Over the last two years, we’ve seen a growing number of largely white male politicians, business leaders, and even journalists calling for the end of diversity, equity, and inclusion, or DEI, initiatives at public corporations.

This response is not based on empirical data that shows DEI leading to financial underperformance – in fact, the opposite is true. Rather, it seems to be driven by politics and fear.

Ford Motors last week decided to join a small cohort of companies by diminishing its public commitment to DEI. The automaker said it would no longer participate in surveys for the Human Rights Campaign Corporate Equality Index, an assessment used to gauge company policies that support lesbian, gay, bisexual, transgender, and queer employees.

Ford joins Lowe’s, Harley Davidson, Tractor Supply Co., and John Deere in backpedaling on social policies, even as other companies have retained, and reaffirmed, their belief in the bedrock American ideal of the advantages of diverse and inclusive workplaces. It’s been theorized in the media that the rollbacks at these five companies reflect pressure, or the threat of pressure, from right wing extremists.

We have spoken with hundreds of companies about their workplace equity programs and broader sustainability strategies. In private conversations with company leadership, they have expressed their concern that speaking up on DEI-related topics will get them into trouble with a small group of folks who oppose equity. Indeed Ford alluded to this in their announcement, stating “we are mindful that our employees and customers hold a wide range of beliefs.”

Frankly, this is a terrible corporate strategy. It may be easier in the short term — the equivalent of hiding from the classroom bully. In the long term, it harms the company, its employees, consumers, and shareholders. It may also be a fiduciary breach by the corporate board of directors if they reversed DEI policies after making material disclosures to investors that drove investment decisions.

Bait and switch?

Ford’s 2024 Proxy statement reads, “Ford recognizes the value of diversity of skills, experience, and demographic background. Diversity of skills, experience, race and ethnicity, and gender strengthens our competitive advantage and reflects the customers we serve.”

Likewise, Lowe’s 2022 “Building a Culture of Belonging” report states, “At Lowe’s, we strive to be the employer of choice in retail by creating a workplace that brings out the best in our associates…fostering an inclusive and compassionate culture that embraces, respects and values people of all backgrounds and leverages the diversity within the Lowe’s team.”

You’ll find similar declarations in Harley Davidson’s 2024 10-k Report, Tractor Supply’s 2024 proxy statement, and John Deere’s Code of Business Conduct.

Investors who made buy/sell/hold decisions based on these material disclosures may see the sudden policy reversals as troubling in light of the overwhelming analysis confirming greater diversity leads to financial outperformance.

Why adopt DEI programs

Good diversity, equity, and inclusion programs do not hire or promote employees because of their race, gender, or other diversity characteristics. Rather, well-implemented DEI strategies ensure that an employee’s diversity characteristics do not prevent them from reaching career milestones.

These initiatives help companies invest in diverse teams and build inclusive organizational cultures that not only reflect the diversity of customers and the communities in which they operate and serve, but also help drive new ideas, methods, and products that fuel innovation, and, ultimately, growth.

A watershed McKinsey analysis from 2015 underscored all the ways that diversity supports financial profits, and the report holds true today.

It’s impossible not to notice that the results of a well-run DEI program are identical to the goals of a meritocracy. Despite these goals, attacks continue to be levied against DEI, including the McKinsey analysis, from a network of conservative activists in the wake of the US Supreme Court’s June 2023 decision striking down affirmative action in university admissions.

The McKinsey analysis is startling in the clarity of its finding and in its lack of empathy for those who are uncomfortable working alongside people different than themselves: company financial outperformance is benefitted by leadership diversity.

On the surface, arguments against DEI initiatives often lean into a concern that is often cited with data analysis: correlation is not causation. Does it matter if it’s correlation or causation? Diversity and corporate growth are hard to delink, as it is a change that seems to appear concurrently. Larger, more successful companies are more diverse.

The chicken is success; the egg is diversity. Is it possible to know which came first? Maybe.

Follow the data

In 2023, As You Sow and Whistle Stop Capital analyzed over 6,000 EEO-1 reports to assess the management diversity of 1,641 publicly traded companies against their financial performance from 2016-2021. The study, “Capturing the Diversity Benefit,” shows that rather than diversity creating a burden, the more white male leaders a company has, the more likely it is to underperform financially.

To put a finer point on it, linear regression of this massive dataset showed a statistically significant positive correlation between diversity and financial performance.

Even the Wall Street Journal agreed in a September 2023 article “Maybe Hold Off on Getting Rid of the DEI Leader,” which was informed by our report’s data. It pointed out, “Companies that have executives dedicated to diversity, equity and inclusion generally outperform those without anyone in that role…”

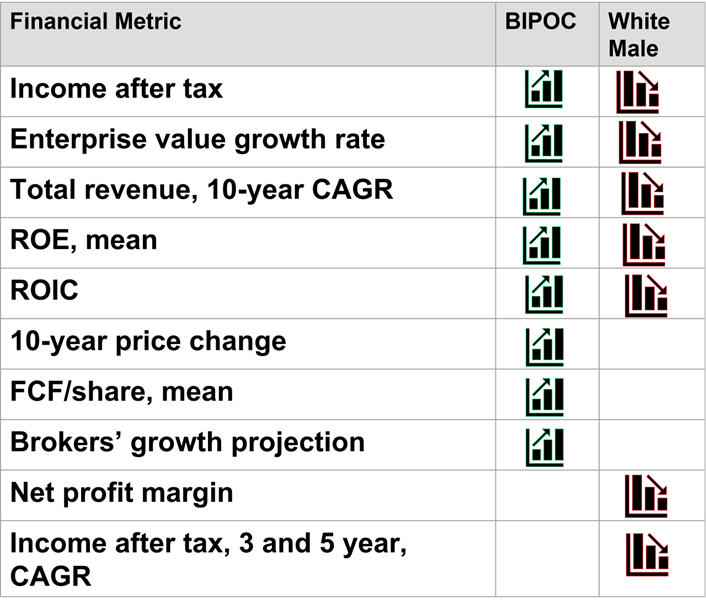

As shown in Figure 1, the more white males a company has, the more likely it is to underperform financially (BIPOC is a shorthand term for Black, Indigenous, people of color. Here it represents all non-White employees).

Statistically significant negative correlations were found between higher percentages of white males and income after tax, enterprise value growth rate, 10-year revenue growth, net profit margin, three- and five-year growth of income after tax, return on equity, and return on invested capital. The numbers are public, the companies are public, and we’re happy to share our methodology and analysis.

Most companies begin with less diverse leadership and diversify over time (a discussion of the skew within venture capital funding is for another time). While the performance harms we see associated with having too many White males is not causation, it is, however, a more damming correlation, as we’re looking at the loss of value; something companies are seeking to prevent.

Engagement

We have been tracking company disclosure of workplace equity data since sending a letter to 3,000 companies signed by investors with nearly $2 trillion in AUM in 2018. While the majority of companies now share workforce diversity data (through the EEO-1 government form), we remain severely constrained in the granular information that a fund manager or investor might review to select the best, most meritocratic companies.

For this reason, As You Sow and Whistle Stop have engaged hundreds of companies to encourage them to release their hiring, retention, and promotion rates (by gender globally, and race and ethnicity within the US).

What better proxy for the strength of a company’s relationship with its employees could there be than a company’s retention rates – not to mention that high retention rates also indicate real cost savings in recruitment, training, and holding institutional knowledge? What better indication for a company’s ability to access the best talent than its hiring rates? And, to understand how well a company can nurture and improve its talent? Promotion rates.

We all want a meritocracy; let’s work together to realize one. We call for the dismantling of systems that allow for historically advantaged groups to continue to underperform.

To do that, we need to understand best practices in detail and call on all companies to release data on their workforce hiring, promotion, and retention rates. Let’s make sure investors have the data they need to allocate capital to those companies that are allowing the best thinkers and hardest workers the success they deserve.

Meredith Benton is the principal and founder of Whistle Stop Capital. Andrew Behar is the CEO of As You Sow.