Centuries of policies that privileged white economic mobility while excluding or actively exploiting communities of color have created a racial wealth chasm in the US. Today, the average white household in the US holds six times the wealth of a Black household, five times the wealth of a Latino household, and more than 10 times the wealth of a Native American household. The persistent divide, compounded over time, threatens to lock generations of people of color into a permanent underclass.

But it doesn’t have to stay that way.

For every driver of the racial wealth gap, there are ways for patient capital to unlock lost potential.

“Capital has done a significant amount of harm to communities of color,” says Santhosh Ramdoss of Gary Community Ventures. “To undo that, we need the same capital to become a restorative tool.”

It would take more than $8 trillion to close the wealth gap between the median white household and the median household of color. That number may seem astronomical but consider this: the combined wealth of the top 1% of households climbed a staggering $11 trillion since 2020.

The racial wealth gap not only locks communities of color out of full participation in the “American Dream,” but also stunts the economy as a whole. Both consumption and investment grow with increased wealth—McKinsey & Company estimates that closing just the Black-white gap would add $1 trillion to $1.5 trillion in annual GDP growth by 2028.

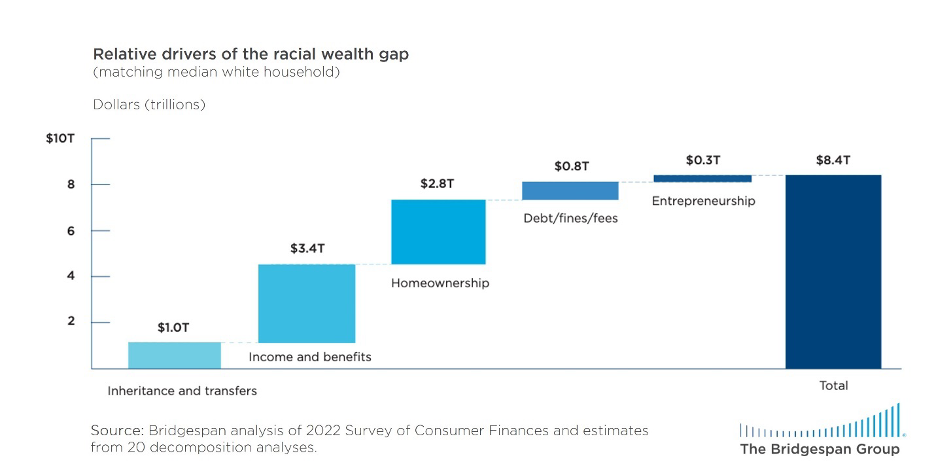

Bridgespan recently published research that found five main drivers of the $8.4 trillion racial wealth gap:

- Family inheritance and financial support provided to households via intergenerational transfers and contributions in the form of gifts during one’s lifetime. Young white households (ages 24-35) with limited time to build assets on their own already have a 2:1 advantage over Latino households and a whopping 40:1 advantage over young Black households in terms of net worth.

- Income and benefits received from participation in the labor market, including retirement plan contributions and health insurance. People of color, women, and particularly women of color, dominate the lowest-paying occupations with disproportionate overrepresentation in lower-wage jobs with fewer benefits and fewer worker protections.

- Homeownership and the relative return from investing in real estate assets. Homeownership rates for Black (44%), Latino (51%), and Native American (53%) communities are lower than the rate for white families (72%).

- Avoiding excessive debts, fines, and fees (for example, consumer debt, banking fees, interest rates) that become an encumbrance on income and assets. Rooted in a history of predatory practices, profit-seeking entities have historically built wealth for white individuals and institutions at the expense of households of color, reflected in median debt-to-asset ratios nearly twice as high for Black and Latino families compared to white families.

- Entrepreneurship and small business ownership that provides both income and commercial assets via business equity. Disparities in business ownership show Black business owners at 2.7% of employer businesses, Hispanic owners at 6.9%, American Indian and Alaska Native owners at 0.8%, and Asian owners at 10.9%.

A role for impact investors

We believe philanthropists and impact investors have an important role to play here to benefit communities and the economy as a whole. They should regularly use the full spectrum of investment returns—from market-rate to impact-first to grant funding—to scale up wealth-generating opportunities that disproportionately benefit those at the bottom of the economic pyramid.

Let’s consider each of these five drivers of the racial wealth gap one-by-one alongside corresponding investment, as opposed to philanthropic, solutions. (Full disclosure: some of the organizations featured here have been clients of Bridgespan.) These opportunities first and foremost aim to build the wealth of communities of color, not extract wealth from them. So, while they are all attractive to returns-focused investors, they are not the best fit for investors out to make a quick buck.

Family inheritance and financial support

We don’t believe this driver is easily investable in a returns-seeking way. It appears to us that this driver is best addressed through government policies, programs, and philanthropy. For example, recent Bridgespan research explores the potential of “baby bonds”—a trust account that beneficiaries born into poverty can use for wealth-building activities when they reach adulthood. This approach is being piloted at scale in Connecticut with at least half a dozen states exploring similar initiatives.

Income and benefits

Employee Stock Ownership Programs, or ESOPs, are one promising, investable way to help raise the income and benefits of people of color. One form of ESOP uses investor capital—often in the form of a loan—to buy out departing owners and create shares allocated to individual employees. When employee-owners of the ESOP subsequently leave or retire, the company buys back the employee’s stock at fair market value—which can be up to multiples of an annual salary.

Research shows that this type of ESOP leads to higher wages, greater job stability, and significant wealth generation for workers. If 30% of all businesses were owned by employees through an ESOP, median wealth among Black households would more than quadruple, from $24,000 to $106,000.

Mosaic Capital Partners, for example, is a private equity firm managing $371 million in assets that seeks to increase employee ownership by acquiring lower and middle market companies through ESOP buyout. The firm finances the purchase of the company through an ESOP Trust, and structures the deal to hand over all equity to employees in three to five years. With its inaugural fund, Mosaic has created over 3,000 employee owners.

Ownership economy

Homeownership is the most broadly accessed path to wealth generation in the United States. More households own their homes than hold retirement accounts—with primary residences representing 42% of the median homeowner’s net worth. The legacy of exclusionary federal policies is clear in the homeownership rates for communities of color.

The Blackstar Stability Distressed Debt Fund, for example, has raised $100 million to purchase thousands of single-family homes tied to “contract for deed sales,” an often predatory lending practice where the seller sells directly to the buyer through an installment payment plan, but the buyer only holds the deed upon completion of installments. Blackstar Stability refinances these homes with traditional mortgages that offer better interest rates, lower monthly mortgage payments, and the potential to build home equity. So far, Blackstar has purchased about 200 homes.

Or consider the Dearfield Fund for Black Wealth, which aims to help Black first-time homebuyers build generational wealth. The fund provides up to $40,000 in down-payment assistance and helps borrowers through a homeownership support program. The loan is repaid upon sale of the home in a balloon payment of the principal plus 5% of the home’s appreciation. Dearfield has worked with over 150 families to purchase their first home.

To be sure, while there is wide agreement that differential rates of access to homeownership historically drove the racial wealth gap, experts debate whether more equitable rates of homeownership are the solution going forward. Some argue that the challenges of homeownership make it a less compelling avenue for wealth creation: the illiquidity of the housing asset, the magnitude of debt required to purchase a home, and the “eggs in one basket” risk that could burst with a housing crash. Other experts are still convinced that homeownership remains a key driver of wealth generation for communities of color.

Avoiding excessive debts, fines, and fees

One way that investors can engage in this driver is through community development financial institutions, or CDFIs. These are lenders with a mission to provide fair, inclusive financing to historically disinvested communities. To address the financing needs of small businesses that may struggle to secure traditional loans, they offer patient and flexible capital.

Camino Financial, for example, is a CDFI and online lending platform that offers business loans that specifically target under-banked Latino microbusinesses in need of affordable credit. The firm seeks to promote financial inclusion and support overlooked entrepreneurs. It currently manages at least $250 million in assets and has deployed $30 million in loans.

Entrepreneurship and small business ownership

One straightforward way to address this driver is to invest directly in leaders of color. Entrepreneurs and business owners of color face historic structural barriers and patterns of bias when seeking capital to get started—from both financial institutions and investors. In our research of over 200 investees of impact funds, we found that those led by people of color were twice as likely to take an explicit lens toward racial equity.

Collab Capital, for example, is an early-stage venture fund that provides social and financial resources to businesses with at least one Black founder with a controlling stake. The firm invests across a range of industries and looks to focus on investees in Atlanta and other cities with high levels of Black entrepreneurship. It uses versatile profit-sharing agreements that allow founders to retain more equity as they grow their enterprises. Its versatile agreement structures do not demand as stringent returns as typical VC funds. In the two years since closing Fund 1, Collab Capital has already invested in 35 companies.

Similarly, Harlem Capital is a venture fund with a mission to invest in 1,000 underrepresented entrepreneurs over a 20-year period. It makes initial investments of $1 million to $2.5 million in seed rounds for 10% to 15% ownership in companies that have proven their value propositions in markets of at least $1 billion. Founders also benefit from the fund portfolio’s overall performance by splitting 1% of the fund’s carry with them, sharing the benefit of other founders’ success. To date, Harlem Capital has invested in 53 companies across 10 cities in a range of industries.

The private sector has historically disinvested in, excluded, or exploited communities of color. We see a range of investable opportunities to right those wrongs and generate returns without further exploiting communities. Strategies for narrowing the racial wealth gap are abundant. Impact investors seeking to engage will find real returns-seeking opportunities awaiting their diligence.

Stephanie Kater is a partner at The Bridgespan Group based in Boston. Devin Murphy is a partner in Bridgespan’s New York office. The authors also thank Rebeca Cavalcanti, a manager in the Chicago office of Bain & Company, and Zach Slobig, an editorial director at Bridgespan.