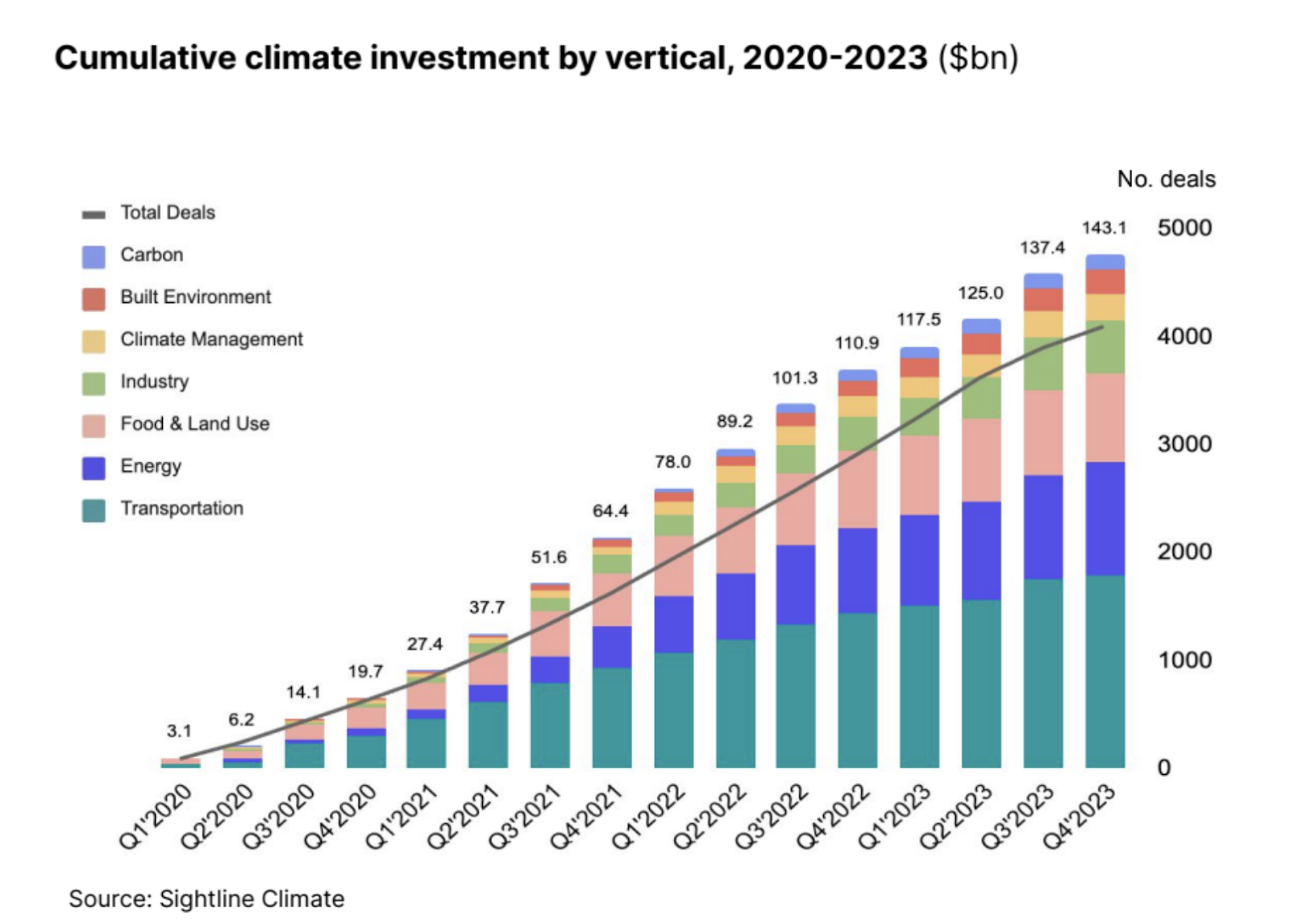

ImpactAlpha, January 5 — Batteries, green steel and hydrogen were among the bright spots for climate tech investment in 2023, even as overall climate tech private investment fell by almost a third. Behind the trend: smaller deal sizes and a flight from high-ticket, later-stage deals.

A new report by Sightline Climate, the folks behind Climate Tech VC, parses the toll that high interest rates, rising supply chain costs and a slowdown in exits had on climate tech investment in 2023.

“In 2023, Investors and founders adopted a wait-and-see approach, anticipating a realignment of valuations with expectations and a stabilization of market uncertainty,” Sightline’s Kin Zou told ImpactAlpha. “Now that interest rates are expected to come down, rules around policy incentives and regulation are emerging, and international competition has become a driving force in climate tech, 2024 is looking to be a critical year for the next phase of climate tech evolving from innovation to real-world deployment.”

What to look out for in 2024: bridge rounds, corporate acquisitions on the cheap, and continued investment in industrial decarbonization.

Here are some of the highlights from Sightline’s Climate Investment Trends report (and check our ImpactAlpha’s own year-end climate outlook):

Batteries

Battery manufacturing and recycling reigned supreme last year, attracting some of the biggest hauls even as overall EV investment declined. Battery investments rose from $979 million in 2020 to $6.2 billion in 2023, representing 58% of all transportation-related investment. As with other big-ticket deals in 2023, they are often catalyzed by government funding.

Redwood Materials, a Nevada-based battery recycler that has emerged as a key player in the US supply chain for lithium-ion batteries, hauled in $3 billion in investment last year. That included a $2 billion loan from the Department of Energy’s Loan Programs Office and $1 billion in equity from Goldman Sachs, T. Rowe Price, and Capricorn.

In Europe, Stockholm-based battery manufacturer Northvolt raised $1.6 billion in two funding rounds in 2023. Since 2021, Northvolt has raked in close to $5 billion from investors and has secured tens of billions in contracts with customers such as Volkswagen.

The action should continue in the year ahead. Battery startups are innovating around new materials and chemical processes that are lighter weight and don’t rely on rare materials, as well as recycling processes to fortify supply chains. And policy makers in the US and elsewhere are encouraging domestic production to help supply the 145 million electric vehicles that could hit the road by 2030.

FOAK funk

The path to commercialization for climate tech startups is marked by demonstration plants and first-of-a-kind, or “FOAK,” facilities. Those capital-intensive projects typically require $100 million to $500 million per deal, and are often the last fundraise before startups are able to attract non-dilutive funding, as Sightline points out.

Nonetheless, funding for these critical projects (and the broader Series B+ category) fell by more than half to $10 billion in 2023. “2023 had too many open questions, with investors and startups adopting a wait-and-see approach,” writes Sighline.

As rates cool and regulatory rules for everything from the Inflation Reduction Act to the EU’s Carbon Border Adjustment Mechanism come into focus, crucial FOAKs and demo’s could be back on track in 2024.

Industrial Decarbonization

From industrial heating and cooling to cement and steel, industrial processes are among the thorniest to green. But investors see opportunity. Investors poured the most money ever into industrial decarbonization in 2023, with 46 deals totaling $3 billion, up 13% from 2022.

Behind the breakout performance: a 430% rise in green steel investment. And behind that rise: H2 Green Steel’s whopping $1.6 billion raise.

“Industrial decarbonization will continue to grow, with growing interest across mining, steel, cement, and industrial heat taking advantage of incoming regulations,” like the EU’s CBAM, says Sightline.

Investors

Sightline counts some 2,787 private climate tech investors across seed and pre-seed to growth stages. That’s more than double the 1,225 investors in 2020. While new investors continue to enter the market, they did so in fewer numbers last year.

Venture capitalists make up the largest share of investors, by far, at every stage, but they have more competition in later stages, particularly from corporate VC, private equity, infrastructure investors and institutional investors.

Among the most active investors: Lowercarbon Capital and Breakthrough Energy Ventures among climate generalists, Siddhi Capital and S2G Ventures in the food and land use sector, while Temasek led in transportation deals.

Corporate checks

IPO windows may be narrowed to a slit. But corporations have been snatching up small, struggling climate tech companies and integrating their capabilities to gain more foothold in the market. Corporations have been the most active acquirers since 2020, participating in 41% of all acquisitions.

Shell and BP lead the pack, having collectively acquired a dozen climate tech startups since 2021. Early last year, Shell completed its $2 billion purchase of Danish biogas producer Nature Energy. The oil and gas giant also acquired EV charging company Volta, and Nigeria solar energy provider Daystar Power.

BP’s recent acquisitions include Texas-based renewable natural gas producer Archaea Energy in a deal valued at $4.1 billion and California’s Amply Power to build out electric vehicle charging in the US.

Shake out

The challenging economic conditions took down several one-time high-flyers, particularly in the EV and indoor farming markets. Seven electric automakers declared bankruptcy or went belly up in 2023, including Proterra, Lordstown, and Electric Last Mile Solutions. Indoor farming startups also struggled with rising costs, notably Infarm, Upward Farms, and Aerofarms.

Meatless Farm’s bankruptcy illustrated the broader problems plaguing the alternative protein space. It’s a reminder that when money is easy, everything looks easy.