against the negative pressures developing from interest rate-sensitive sectors of the economy. Wind power, modular nuclear reactors and other capital-intensive projects have been stalled or canceled in part because of higher interest costs and inflation.

Investment spending continues to lag the growth in consumption spending, particularly in areas such as construction, both residential and commercial, as well as automobiles. And the housing market – which drives consumption of durable goods such as furniture and electronics – continues to struggle.

Finally, let’s bear in mind that GDP and, indeed, broad economic growth, remains a very limited measure of what’s truly important. As Robert F. Kennedy (the father, not the son) told students at the University of Kansas in 1968, “the gross national product does not allow for the health of our children, the quality of their education or the joy of their play. It does not include the beauty of our poetry or the strength of our marriages, the intelligence of our public debate or the integrity of our public officials.

“It measures neither our wit nor our courage, neither our wisdom nor our learning, neither our compassion nor our devotion to our country. It measures everything, in short, except that which makes life worthwhile.”

_____________________________________________________________________________________

ImpactAlpha contributing editor Rob Brown was most recently co-founder and head of impact research for Atlas Impact Partners. Previously, he was head of research at JUST Capital and led research teams at AllianceBernstein and Nomura Securities International. Earlier, he was responsible for global macro research at Morgan Stanley.