This year’s survey by the Global Impact Investing Network shows an expanding market that is becoming more cautious amid political and economic headwinds

Some 429 organizations – including fund managers, limited partners, and advisors – reported $448 billion in assets under management in 2024, up 21% annually since 2019, according to the Global Impact Investing Network’s annual “State of the Market” report, released on the eve of the GIIN Impact Forum in Berlin.

But their capital deployment dropped 30% from 2023, falling to $49.8 billion. That’s 18% below what investors themselves had projected just 12 months earlier.

The data revealed a defensive geographic shift. With nearly 70% of respondents based in North America and Europe, most new capital stayed in wealthier regions and moved toward lower-risk assets. Meanwhile, investors continue to cite inconsistent data and exaggerated impact claims as their top concern.

Respondents expect their dealflow to rebound, to $58.6 billion for 2025, in hopes that demand for climate, agriculture, and health solutions will keep impact capital flowing despite tougher macroeconomic conditions.

“The choices we make now, as a global community of practitioners, will define not only the future of the industry, but the wellbeing of generations to come,” writes The GIIN’s Amit Bouri in the report’s intro.

The State of the Market report is separate from the GIIN’s market sizing report, which last year pegged the global impact investment market at around $1.5 trillion.

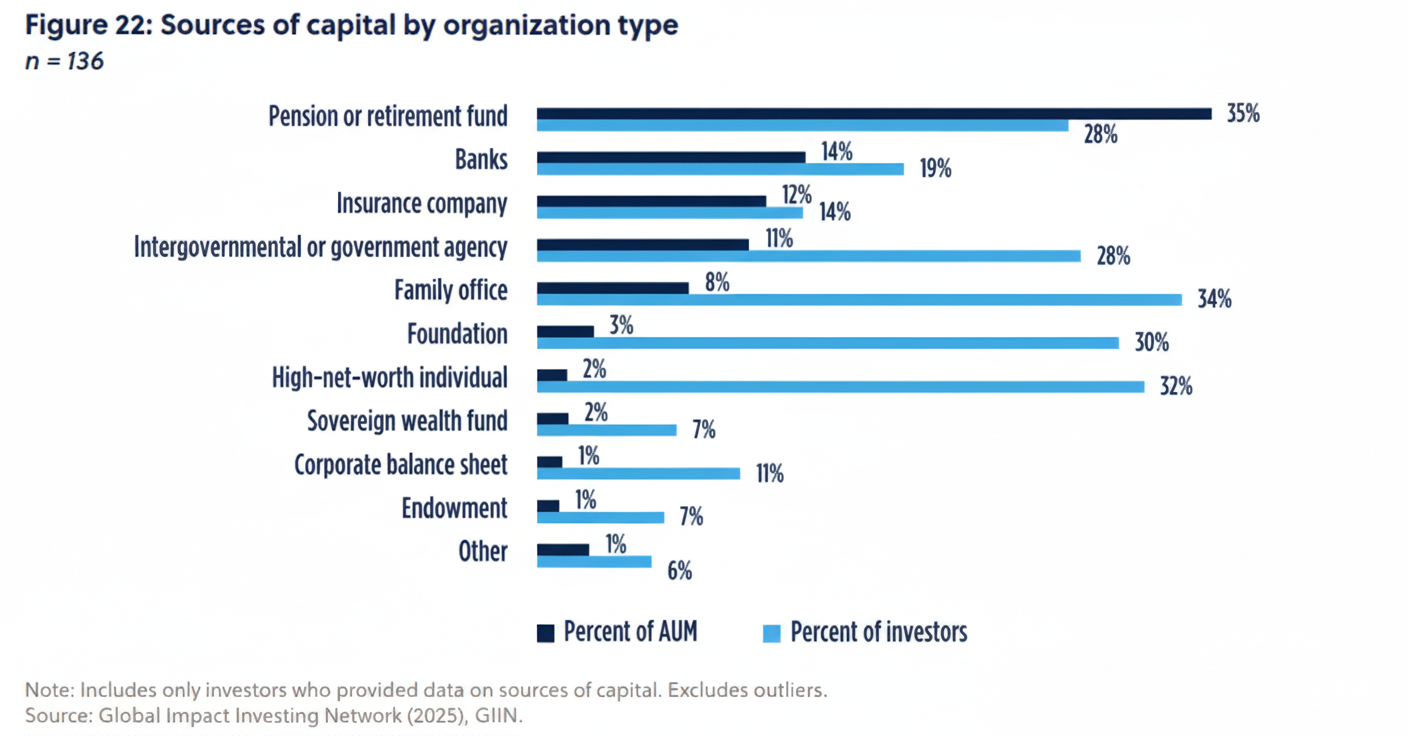

Institutional investors dominate impact capital

Pension funds, insurers, and banks now account for more than half of new reported impact capital among the respondents, overtaking foundations and family offices that once led the field. Pensions alone contributed 35% of 2024’s total, followed by banks at 14% and insurers at 12%.

The influx of institutional money has concentrated impact holdings in the market among the largest asset owners in the survey. Firms managing more than $500 million in impact assets control 84% of total reported AUM, though they represent just a quarter of investors surveyed.

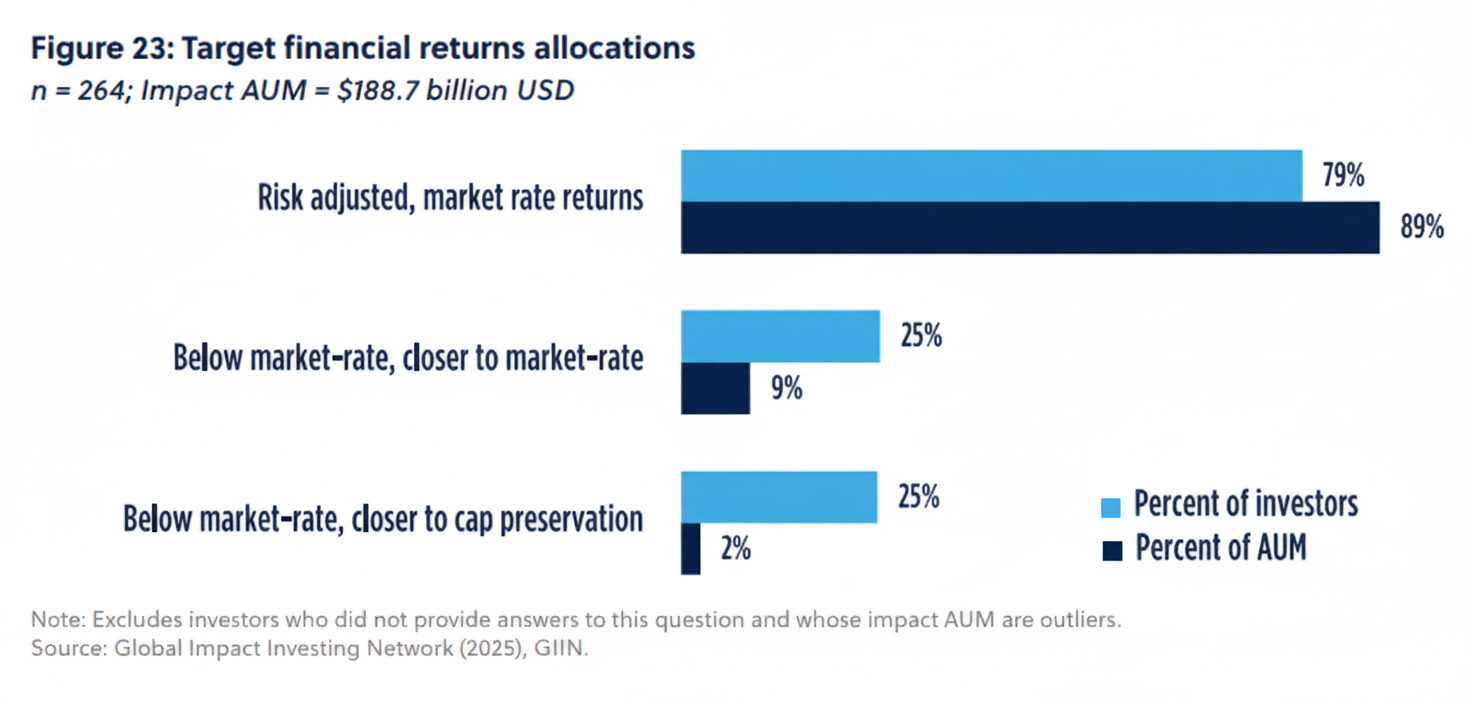

Nearly four out of five respondents now target full market-rate returns. The shift reflects the field’s growing maturity but also a pullback from higher-risk, high-impact markets where capital is most needed. About 52% of new investments are in North America and Western Europe while Sub-Saharan Africa, Latin America and South Asia attract 10%, 17% and 7%, respectively.

Even so, there are aspirations to fill these capital gaps in emerging markets. Roughly a third of respondents plan to increase allocations to South America, West Africa, and Southeast Asia over the next five years.

Climate and clean energy investments lead

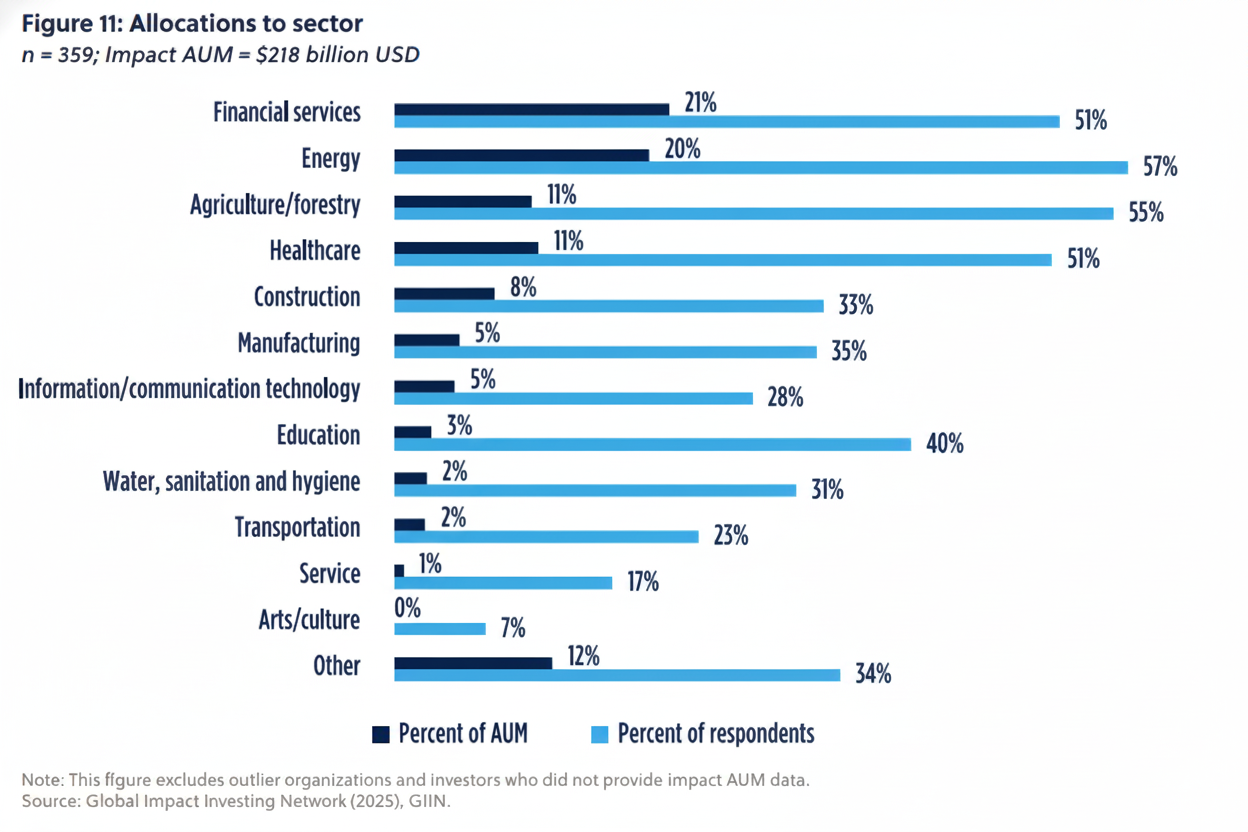

Climate investing continues to define the impact market. At least 86% of respondents invested in climate-related projects, with the vast majority focused on mitigating greenhouse gas emissions. Much of that is flowing into clean energy, now the dominant channel for climate investment, accounting for about one-fifth of total impact assets and growing faster than any other sector.

Allocations to clean energy have tripled since 2019, from roughly $10 billion to more than $34 billion, a 22% compound annual growth rate. Investors cite clear metrics, supportive regulation, and proven commercial models that make the sector attractive even in a higher-rate environment.

More than half of respondents plan to increase their energy commitments over the next five years, underscoring confidence in the sector’s growth.

Beyond climate, financial services remains the single largest sector overall among survey participants, also representing about one-fifth of global impact assets. More than half of respondents have exposure to financial inclusion, SME lending, or digital banking, and 43% plan to increase allocations in the next five years.

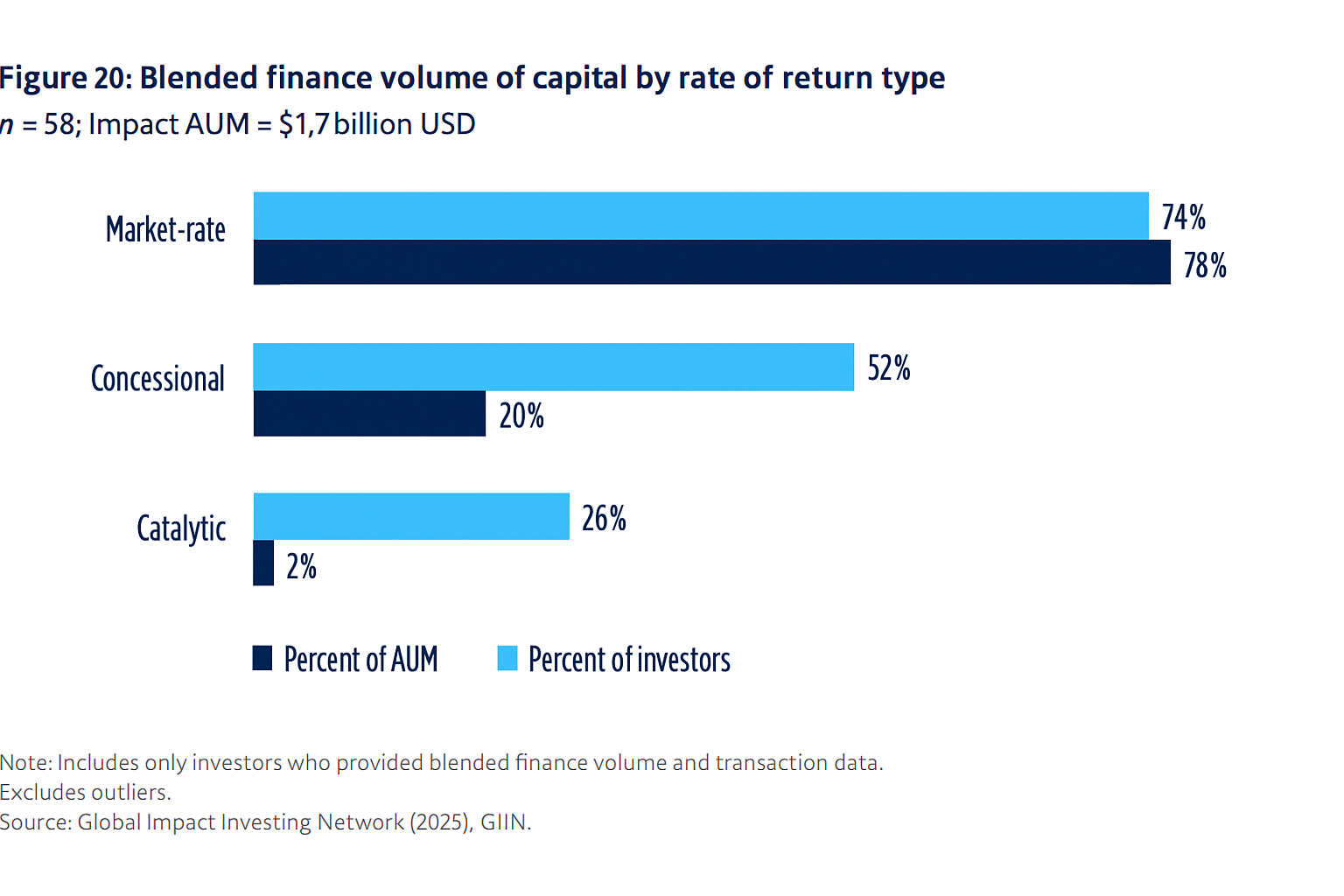

Blended finance is efficient, but nascent

Blended finance remains a small part of the impact market.

In 2024, only about a third of respondents participated in blended transactions, mobilizing $1.9 billion across roughly 4,000 deals. 78% of that capital sought market-rate returns while just 20% was concessional and 2% catalytic. The most common instruments were senior debt and market-rate equity, which together made up about two-thirds of transactions.

Those who did use blended tools leaned heavily on them to expand reach: 69% aimed to channel capital to underserved markets, 61% sought to advance the Sustainable Development Goals, and 44% used concessional capital to de-risk investments for commercial partners. Yet execution remains slow. Deals take an average of 2.1 years to close — and nearly four years for early-stage ventures.

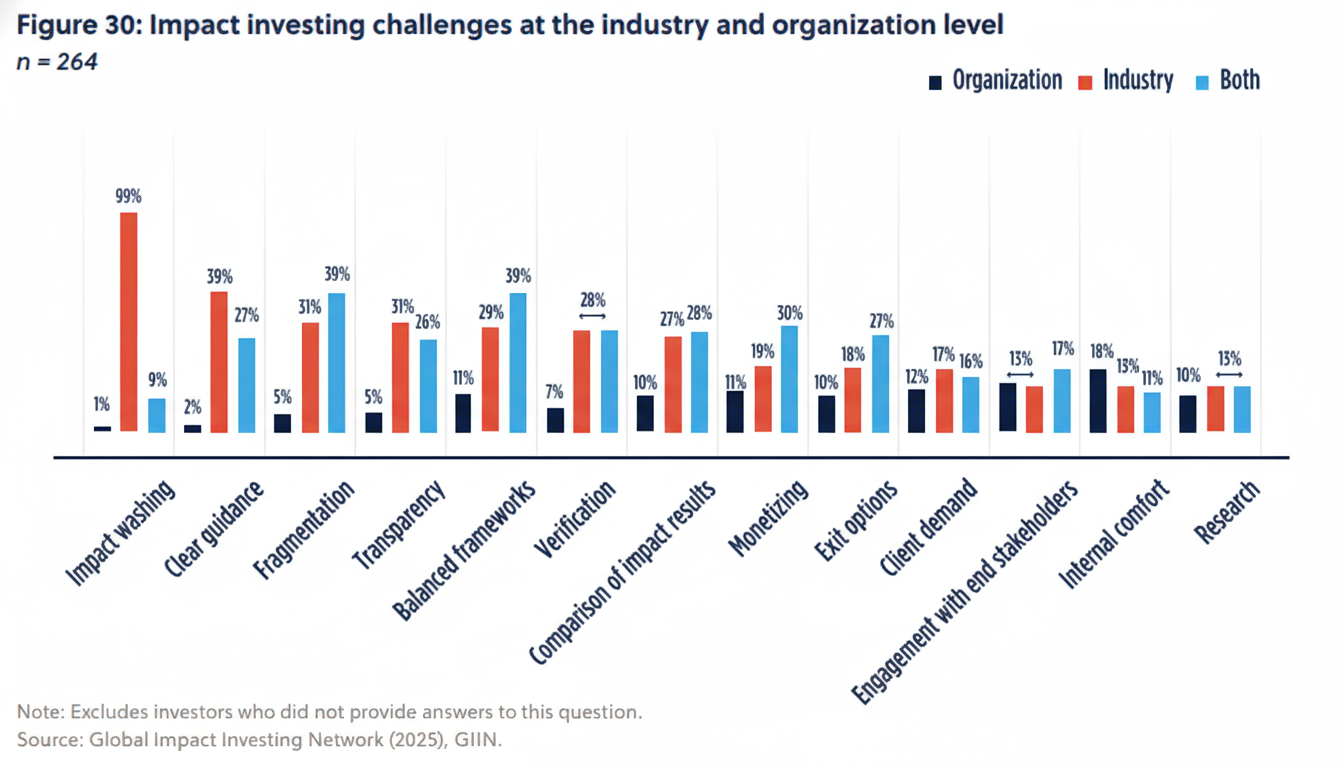

Impact-washing is a major concern

As the market grows, questions about credibility are rising too.

Nearly two-thirds of investors cite overstated or unverified impact claims, or “impact-washing,” as their top concern. And more than half say the problem has worsened over the past three years. Yet only one in 10 acknowledges the issue within their own firms.

Nine in 10 of survey takers say they’re satisfied with their impact results, and none reported performing worse than peers, a statistically improbable outcome that points to what the report calls “a persistent gap between rhetoric and reality.”

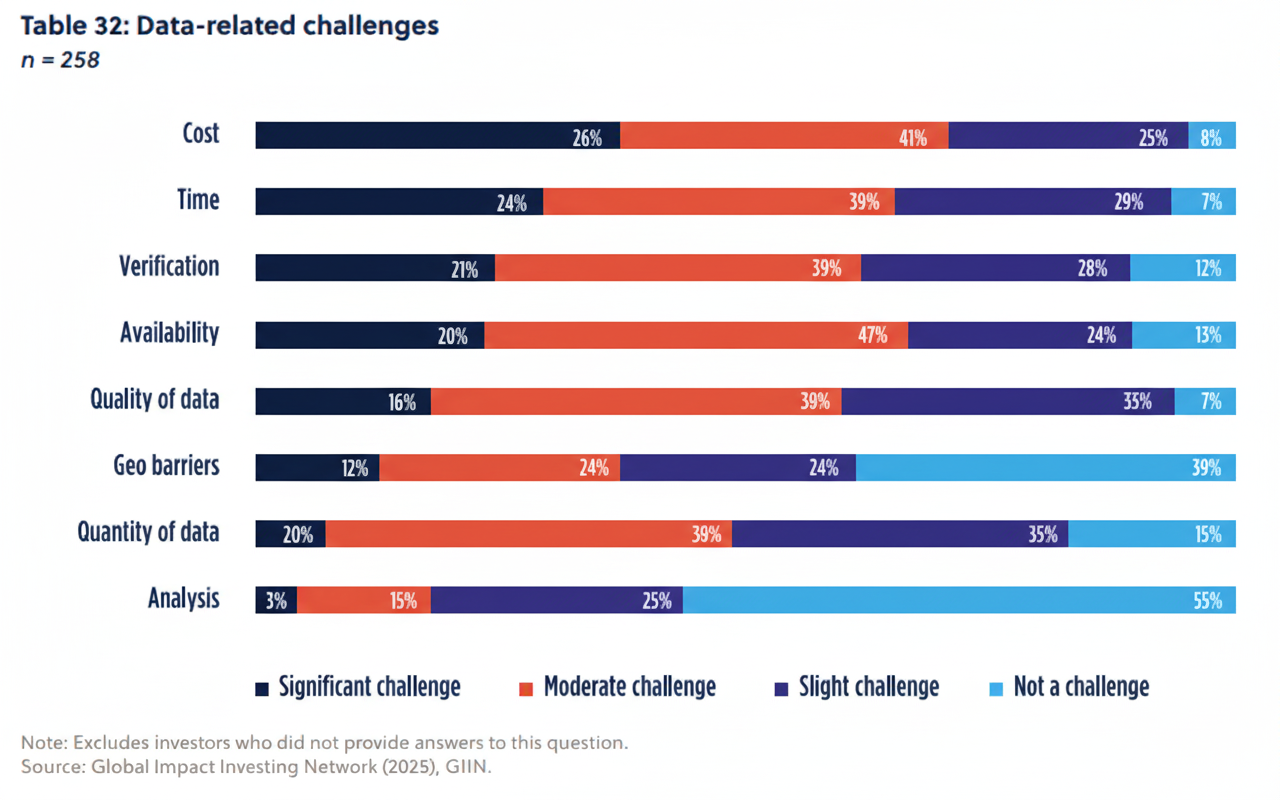

Data is a major part of the problem. 93% of respondents said collecting reliable impact data is time-consuming, and 92% cited cost as a barrier. Many recognize the need for stronger measurement but still rely on inconsistent or self-reported data. The GIIN argues that better transparency and peer benchmarking could help close this gap and build greater trust in reported outcomes.

A generational opportunity

The report reflects Amit Bouri’s call for impact investors to step up to what he sees as a leadership moment.

“Impact investors have been and remain engaged at high rates in energy, inclusive finance, agriculture, healthcare, sanitation, and the other building blocks of human life,” the report states. “In other words, impact investors are positioned well to meet this moment.”