If you had to choose a single industry that Donald Trump promised the most to in the run-up to the election, oil would top the list.

In a private Mar-a-Lago dinner, he told oil executives that donating $1 billion to his campaign would be a “deal” because they would more than recoup that in savings, reduced taxation and deregulation.

Then, delivering on this promise, one of the executive orders he signed on his first day in office was to declare a “National Energy Emergency” to push for more oil and gas drilling and heavily boost fossil fuels. “Drill, baby, drill” is basically a catchphrase of his at this point.

So, seven months in, is America “drill, baby, drilling?” Did oil executives get what they paid for? Is an industry notorious for booms and busts riding federal policy tailwinds into its next boom?

No. At least not yet.

Underperformance and layoffs

Here are some recent energy industry headlines:

- “ConocoPhillips is Latest U.S. Oil Producer to Announce Major Layoffs”

- “ConocoPhillips layoffs an alarm bell for energy industry”

- “Houston-based Chevron to lay off up to 20 percent of its global workforce, according to reports”

Those are definitely not the headlines you would see from an industry poised for boom-time.

What about oil stocks? Layoffs aren’t always a bad thing in the stock market, and sometimes investors can reward companies for cost-efficiency. Here, the news is head-scratching as well.

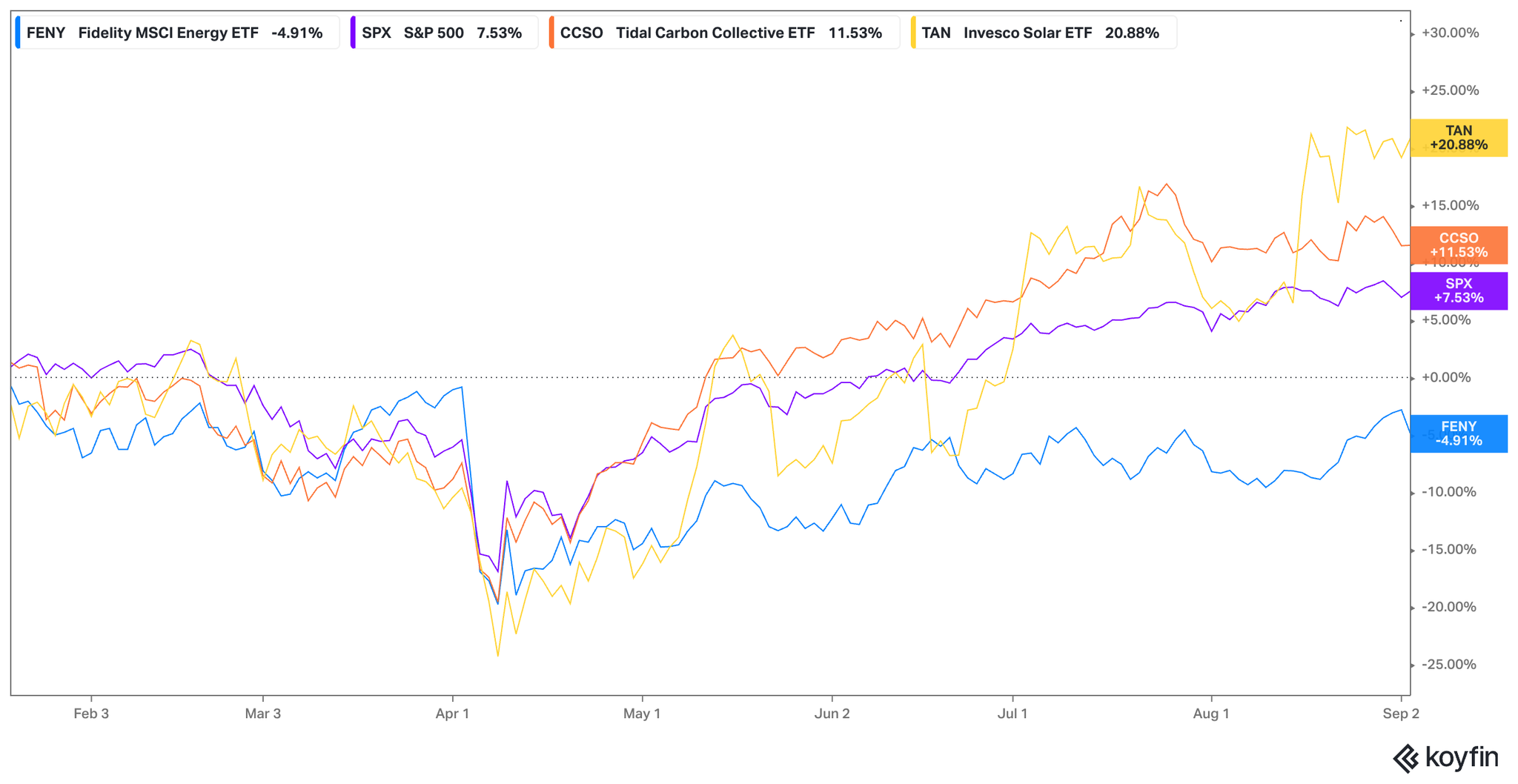

Here’s how FENY (an ETF that tracks the US energy sector, in blue), the S&P 500 (in purple), CCSO (our climate solutions ETF, in orange), and TAN (the US solar stock sector ETF, in yellow) all have performed since the day Trump declared the “National Energy Emergency” on January 20 through September 3.

As you can see, TAN (US Solar sector) has performed much better than FENY (US Energy sector), and you’d expect that to be reversed.

Here at Carbon Collective, we wanted to dig into exactly what is going on. Why are oil stocks down under Trump? Why are companies like Chevron and ConocoPhillips conducting major layoffs after the most industry-friendly executive comes into office? And what, if anything, does the rise of climate solutions have to do with it?

Houston, we have a (demand) problem

You can “drill, baby, drill” all you want, but if demand isn’t there to absorb what you pump out of the ground, you’re going to have a problem. And oil is facing a demand problem in 2025.

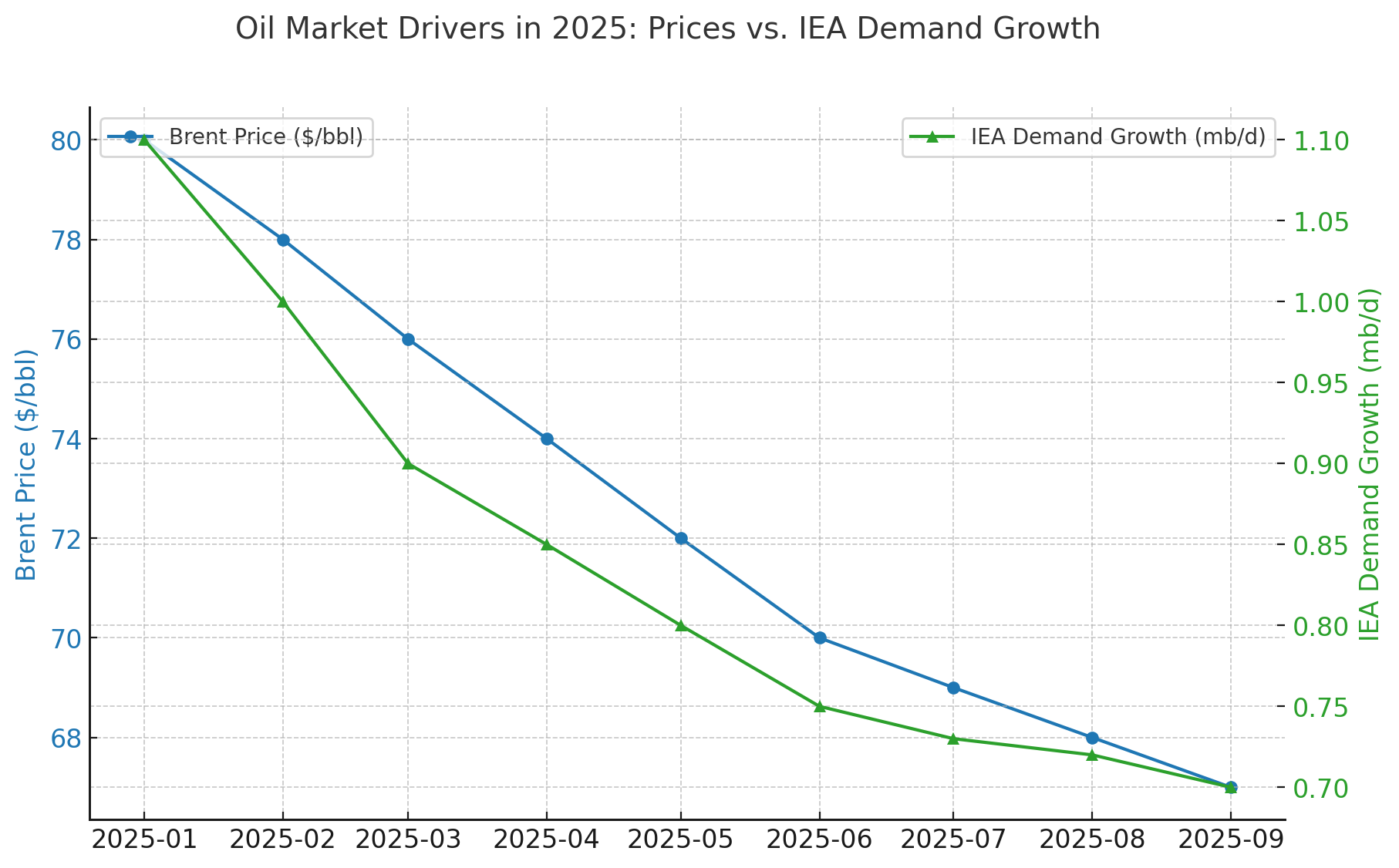

Here’s a graph from the beginning of the year to now tracking oil demand growth (in green) and the price of crude oil (in blue):

It paints a pretty clear picture.

So, what has been driving down demand for oil? Ironically, Trump himself. According to the IEA’s 2025 report on oil markets, “Heightened trade tensions and uncertainty have weighed on the world economy and, by extension, oil demand growth.”

The unexpectedly high and arbitrary barrage of tariffs introduced by the Trump administration in April had a big negative impact on his favorite industry.

The tariffs and ensuing business uncertainty have introduced a real drag on economic growth. Analysts estimate that the tariffs will slow down US GDP growth by 0.5%. And (unfortunately) oil demand and GDP growth are still heavily correlated.

But let’s not give Trump all the credit. There are other trends at work.

First, there were some situational events that affected oil demand:

- The winter was mild in the northern hemisphere – maybe a sign of things to come in a warming world.

- The summer was cooler than expected in parts of Asia and Europe, reducing the need for oil-powered “peaker plants” that kick in during high demand.

- Construction growth in China was a lot lower than initially projected.

But second, we are seeing the impacts of real structural changes to our global energy system:

- High EV adoption in China and high fuel standards in Europe are pushing down demand growth for gasoline.

- The oil and gas price shock of 2022 has pushed more emerging markets towards renewables, particularly solar.

- Petrochemicals (largely plastics) are also showing signs of slowing growth. China’s demand has peaked and the EU has banned single-use plastics. Maybe peak plastics is in sight?

- China is pushing for its own energy security by rapidly building out its renewables (yay!) and coal (boo!) fleets, reducing its demand for foreign oil and gas imports.

It’s pretty clear that the oil industry has a demand problem. Some of it is likely temporary, but other parts seem pretty sticky.

But this is far from the first time the oil industry has faced a demand problem. The answer from the industry should be obvious, right? Restrict supply and bring prices back up. So why isn’t the industry doing that?

Saudi Arabia: Playing the long game

For decades, Saudi Arabia and the broader OPEC+ cartel of national oil producers were the biggest players in the international oil industry. This gave them enormous power and influence in the world, most famously seen during the oil embargo of 1973.

But with the fracking revolution, the mantle for the largest producer of oil in the world passed from Saudi Arabia to the United States. US oil producers were able to unlock massive oil deposits across the country, but particularly in the Permian basin in Texas.

But fracking has a problem. It’s expensive. To drill a new well in the Permian basin, extract oil, and sell it, an oil major needs oil prices to be above $62 a barrel to break even. As of September 4, the price of crude oil is around $63 a barrel. The profit margin is gone.

Permian drillers are getting hit by the tariffs, too. Each fracked well uses many thousands of feet of high-spec steel piping specifically designed for the industry. That piping is generally built outside of the US.

So, barring some kind of direct subsidy from the government, there’s no way that US Permian drillers can “drill, baby, drill” in this environment. At least not any new wells. But you know who can? Saudi Aramco.

There is a reason Saudi Arabia is so rich. It is sitting on the world’s largest supply of cheap and easy-to-access oil. No fracking needed. The Saudi oil fields have high pressure with easy geology and they have already built all the necessary infrastructure to transport and refine it. The breakeven price for Saudi oil is only $20 a barrel.

In an era of international strongmen flexing their economic and military might, the Saudis and OPEC are happy to demonstrate to western oil majors that the very viability of their business model requires the Saudis’ blessing.

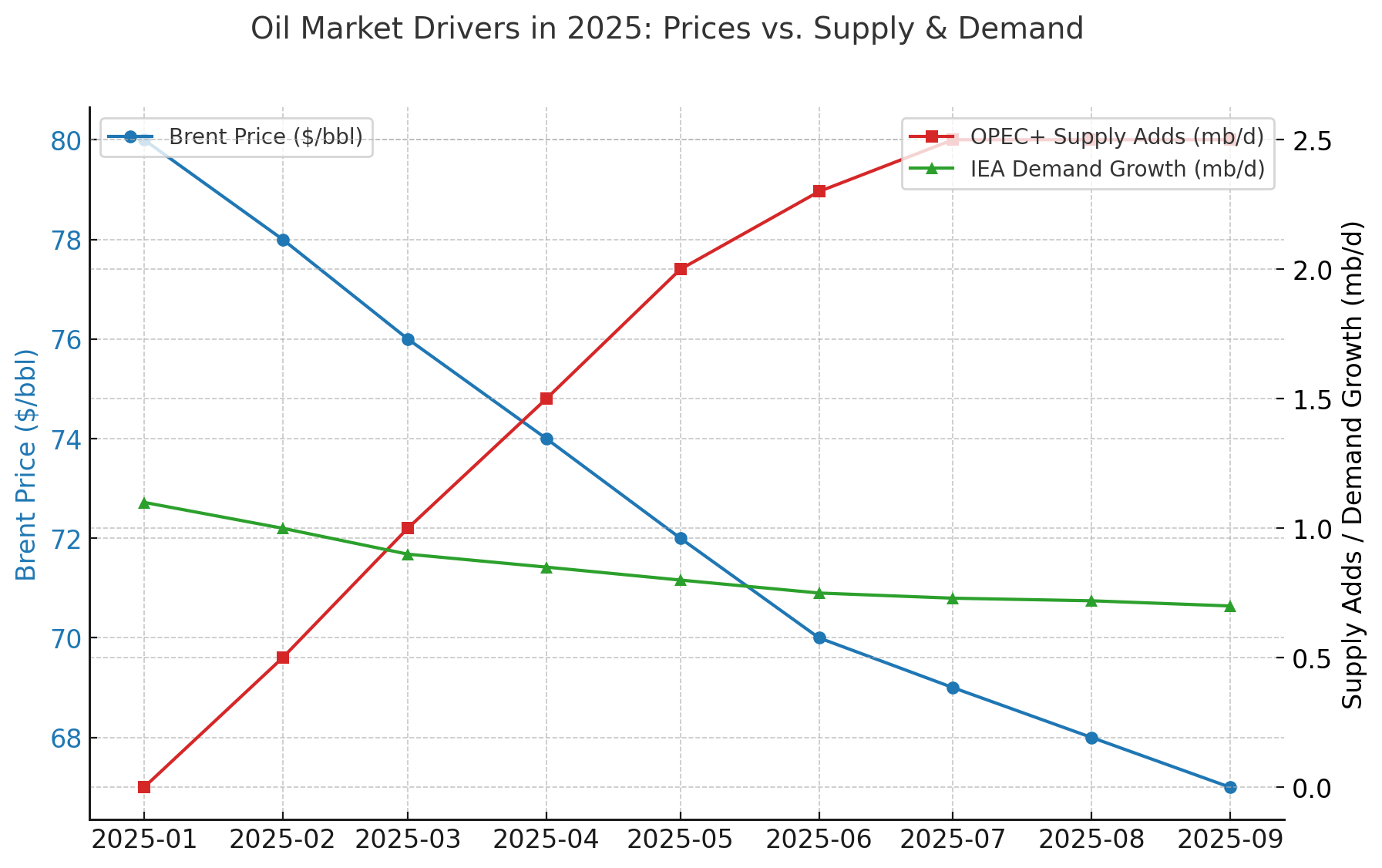

Remember that graph of crude oil price and demand falling together? Well, here it is again, but with OPEC’s supply additions layered on top, in red.

At the end of the day, the price of oil comes down to the simple economics of supply and demand. With demand falling, the Saudis and OPEC saw an opportunity to embrace the glut and play the “long game.” For in a race to the bottom on price, there’s just no way the US can compete. And there’s a world where the Saudis are just getting started. This recently popped up in my newsfeed:

The bottom line: oil executives may have thought they were buying a boom, but demand headwinds and OPEC’s leverage have left the industry on shaky ground. It’s trends like these that make us stand behind our oil-free portfolios as fiduciaries.

Zach Stein is a co-founder of Carbon Collective. ImpactAlpha has partnered with Carbon Collective to provide a monthly analysis on how individuals, companies, and organizations can incorporate the realities of our changing climate and energy systems into their investments. The analysis originally appears in Carbon Collective’s newsletter. All content is solely for informational purposes and should not be used as the basis for investment decisions.