The fossil fuel industry made a big “investment” in supporting Trump’s 2024 election. So, 10 months post-election, what kind of return on investment were they seeing?

At least for oil, 2025 has not been a good year, as we found. Their stock prices are down. Demand is relatively flat as oil prices hover near or below the breakeven price for drilling new wells. Instead of unleashed “drill, baby, drilling,” the industry has been quietly contracting to seek greater efficiency with the wells and infrastructure they already have.

But oil is just one of the three major fossil fuels, and each of the other two, natural gas and coal, has its own set of tail and headwinds.

So, for part two of this series, we dig deep into how the US natural gas industry’s investment in Trump 2.0 is going sideways. Maybe a bit better than oil, but far from a slam dunk.

How has the US natural gas industry fared under Trump 2.0?

Thanks to the fracking revolution in the US, the price of natural gas has been relatively cheap since the early 2010s.

The US is the leading natural gas producer in the world, generating about 25% of global supply. The only other country that is close is Russia, which generates about 20% of the global supply. Unlike oil, the US is far closer to a monopoly player on gas.

So, under Trump 2.0, are we seeing a revolution of “drill, baby, drilling” like we saw in the initial fracking boom?

Has the cycle swung from Biden-bust to Trump-boom?

Are natural gas executives and investors raking it in?

No.

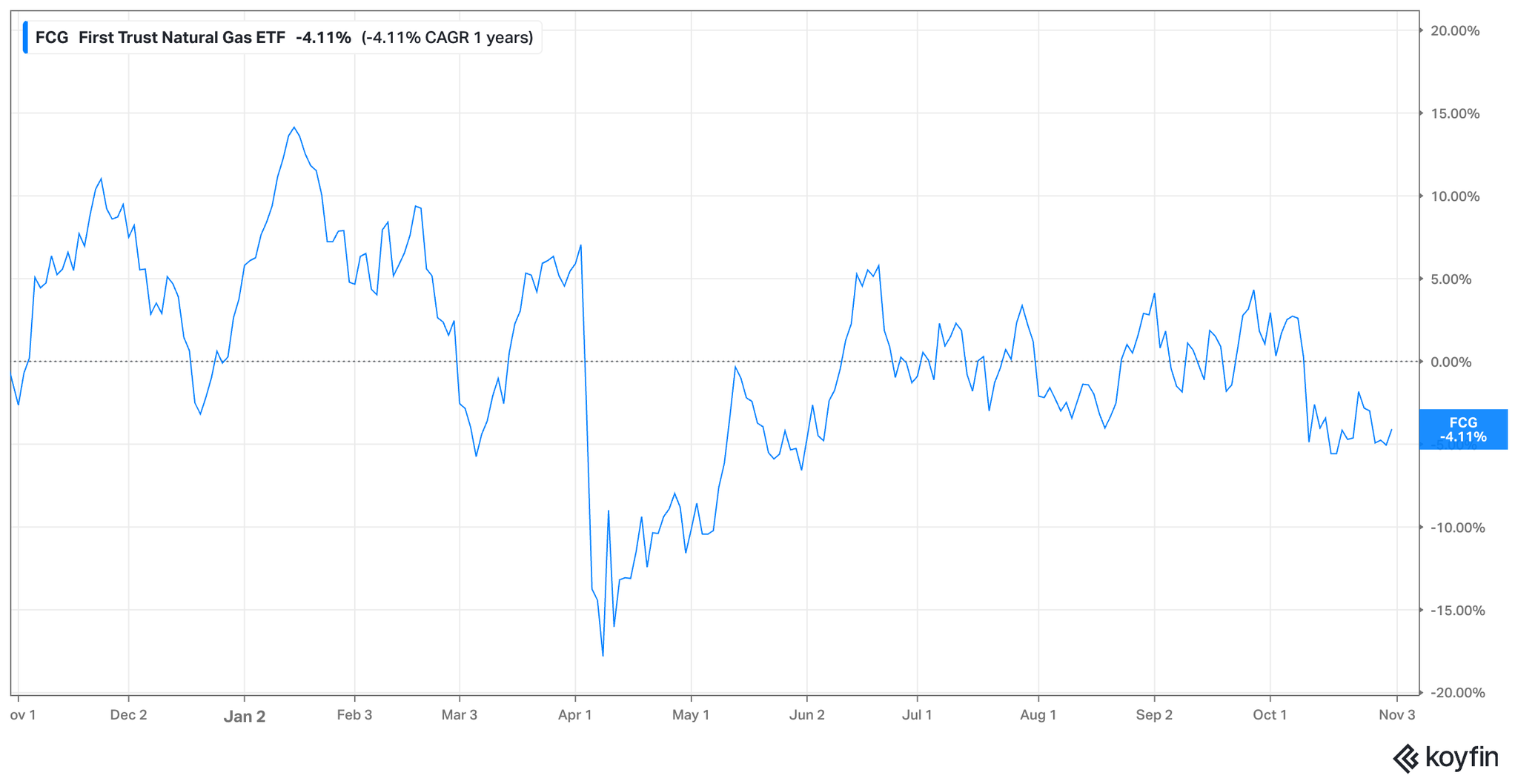

Let’s start with that last question. Here’s what the US Natural Gas equities ETF has done over the past year (so beginning right before the 2024 election).

Equity prices for natural gas drillers, refiners, and shippers as a whole have broadly fallen over the past year, in spite of the overall stock market rising.

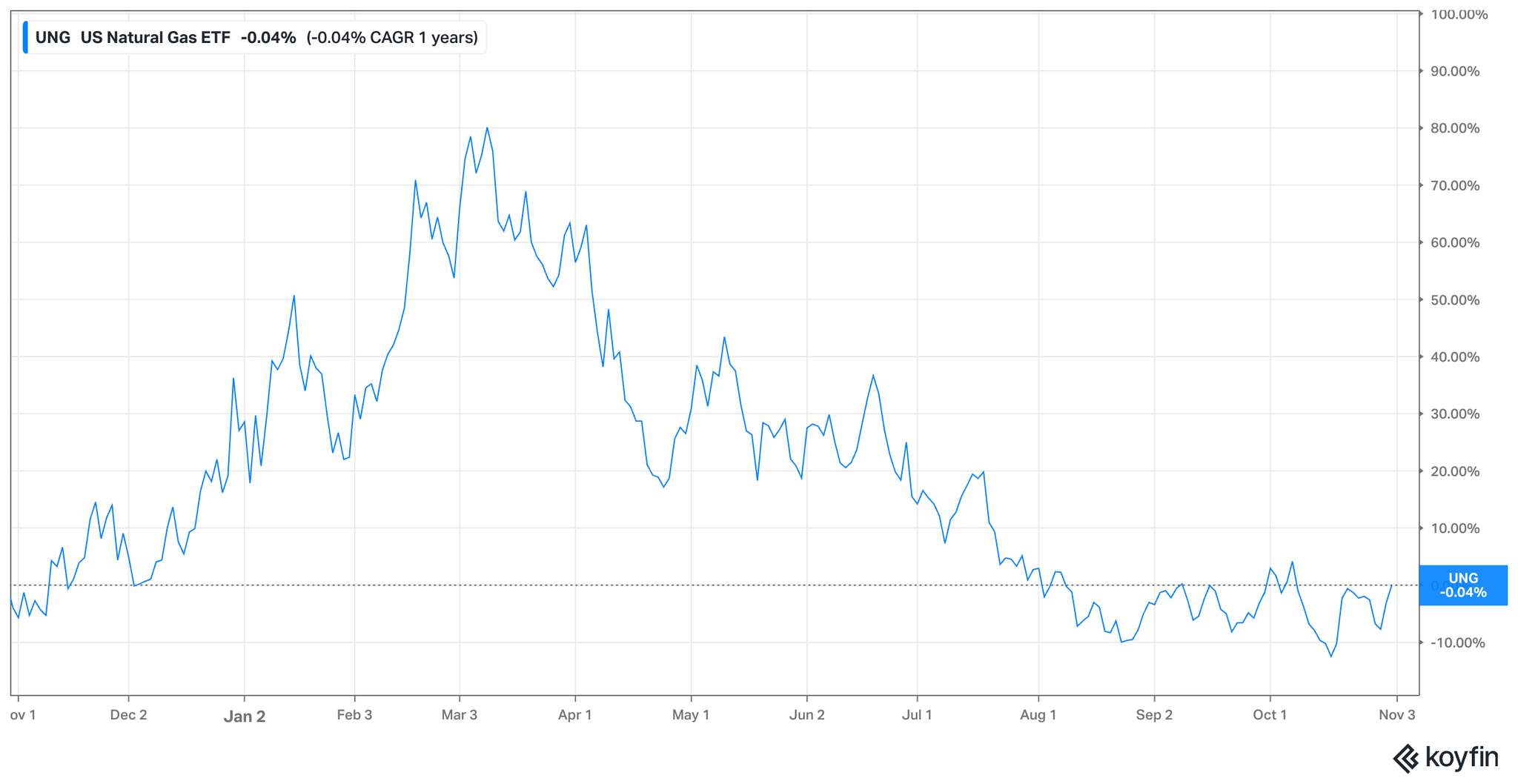

The same is true for investors looking to bet on US natural gas futures. UNG, the natural gas futures ETF, had a big rise at the beginning of the year, but is now basically flat over the year:

So what happened?

Why aren’t we seeing tangible signs yet of the natural gas industry’s ROI for helping elect Trump?

The answer… is interesting.

Profitability problems

The US gas industry has a big problem: It has really struggled to ever be that profitable in the fracking, shale revolution era (which stretches from the 2010s until now.)

It’s not cheap to use advanced horizontal drilling technology, then force a bunch of water down the well at high pressure, and then capture and clean the stuff that comes back up.

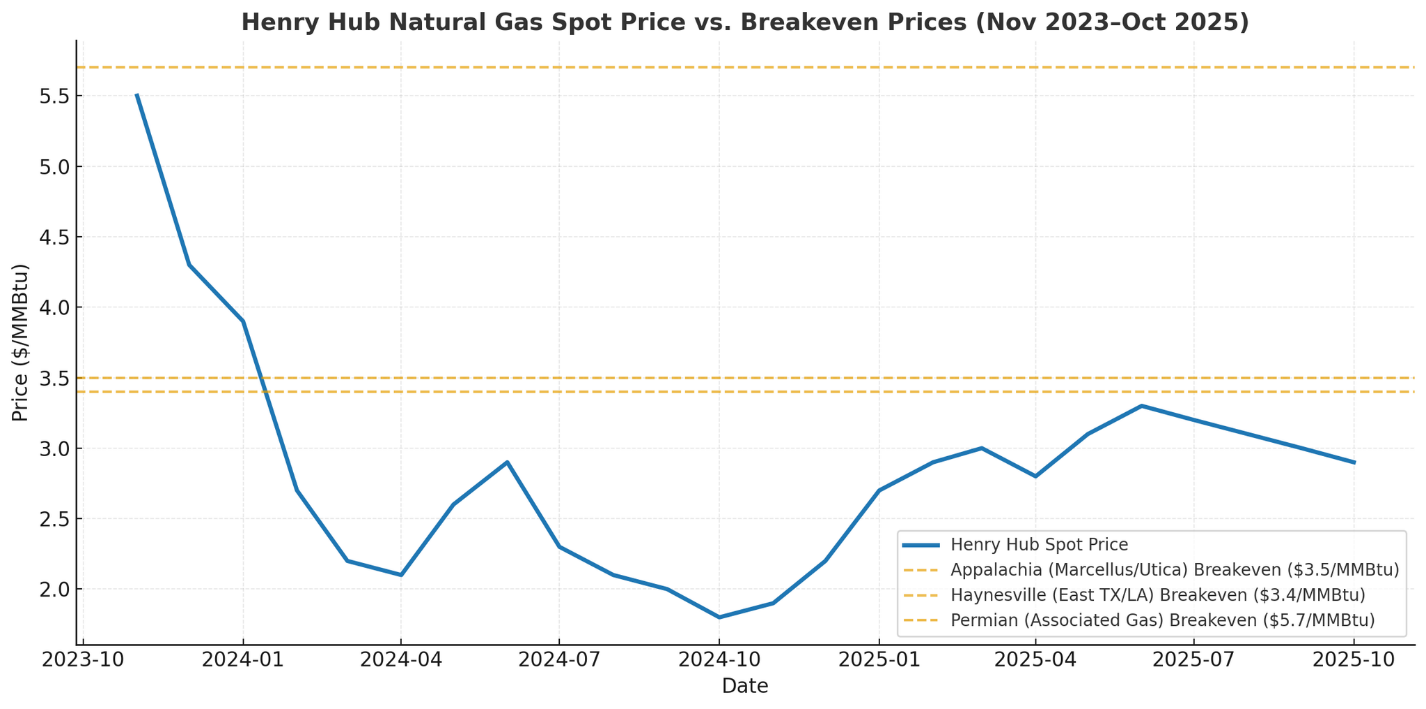

Depending on where in the country you are, these costs combined require a breakeven price of the end product, natural gas, to be above $3.40/MMBtu. (One MMBtu = about the amount of gas used to keep a home heated overnight during winter in a cold region of the US).

The wholesale price of gas is tracked by the government and is called the Henry Hub Natural Gas Spot Price. It’s the main number that will ground that exploration.

And the problem for “drill, baby, drill,” well, it’s just not profitable right now:

The blue line here is the price of gas in the US, and the yellow lines are various estimates of the breakeven price required to generate a profit for drilling new wells in various regions.

As you can see, it has not been profitable to drill more since 2023.

This has left the gas industry in a similar kind of bind as the oil industry under Trump: it’s still profitable to keep working existing wells, but not profitable to expand. This has left the industry in stasis to some extent, which we can see reflected in their stock prices.

But unlike oil, the US natural gas industry may have a white knight waiting in the wings: Europe.

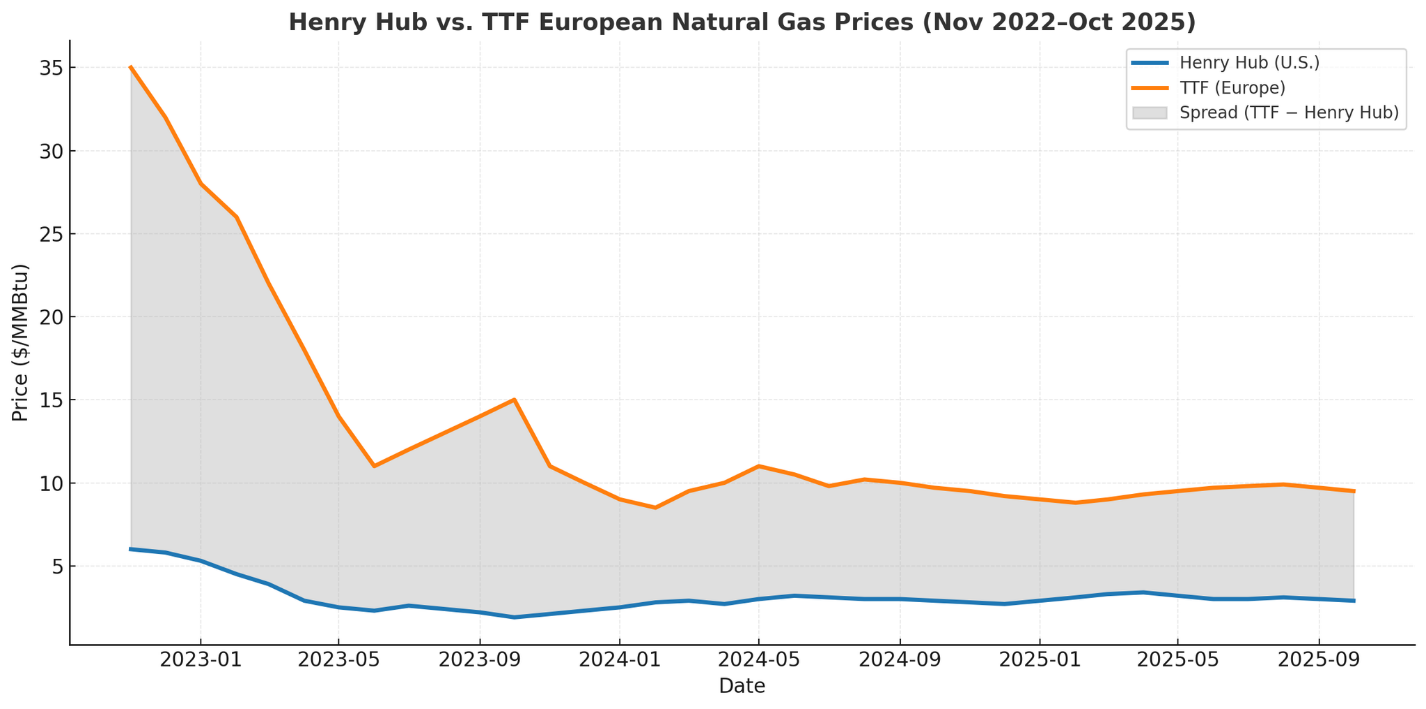

You know who pays WAY more for gas than we do here in the US? Europe, particularly in the wake of Russia’s invasion of Ukraine.

Here’s the US spot price for Gas over the past three years, mapped against the price paid in Europe.

As you can see, the spread was pretty crazy back in January of 2023. What cost $6 in the US cost $35 in Europe!

But since then, prices seem to have flattened out, with 1 MMBTu in Europe costing around $10 in Europe and something like $3-4 in the US.

That spread, the ability for US gas producers to take advantage of price arbitrage between US and EU (and to some extent other regional) price variations, is the bet the US natural gas industry is making.

Today, something like 20% of US natural gas is exported. If the industry is able to get that up to 40%, the resulting competition over US gas could result in domestic prices rising and remaining above break-even levels going forward.

“Liquify, baby, liquify”

So why aren’t US gas producers simply exporting more natural gas today?

They would if they could! But exporting natural gas is not a switch that can be flipped overnight.

You need a lot of big pipelines. And special ports. And special facilities to turn natural gas into LNG or liquefied natural gas, and then the same infrastructure on the receiving end to “unliquefy” and transport that gas to its final destination, where it will be lit on fire and immediately need to be replaced.

LNG just needs special stuff. Here’s what an LNG ship looks like. It’s not a normal container ship, but an entire, comically shaped ship just built to transport LNG:

Which brings us to the title for this section. The US natural gas sector can’t really do any more “Drill, Baby, Drilling” until it successfully does more “Liquefy, Baby, Liquefying.”

This is the big bet the natural gas industry is making under Trump: that the new administration would reverse the Biden administration’s efforts to delay their buildout of LNG infrastructure.

And, so far, this investment really does seem to be paying off, since literally day one of his presidency:

These are the three big wins for the natural gas industry with Trump as president:

- Smooth sailing to get new LNG infrastructure approved.

- Little fear of environmental review holdups for more drilling or pipelines when the industry is ready to build new ones.

- Unrelenting attacks on gas’s greatest competitor in the country: renewables.

So why aren’t natural gas stock prices soaring along with gas futures?

Well, the president also did something that could/maybe throw a giant stick in the wheel of the LNG expansion plan: Liberation Day.

Tariff policies introduce uncertainty

On April 2nd, 2025, Trump famously announced a new tariff policy that made absolutely no sense. This not only sent stock and bond markets reeling, but it also significantly undermined the global perception that the US was a good trading partner.

Since then, things haven’t gotten better. Trump doubled down on tariffs. Announced a pause. Targeted China. Made a deal with China. Flipped out because an ad in Canada used a Ronald Reagan quote against him…

And while such activity may generate some near-term gains for Trump and may even help the natural gas industry (Trump did get an agreement in principle for the EU to buy more LNG from the US in exchange for lowering tariffs), it introduces obvious motivations for America’s trading partners to add redundant sources of key inputs, like LNG. Which leads us to the problem Trump has introduced for the natural gas industry:

The industry needs to significantly increase exports of natural gas in order to justify drilling more in the US.

Those exports require major buildouts of capital-intensive infrastructure that turn natural gas into LNG and can ship it.

That capital-intensive infrastructure will take a long time to deliver a return on investment.

Financiers generally require long-term, multi-decade contracts in place first before they’ll underwrite the construction.

So, while Trump is lifting up the natural gas industry with one hand, his tariff policies and unpredictable nature on the global stage are pushing it down with the other.

LNG is a long game that requires a fair degree of certainty that the buyers on the other side will provide robust demand for US natural gas for decades to come. And Trump is introducing a lot more risk into that calculus than industry executives would like.

The world isn’t sitting still on this. China has created a much closer relationship with Russia (the second-largest provider of gas) to the point where one could fairly consider them to be allies. Qatar is expanding its own production, which has the potential to be as much as 70% of the US.

And while we hear so much hype about the demand for natural gas in the US for data centers, the delay for combined cycle turbines (which are extremely specialized machines that only three companies in the world can build, and therefore have a 5-year backlog right now), could similarly push domestic potential buyers of US gas to diversify as well.

Backlash to high energy prices

The final piece of this puzzle that is fascinating to ponder is the sensitivity to energy prices here in the US. There are a lot of articles like this going around right now:

If the natural gas industry is able to pull off its LNG plans, US gas prices would stabilize at something about $4 per MMBTu. That’s about double what prices were at their low point in 2024.

Not only will this raise the cost of gas-powered electricity, but winter heating bills are a big expense, particularly in the northern half of the country.

So how will the public react to their winter heating bill… doubling?

Probably not well. Particularly in this environment.

To me, this is why we see the natural gas industry’s stock and futures prices at their current flat-ish levels. The industry has a timeline problem.

To succeed in the mid-term, it will need its LNG investments to get built and start paying off. For that to happen, it will need to see demand for US LNG continue to be strong in the years ahead. And it will need to successfully weather the potential political backlash such a success could generate at home in response to rising prices.

Maybe AI and its electricity demand will save the day here, too, but it’s notable that we’re not seeing traders make that bet amidst all of the other AI-froth style investments.

So, while it seems like the natural gas industry may have gotten more than the oil industry has from their investment in Trump, it’s far from conclusive that Trump 2.0 will be a net positive for the industry.

Zach Stein is a co-founder of Carbon Collective. ImpactAlpha has partnered with Carbon Collective to provide a monthly analysis on how individuals, companies, and organizations can incorporate the realities of our changing climate and energy systems into their investments. The analysis originally appears in Carbon Collective’s newsletter. All content is solely for informational purposes and should not be used as the basis for investment decisions.