Impact investors must wrestle with an uncomfortable truth: social and ecological crises have deepened and become more entrenched in the years that impact investing and sustainable finance have grown in prominence.

Our idea was radical when the term “impact investing” was coined 20 or so years ago, but the tools we have developed as a field have largely failed to scale or radically change traditional financial market architecture. Ours instead have mostly tried to fit in. We have muted our missions and our impact as a result.

We’re not here to maintain the status quo.

We’re here to reimagine capital – to make it accountable, inclusive and regenerative. It’s time for impact investing to get a refresh. Let’s call it Impact Investing 3.0.

In this new phase, new formulas for fund design will play a central role in shaping the economic possibilities for enterprises and founders and their pursuit of deeply impactful business models. Impact investors will need to embrace active fund design, from the ground up, to fit the purpose of what they are trying to achieve.

If that sounds like starting over, it isn’t. In the early days of impact investing, we proved to the markets that impact and financial returns can go hand in hand. In our 2.0 era, we created and adopted more standardized ways to measure and manage impact; we delved into thorny issues like the extractive nature of impact investing, ownership models and inclusion; and we built, tested and replicated a raft of new financing models. We have accumulated nearly two decades of field-building muscle to launch us into a new phase.

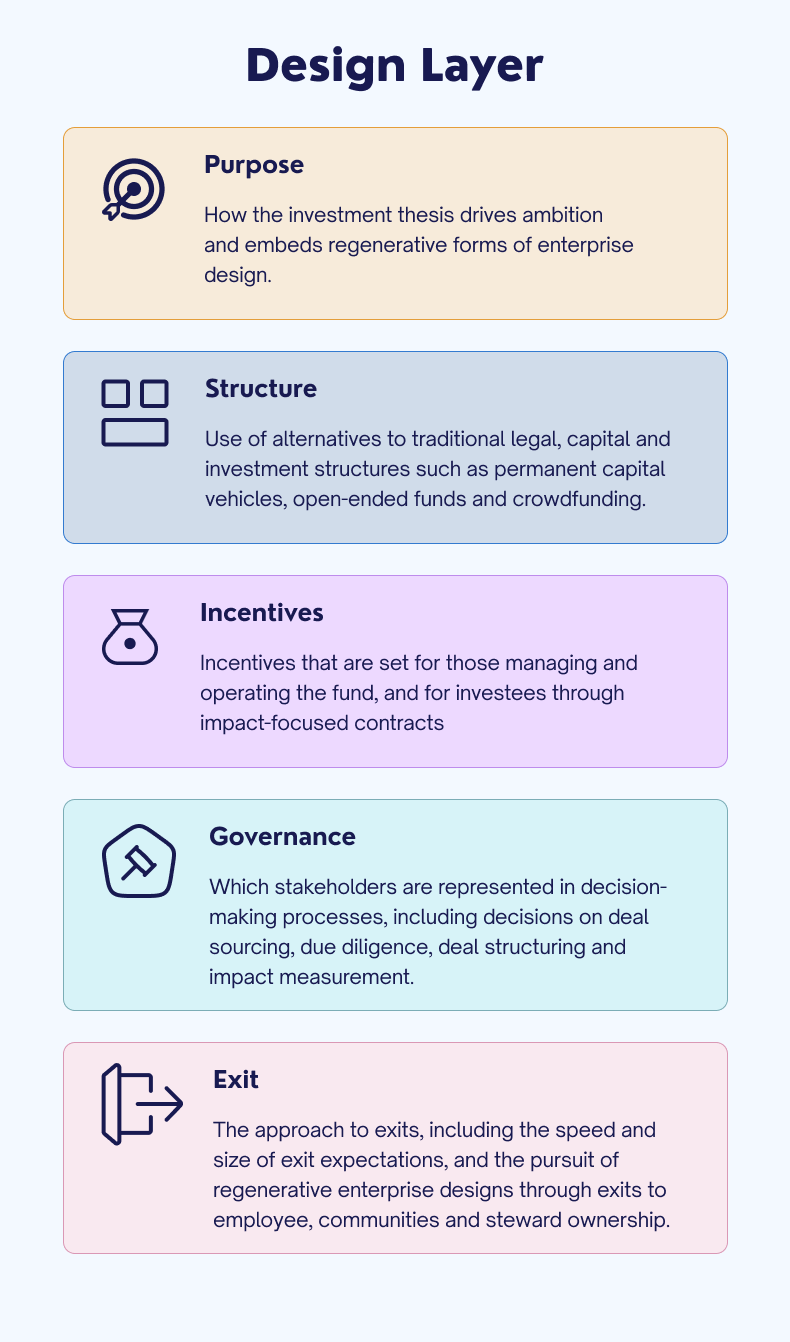

In this piece, we propose a framework to help fund managers get started in Impact Investing 3.0 by actively designing their funds to unlock greater impact. We detail five component pieces – purpose, structure, incentives, governance and approach to exits – and provide questions to consider and models to explore.

Our approach melds together the concepts from “Adventure Finance” and “Doughnut Economics,” as well as frameworks developed by the author and theorist Marjorie Kelly.

Note: we use the term “fund” to broadly capture any type of capital allocation vehicle.

Why fund design matters

How a fund is designed determines which enterprises receive funding and what kind. Components of design include the purpose (investment thesis); how the capital aggregation and allocation are structured; how those managing the fund are compensated (incentives); and whose voice is part of investment decisions (governance).

Fund design can also influence the relationship between a fund manager and its investees. The type of capital, returns expected, and/or timeline for repayment can affect how ambitious an entrepreneur can be with their business model, product design, production model, approach to suppliers, relationship with employees and more.

Take, for example, a fund focused on renewable energy access. Incentives, like a fund’s carried interest structure, could help or hinder the work of a startup building critical on-the-ground energy infrastructure in rural areas. That startup may be building distribution, installation, maintenance, education and financing infrastructure from scratch. The exit and return expectations of capital it receives would likely factor into key strategic business decisions, like partnerships with other organizations to scale, or how tightly it holds onto its insights and intellectual property.

Fund purpose

The purpose of a fund is reflected in its investment thesis. For a fund to achieve its purpose, the design must reinforce the thesis and aim to invest in a way that helps businesses become regenerative.

Consider The Purpose Fund, Unlike traditional models that prioritize shareholder value and short-term profits, The Purpose Fund champions “steward ownership,” which legally enshrines prioritization of companies’ long-term purpose and ensures that decision-making power is held by stewards directly connected to its operation and mission. By investing in companies committed to this ownership structure, The Purpose Fund actively promotes a business approach where purpose and mission take precedence over profit maximization.

An important question for consideration in developing a fund’s purpose: Does your investment thesis take a transformational approach, attempting to foster impact enterprises that themselves embed a regenerative enterprise design?

Fund structure

How a fund is structured and how it deploys capital determines its relationships with both investors and investees. Traditional legal, capital and investment structures, like venture capital, or private equity or debt funds, may restrict a manager’s ability to have deep impact.

Alternative options: permanent capital vehicles, open-ended funds, holding companies, nonprofit vehicles, crowdfunding, rolling funds, and innovative syndication models.

By embracing a broader continuum of capital and diverse array of financial products, fund managers can free themselves from the narrow, one-size-fits-all approaches.

Consider Fair Capital Partners, which uses a permanent capital, or evergreen, model. This structure allows a longer-term investment horizon helps foster deeper and more sustainable impact. Fair Capital Partners’ decision to start from scratch on fund design allowed it to tailor its architecture to best serve its impact objectives.

Questions to consider in designing fund structure:

- Does the legal structure of your fund allow you the time, space and agency to generate deep and transformational impact?

- Have you built a capital structure that gives you the license to focus on the most significant issues, and enable the strategies, practices and business models that can drive transformational impact?

Fund incentives

Incentives cover both compensation structures for those managing and operating the fund, as well as the contractual obligations with investees.

Salaries, bonuses and other rewards shape the decisions and priorities of fund managers. Often managers of traditional funds are incentivized only based on financial returns rather than by their funds’ impact.

Similarly, contracts with investees are often skewed toward financial performance. Designing contracts to include social and/or environmental incentives is critical to enabling deeper impact.

Prime Coalition, for instance, has embedded impact-linked compensation into its fund structure. Its investment managers’ compensation is directly tied to the achievement specified climate impact goals, such as emission reductions. By incentivizing impact outcomes alongside — or even over — financial returns, Prime Coalition ensures its team’s motivations are aligned with its overarching mission of tackling climate change.

Questions to consider in designing the incentives for staff and investees:

- Are your team members incentivized to create positive social and/or environmental impact through their carry, bonuses or performance evaluations?

- Are your investees contractually incentivized (or obligated) to create positive social and/or environmental impact?

Fund governance

The governance structure of any fund or business determines how decisions are made. This covers how the fund conducts sourcing, due diligence, contracting and deal structuring, portfolio management, and impact measurement and management.

Funds can be designed to determine who is represented on the board, how trade-offs are navigated, transparency of decision-making and impacts, and how the approach and strategy evolves over time.

A central point to address in governance is to identify those who are impacted and who otherwise have the least power and voice, and how to extend power and voice in decisionmaking and priority-setting.

Citizenfund in Belgium invests in local impact enterprises that struggle to secure capital. The fund is run as a cooperative; investors, or “cooperators,” select the projects the fund backs through inclusive discussions supported by subject matter experts. Anyone can become a cooperator by investing as little as €5, and every cooperator gets to vote on pitched projects. Cooperators also collectively decide how to tailor return expectations and exit approaches for each investment.

Citizenfund is using a franchising model to spread to other locations while using a centralized platform.

Questions to consider in designing the governance of the fund:

- How can those most impacted have a voice in your investment committee and/or board?

- How do you ensure the way you source deals is inclusive (and not biased from a racial, gender, religious, sexual orientation or geographic perspective)?

- Whose interests are prioritized when you do due diligence? Have you designed the process to empower those closest to the issue you are trying to solve?

- Who do you decide on the impact data that matters, and who has a voice in this?

Fund exits

How fund managers pursue exits shapes strategies their investees pursue, and can influence how a business pursues impact long-term, after the exit. The speed and size of a desired exit can affect how aggressively a portfolio company chases short-term profits, how much debt it takes on, its selection of subsequent investors and owners, and whether they remain committed to impact.

Exit strategies that are more conducive to long term impact than traditional equity deals include employee- or community-ownership transactions and self-liquidating instruments.

Apis & Heritage, for example, operates as a mezzanine debt fund manager that acquires companies from retiring owners, particularly those with significant workforces of color, and transitions them to 100% employee-owned businesses. A&H’s capital facilitates the sale of a business directly to its employees, providing retiring owners with a path to liquidity at a fair market price and, crucially, helping low- and middle-income workers build wealth through business ownership.

Questions to consider in designing the approach to exits:

- Does the exit strategy of the fund reinforce the impact thesis?

- Are the return expectations and the expected timing of the exit fit for purpose for the underlying investee?

- How will those most impacted have a voice in the enterprise after your exit?

- How will your exits facilitate enterprise designs that are focused on transformational impact?

Embracing Impact Investing 3.0

We are at an inflection point in impact investing. We have the opportunity to build funds that redefine what it means to allocate capital to impact. This is only possible if asset owners and fund managers work together. We need infrastructure, support, education and a collective willingness to do things differently.

The Doughnut Economics Action Lab now has a community of more than 100 networks, consultancies and business schools working on enterprise design innovation and to support founders and business leaders in adopting these emerging designs. What’s needed now is more fund managers that with investment vehicles designed to match these businesses’ impact ambitions. The community of change-makers is calling on investors to engage with this agenda.

The newly launched Innovative Finance Network is working to map, connect and convene those embracing Impact Investing 3.0. It has support from over 200 asset owners, including family offices and foundations, technical experts like impact management, tax, legal and structuring experts, fund managers and ecosystem builders.

Connect with us so we can learn, engage and build better, deeper and more transformative impact finance, together.

Aunnie Patton Power is a co-founder of Innovative Finance Initiative, five-year effort to scale what works and unlock what’s next in the world of innovative finance. She is an advisor, author and academic on impact investing.

Erinch Sahan is the business and enterprise lead at Doughnut Economics Action Lab and teaches sustainability at University of Cambridge.