Pump it up until you can feel it.

Pump it up when you don’t really need it.

– “Pump it Up,” Elvis Costello

The realities of high interest rates and lower liquidity are setting in for many impact investors.

The immediate questions for company business leaders, ‘How will higher rates affect the financing costs of our capital expenditures? How will higher rates impact our core business?’ And, after having thrived for (perhaps) too long on low interest rates, ‘Will impact investments now flounder for too long as interest rates remain high?’

Or, ‘Will this be the period when good businesses run by competent leaders surface and thrive?’

To understand where we might be headed requires a thoughtful assessment of the truly unique set of circumstances we are in today. This time it really is different.

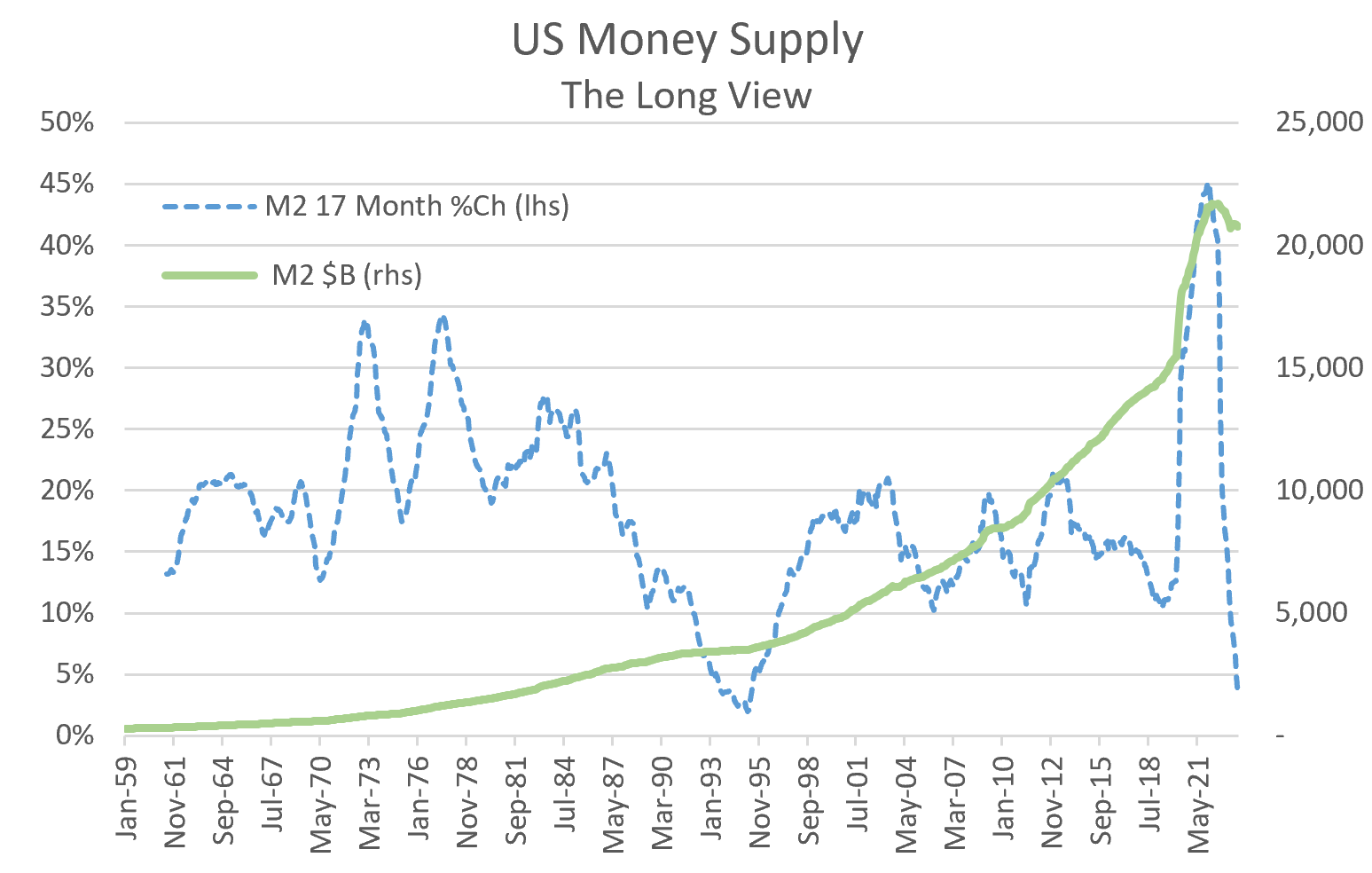

The phrase “all-time” can appropriately be applied “all-over” this monetary environment. The largest-ever nominal increase in the US money supply. The largest percentage increase in the money supply. The largest rise in consumer borrowing. The US financial system has never before experienced an injection of liquidity on that scale, or at that rate of change.

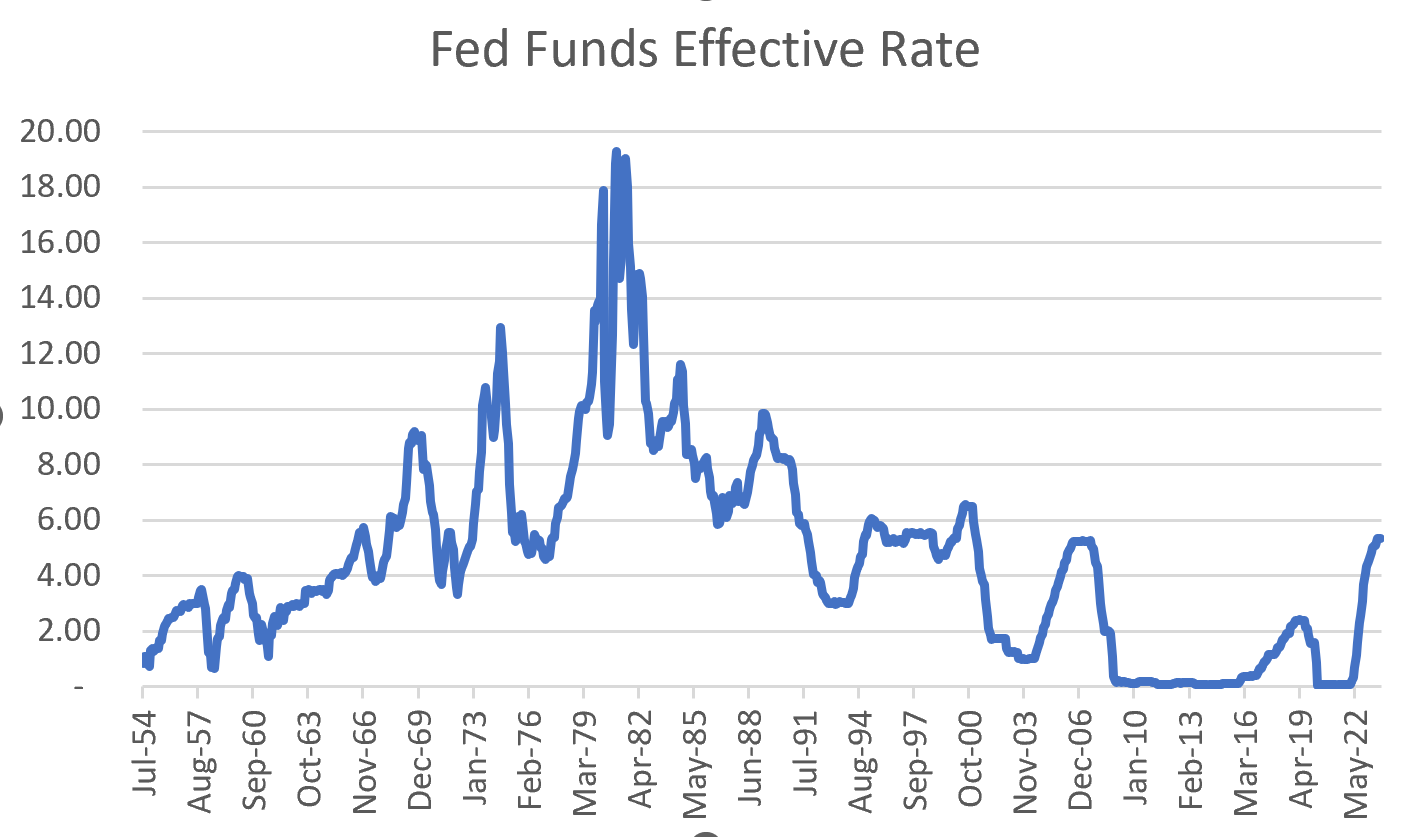

And then followed by the most rapid decline in the US money supply, ever. The fastest policy rate hike in US history, ever, and the most inverted yield curve in history since 1981.

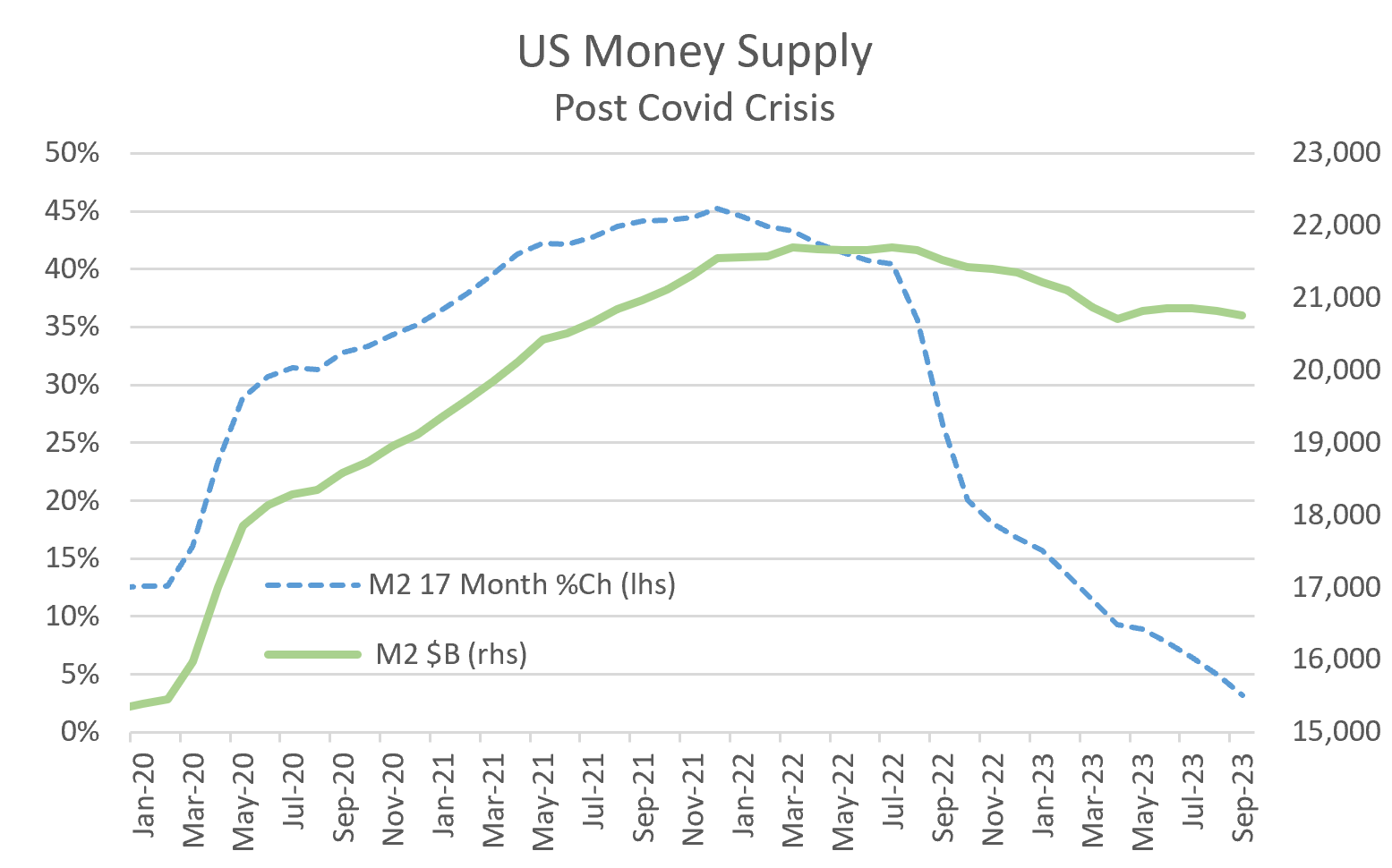

The US money supply, which can be described with an estimate of M2, or the notional total of all physical cash, bank deposits, checking accounts and CDs, (chart 1), rose from $15.5 trillion in February 2020, to a peak of $21.7 trillion in July of 2021; a rise of almost 45% in a 17-month period.

Following that rise, M2 growth has reversed dramatically and the nominal level of M2 has contracted, leading to tighter financial conditions for the consumer and businesses. In practical terms, there’s less money to lend and less money to invest. At the same time, the Federal Reserve policy interest rate in the US has rapidly risen from a low of zero in March of 2022, to the current 5.5% (more on that below), resulting in further tightness of financial conditions.

Margins and valuations

It is likely rates remain high, and it is also likely the lagged effects of a higher rate environment have not kicked in yet. Each company faces a unique set of circumstances. Typically, in the last 30 years, we have seen a rate increase affect aggregate corporate earnings six quarters after the event. The next few months will be important to watch.

In the meantime, investors are starting to see signs of stress. Smaller banks and finance companies – lenders to small companies, including many impact endeavors – have seen net interest margins and financing spreads compress. Solar installers have seen demand drop off as financing costs for rooftop solar have risen dramatically. And we have seen signs of interest rate sensitivity indirectly through the market’s lens of lower asset valuations.

During a period when we fully expect rates will be “higher for longer,” we can roughly divide an analysis of the investment landscape into three buckets:

Business models dependent on low interest rates. This includes consumer finance companies lending to riskier borrowers, small business lenders, and low-income housing construction. As rates remain high, many service providers will be squeezed out of the market by larger competitors willing to accept lower margins on services.

Businesses benefiting from low rates. Many of these companies over-earned in a low rate environment. These include traditional financial services and higher quality consumer finance, as well as capital intensive businesses like wind projects, low income housing, and student housing. Demand for services and products will likely continue to be weak as financing rates remain high, and margins will likely be lower.

Early-stage companies dependent on financing to continue their operations. Valuations for all asset classes have declined, meaning capital is more expensive, allocators more judicious and return expectations higher for any investment of early-stage capital.

Rate whiplash

The Covid and post-Covid environments have undoubtedly been unique. But often overlooked, in all of this monetary change, is that we had an equally anomalous period leading up to the monetary expansion and rate hikes, characterized by exceptionally easy monetary policy.

The pre-crisis period was supported by an unprecedented and historically easy monetary policy in the US. In 2008, during the Great Financial Crisis, in response to extraordinary strains in the financial system, the Federal Reserve set the target interest rate for reserves (the Fed Funds Rate) at zero and then pegged it there for seven years, until December 2015.

For the next five years, The Fed steadily increased the Fed Funds Rate but never above 2.5%. And then, in 2020, in response to the Covid crisis, the Fed again dropped it to zero. Essentially, a generation of home buyers, banks, developers, corporations, and investors had leveraged their assets, financed their dreams, and built their businesses expecting cheap financing.

We experienced the lowest fed funds rate, ever, and in the private sector, some of the least restrictive lending standards – ever.

In other words, historically easy financial conditions were followed by a rapid reversal into extremely tight financial conditions. Call it interest rate whiplash.

For global investors, the interest rate story has been much the same, though even longer. The world financial markets first experienced zero policy rates in 1998, when the Bank of Japan introduced the world to ZIRP, the Zero Interest Rate Policy. Until then a policy interest rate “near the zero boundary” was still a theoretical concept. Two decades later, Japan has yet to normalize rates, and in fact has been running with negative interest rates.

Following that precedent, 12 years later, were the aforementioned actions of Fed chair Ben Bernanke during the global financial crisis, which were quickly followed by Mario Draghi at the ECB. So, zero interest rates have become a standard tool in the global central bankers’ kit.

Impact playbook

The challenge is that we do not have a playbook for normalizing policy rates from the zero bound. Experience has taught us repeatedly over the last 15 years what typically occurs when policy rates remain low and liquidity is high: Accommodation leads to higher asset valuations and at the extreme, asset bubbles. What we don’t know: What will happen as investors and businesses adjust to the end of liquidity and excessively low interest rates?

For starters, in the near term, the Fed has been crystal clear that until inflation recedes to historic norms, meaning two-ish percent, policy rates will remain high. Most observers assume that when the Fed stops raising rates, they will make a U-turn. That is unlikely.

The October jobs report was fairly modest, with an increase of only 150,000, and a downward revision of 101,000 for the previous two months and a slip in the average hourly work week to a cycle low of 34.3 hours. Together with an improving inflation outlook, that gives the Fed a justification to pause, and potentially stop, raising rates.

That doesn’t mean we see easier monetary policy anytime soon. The probable scenario is that we have policy rates remaining high for some time. And we will also see the yield curve – which is the range of interest rates for all different lengths of borrowing periods – normalizing from inverted to steep. The implication is that the whole yield curve remains high.

Predicting the economy and broad macro markets is always complicated, usually frustrating, and only sometimes rewarding. The implications are broad, but the central questions that we impact investors face now is, What do we expect as rates remain higher for longer? Which businesses will likely win and which will lose? And for those businesses which remain after the monetary storm, what will the implications be on their revenue and margins, and what will valuations be?

How are high interest rates affecting your businesses and your investments? How have you adjusted your models and expectations? In coming months, Macro Impact will be exploring the new economic conditions in which impact investors and entrepreneurs are working.

Drop us a line about what you’re seeing and what you need to know.

________________________________________________________________________________________

ImpactAlpha contributing editor Rob Brown was most recently co-founder, Senior Partner and head of impact research for Atlas Impact Partners. Previously, he was head of research at JUST Capital and led research teams at AllianceBernstein and Nomura Securities International. Earlier, he was responsible for the global macro research team at Morgan Stanley.