When do investors change real-world outcomes?

Imagine two investors that publish impact reports both stating that their investments created 10,000 new jobs. In one case, the investor’s capital and engagement with the company was critical to the creation of those jobs, while in the other, the investor’s role was incidental and the jobs would have been created anyway.

Both of these are good outcomes; there is nothing to criticize here. But from an impact perspective, surely we prefer the first!

How can we as investors avoid negative impact and identify and focus our capital and our efforts where they will create the greatest positive change? This is our inspiration for the Investor Contribution 2.0 public consultation that we have launched in partnership with the Predistribution Initiative.

Similar to ImpactAlpha’s recent Metrics Madness tournament, we recently undertook an exercise to collect metrics for investor contribution to intended positive impacts in private capital markets – that is, the contribution that investors make to changes in outcomes for end-stakeholders and the natural environment that would not have likely occurred in investors’ absence1 – and experienced some ‘metrics madness’ of our own.

Over the past nine months, Impact Frontiers and the Predistribution Initiative, supported by Omidyar Network, have been engaged in a consensus-building effort dubbed Investor Contribution 2.0 to develop resources that investors can use to measure and manage their own positive and negative impacts, as distinct from those of portfolio companies.

New approaches for managing investor contribution are emerging out of that madness, and we are now soliciting feedback from practitioners on those approaches through a public consultation period.

It’s a wonky topic, but it matters. For one thing, the question of whether impact investing has an impact depends on it. And regulators are beginning to take notice. For instance, the U.K.’s Financial Conduct Authority’s recent consultation paper on “Sustainability Disclosure Requirements (SDR) and investment labels” proposed that investor contribution should be a requirement for the Sustainability Impact fund label.

In this post we’ll focus on just one aspect of investor contribution: investors’ intended positive impacts on people and the natural environment. A subsequent post from our partners at the Predistribution Initiative will propose approaches for evaluating investor contribution to negative impacts, with a particular focus on investment structures, investment governance, and systematic risks.

Trying – and failing – to standardize metrics of investor contribution to intended positive impact

While impact investors increasingly recognize the importance of investor contribution – it is one of the nine Impact Principles to which more than 170 investors are signatories – little guidance exists to support investors with managing this aspect of impact performance. In the absence of standardized metrics, many impact investors have begun to create their own bespoke metrics for investor contribution.

Last year, we set out to collect as many of these bespoke metrics as we could through an open call; add metrics proposed in industry resources and disclosure frameworks; de-duplicate and organize them; suggest new metrics for relevant impacts and risks that investors are not currently measuring; and then publish a shared set of metrics that investors could use to measure and manage their contributions to positive and negative impact.

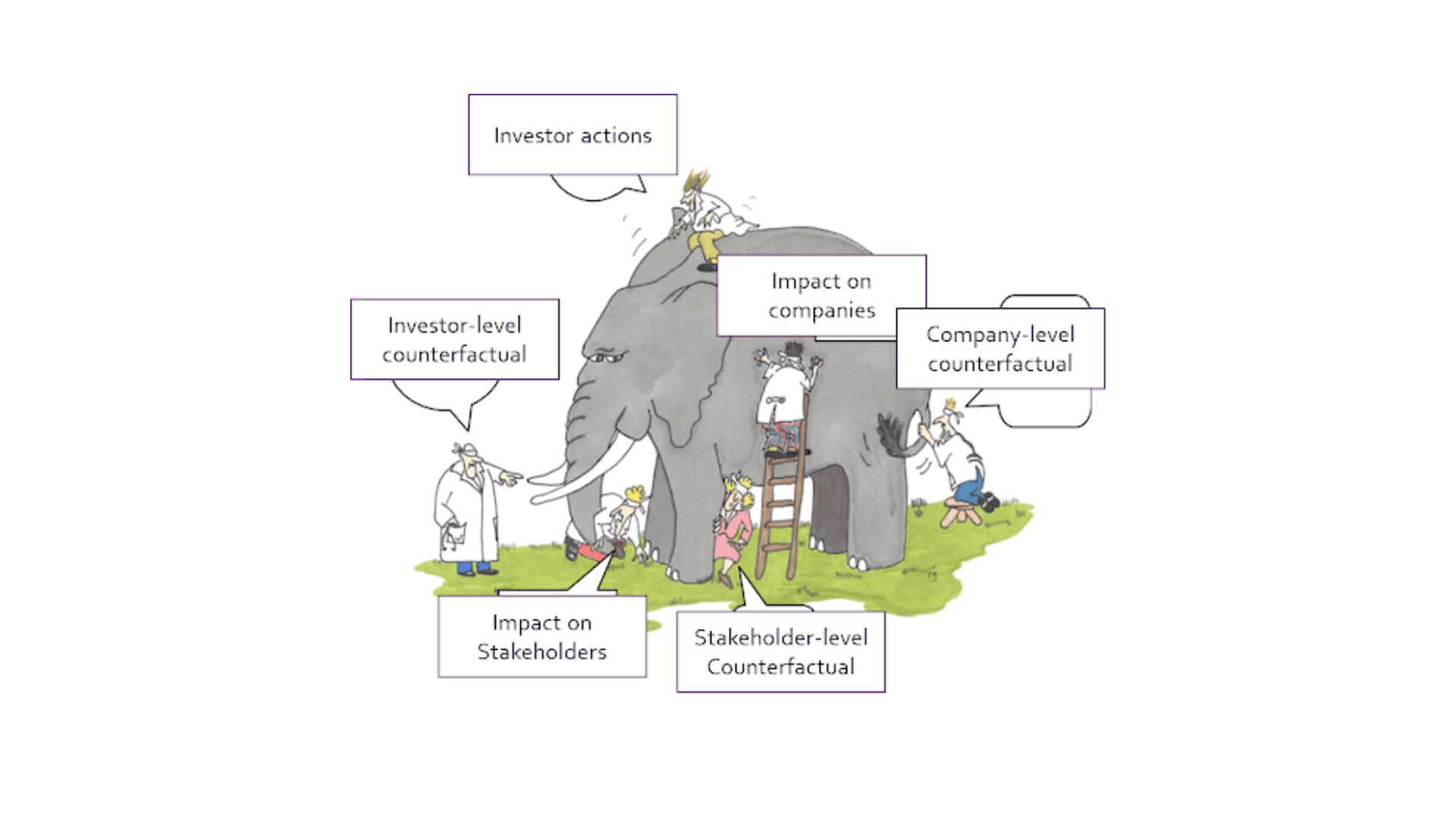

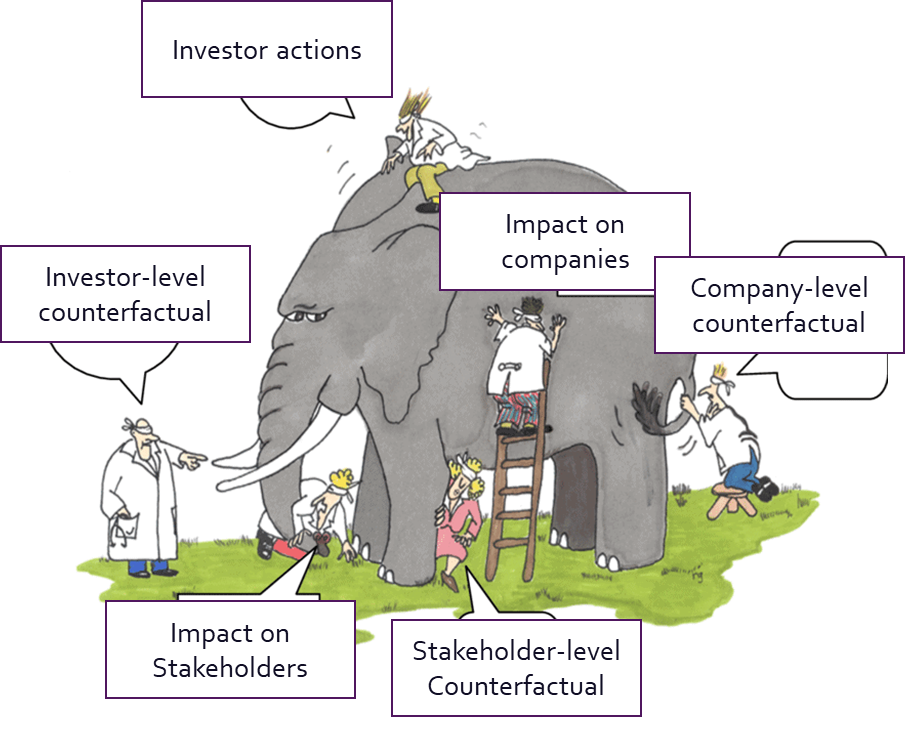

As we began to review the 200+ bespoke metrics we had collected, however, we were reminded of the fable of the blind men each touching a different part of an elephant: each metric seemed to capture a different, incomplete view of the investor’s contribution to impact. (See this short video for a more detailed explanation.)

As we looked more closely, we realized that each of the bespoke metrics spoke to one or more of the following elements of investor contribution:

- Investor actions (e.g., capital allocation, non-financial engagement, investment structure, and governance)

- Investor-level counterfactual (i.e., what would the company likely otherwise have received from investors?)

- Change in company activities (i.e., what did the company do as a result?)

- Company-level counterfactual (i.e., what would the company likely otherwise have done?)

- Change in outcomes for end-stakeholders and the natural environment

- Stakeholder-level counterfactual (i.e., what would stakeholders and/or the natural environment likely otherwise have experienced?)

We’ve published the full list of bespoke metrics that we collected here, if you’d like to review for yourself.

We realized that, when it comes to intended positive impacts, investor contribution does not lend itself to standardized metrics. A ‘metric’ for investor contribution would need to capture not only the change in stakeholder outcomes, but also the causal linkage between the investor’s action(s) and that change in outcomes.

Such causal linkages, between a particular action or set of actions and a particular change in outcomes, are necessarily context-specific and therefore difficult to ‘standardize.’ A particular action or set of actions may not always cause a change in outcomes that wouldn’t have occurred otherwise: the context within which that action takes place often determines whether it is likely to result in a change in outcomes that wouldn’t have occurred otherwise.

In other words, coming up with a list of commonly observed investor actions is easy. Yet to equate an investor action that wouldn’t have been taken otherwise with investor contribution – absent its effects on companies and ultimately on end-stakeholders – is a contradiction in terms. The entire point of investor contribution is the impact on people and the planet!

This series of reflections led us to gravitate away from creating a standardized set of investor contribution metrics, and towards the idea of a plausible narrative for investor contribution that considers counterfactuals. Considering counterfactuals means considering context.

What if, rather than standardizing metrics for investor contribution to positive impacts, we instead standardized the expectation that investors consider each of the six elements of the ‘investor contribution elephant’ in a structured, evidence-informed way?

To be sure, investors won’t always have robust information about all six elements of investor contribution listed above. Many investors have only partial visibility into company impacts, and even less into counterfactuals (i.e., what would have happened otherwise). But these six elements can still provide a shared structure by which we communicate what we do know and don’t know about our investor contribution – and most importantly, help us to improve that investor contribution.

We’ve mocked up a simple template to provide investors with a structured way to think through and gather evidence for their own investor contribution, along with a brief explanatory video. We invite ImpactAlpha readers to try it out and let us know what you think at [email protected]. We’ll incorporate your feedback and provide a revised version of the template this summer.

Confronting Counterfactuals with Plausible Narratives

The template prompts investors to consider counterfactuals, or the difference between what happened with the investor’s investment and what would have happened otherwise, without the investor’s investment.

Counterfactuals are the tusks of the elephant upon which efforts such as this one tend to impale themselves.

To put it bluntly, investors will rarely if ever be able to prove what would have happened in their absence. To expect otherwise is folly.

What we are proposing is that counterfactuals are still worth thinking about – even if you know you’ll never have proof. Proof is not the point. The point is to inform decision-making. For that we can use evidence that falls short of proof.

In lieu of either standardized metrics or rigorous proof of counterfactuals, we are exploring the concept of a ‘plausible narrative’ for investor contribution: a structured, thoughtful account of the six elements of the ‘elephant,’ informed by evidence to the extent possible.

A plausible narrative of investor contribution provides good reason to believe that the investor’s action caused a specific change in outcomes for end-stakeholders or the natural environment that wouldn’t have likely occurred in their absence.

Plausible narratives of investor contribution can be qualitative or quantitative, short or long. They are essentially a theory of change, customized for a specific use by investors. Like any theory of change, they can express ex-ante goals, or ex-post results. And like any theory of change they can differ in quality.

The GIIN has similarly pointed to theories of change for investor contribution in its recent Guidance for Pursuing Impact in Listed Equities, noting that ‘further work is needed to develop methodologies for how to consistently assess the presence and quality of investor contribution.’ We are proposing a structure for what this might like look like, albeit in the context of private capital markets rather than listed equities.

Paddy Carter, British International Investment’s Director of Impact, suggested to us a standard of evidence akin to that of civil law, which requires a ‘preponderance of evidence’ that leads one to believe that the claim of investor contribution is ‘more likely true than not.’ (By contrast, the standard of evidence in criminal law requires ‘proof beyond a reasonable doubt’ – an unnecessarily and possibly unreachably high bar.)

By prompting investors to thoughtfully consider the likelihood that their action(s) did or are expected to cause changes in outcomes that wouldn’t have likely occurred in their absence, this approach improves upon bespoke metrics that present an incomplete view of the whole ‘elephant.’ At the same time, it doesn’t require extensive or impractical data collection and analysis. Our proposal is that investors assess whether there is a sufficiently compelling case that their action(s) have caused or are expected to cause a change in outcomes that wouldn’t have likely occurred in their absence. In other words, a sufficiently ‘plausible narrative.’

Investors may not have a plausible narrative of investor contribution for many of their investments – and that’s to be expected. Many responsible or sustainable investors do not aspire to directly cause positive impacts that wouldn’t otherwise have occurred.

Even for investors that do, some investments offer greater opportunity for investor contribution than others. Investors can and do employ a ‘portfolio approach’ in which a subset of the portfolio’s investments represent most of the investor contribution.

Next Steps

For this idea to work, we as a sector would need to build consensus on what constitutes a ‘plausible narrative’ for investor contribution that neither opens the door to ‘impact-washing’ nor sets the bar impossibly high.

As a starting point, we’d suggest that narratives of investor contribution are ‘plausible’ to the extent that they:

- Speak to as many of the six elements as possible; and

- Provide contextual evidence – from investees, from market research, from stakeholder feedback, and from other relevant sources of information – that give good reason to believe that the observed outcome for end-stakeholders and the natural environment likely wouldn’t have occurred otherwise.

In practice, it will fall to the relevant decision-maker to judge the plausibility of investor contribution. Evaluating asset managers’ claims of investor contribution can be a constructive and proactive role for asset owners and allocators to play in impact management. Consensus that emerges from our public consultation can help them do so, as can third-party verification and assurance.

These ideas are intended as an invitation to thoughtful debate, in hopes of identifying points of consensus by mid-year 2023. We’ll keep the window for discussions open through the end of April, and then circle back in the summer or fall with a synthesis of where we’ve got to.

Additionally, this post is the first in a series of two that share developments on the Investor Contribution 2.0 project. A future post by our partners at the Predistribution Initiative will share developments on draft disclosures that can support Limited Partners in measuring and managing the investor contributions of their General Partners, with a particular focus on investment structures, investment governance, and systematic risks.

We hope you’ll join the discussion. The materials we’ve developed to support that approach are now open for public-consultation via our project website.

Footnotes

- Impact attribution is not part of our project (i.e., estimating what % of an outcome an investor caused, for instance by pro-rating their share of the total capital provided to the enterprise).