Energy pricing volatility. Extreme weather events. Commodity scarcity and disruption. Infrastructure deterioration. Employee dissatisfaction and turnover. Consumer demand for healthy, natural products. These trends, and others associated with material sustainability issues, must be part of well-managed corporate strategy and investment in today’s world.

Many corporates and investors recognize this and embrace ESG reporting and compliance. However, ESG reporting and compliance does not, by itself, drive better financial and societal performance. And most companies are not tracking the financial return on their sustainability investment.

That leaves investors without the data they need to determine if a portfolio company’s sustainability strategy is driving resiliency and better financial performance.

For example, investors may think circularity is primarily about waste reduction and a net cost, and thus underinvest. They will generally ask companies for the net waste removed from landfill, for example, but not what the financial returns were.

However, circularity is a financial superpower: it reduces input costs and reliance on globalized supply chains, cuts waste management costs, and can sometimes allow the company to make money twice on the same product. It reduces exposure to tariffs in the US (e.g. an automotive company refurbishing used parts in the US pays no tariff on those components) and can lower the price of end products, reaching new customers. If a manufacturing company begins to track that kind of data, it and its investors will make better decisions for the bottomline as well as for society.

The NYU Stern Center for Sustainable Business, or CSB, has researched the Return on Sustainability Investment, or ROSI, for a decade, working across industries and asset classes. We have consistently found that sustainability can drive significant value across the value chain. Through hundreds of interviews and engagements, we have also found that GPs are not tracking ROSI and LPs are not asking them for that information.

A framework for sustainability value creation

In response, and working together with an advisory group of Limited Partners as well as guidance from Institutional Limited Partners Association, or ILPA, CSB has introduced a set of five value creation/presentation questions that asset owners can use to explore how well asset managers and corporate executives (especially in private markets) are tracking and investing in sustainability-linked value creation.

Pension and endowment fund managers tested the beta version with their General Partners and their feedback was incorporated into the final set of questions and guidance that was recently released and is available as an open source tool for asset owners. The asset owners used the tool in different ways: most incorporated it into their engagement conversations, some added one or more of the questions into their due diligence questionnaire. All found it a useful addition to their non-financial ESG reporting questions.

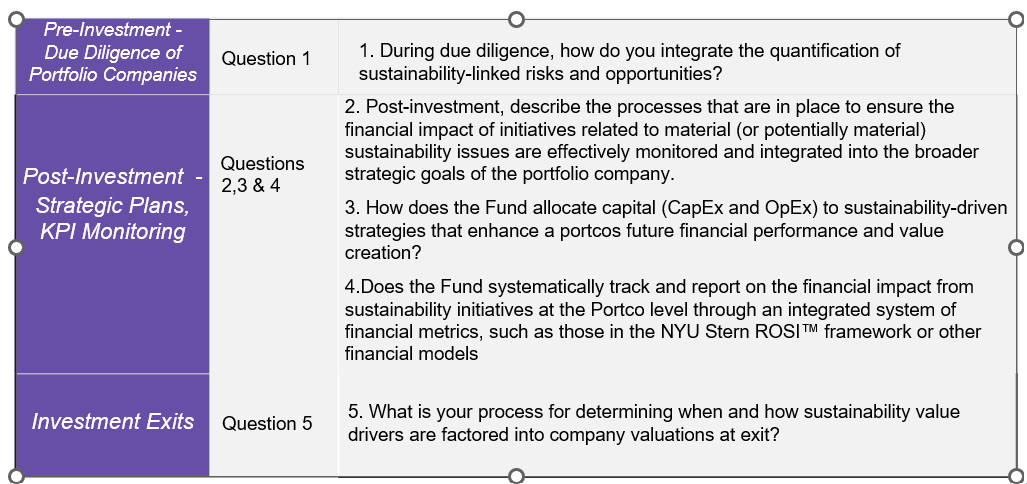

The tool assesses asset manager capabilities in sustainability-linked value creation throughout the full investment life-cycle as seen in Figure 1:

Figure 1: Sustainability-Linked Value Creation Across the Investment Cycle

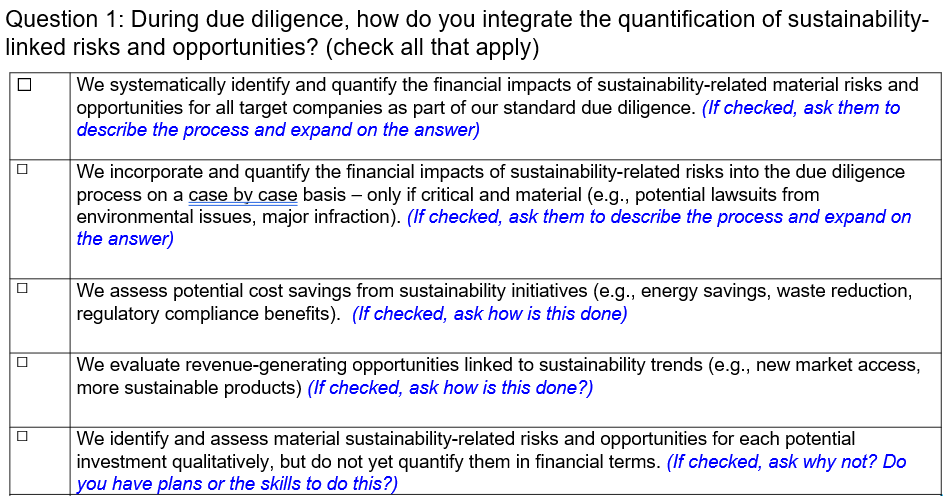

The five questions that investigate sustainability-linked value creation and preservation are in Figure 2. The guidance also provides a set of additional information points to assess actual performance that go beyond these high-level questions:

Figure 2: NYU Stern CSB Sustainability-Linked Value Creation Questions for LPs to ask of GPs

Each question has additional detail for respondents to fill out or for asset managers to ask during a conversation with the GP:

Figure 3: Value Creation Question 1 with Additional Guidance

In piloting the model with their GPs, asset owners found similar results on GP quantification of sustainability returns in keeping with CSB’s research and engagement with private equity firms.

- GPs are not isolating sustainability returns from broader corporate strategy

- They lack internal controls and infrastructure to quantify sustainability-linked financial outcomes

- The “S” and “G” are particularly difficult to quantify

- GPs may be reluctant to share financial KPIs linked to sustainability KPIs due to uncertainty and concerns about accountability

- GPs report a lack of interest by investors generally in quantifying sustainability-linked value

Using the CSB sustainability-linked value creation questions either as part of a due diligence survey or during engagement conversations may help the asset managers develop expertise and additional decision-making data.

Other resources

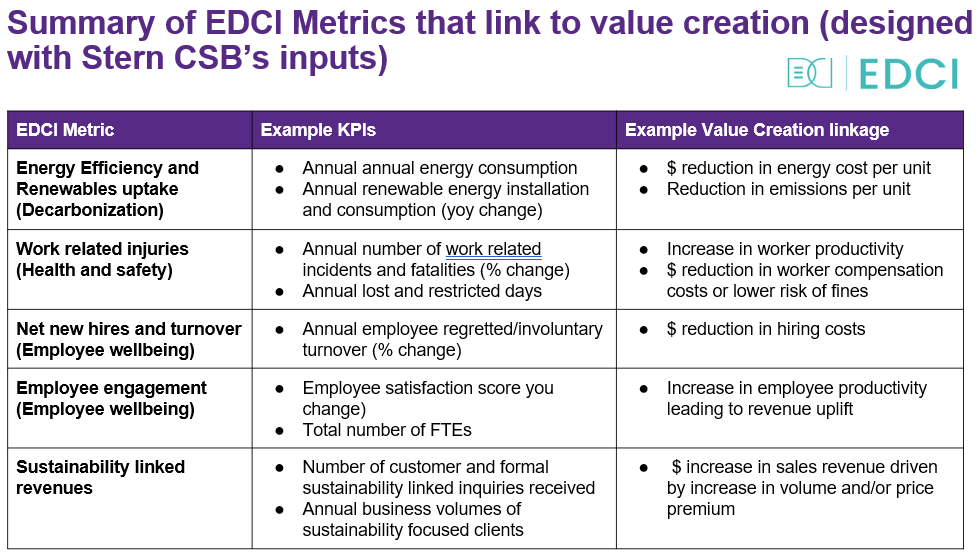

Asset managers have another tool at their disposal, as well. The ESG Data Convergence Project, or EDCI, with CSB’s help has introduced financial KPIs to accompany the EDCI sustainability KPIs. Those KPIs and monetization methods are now being tested by EDCI members. Asset owners can begin to ask GPs to collect the information below as a place to start.

Other useful resources for asset owners and asset managers alike include CSB’s research on the Return on Sustainability Investment (ROSI™), a methodology and set of tools that companies actively embed sustainability factors core to business strategy to drive improved financial performance.

The newly released UNPRI GP sustainability-linked value creation guide, for which CSB was the academic partner, may also be useful. CSB has developed a complimentary tool for GPs and their portcos in collaboration with a group of GPs. The GP tool is designed to help identify financially material ESG issues and manage financial outcomes through a database of sustainability and ROSI KPIs (visit the CSB Responsible Private Equity webpage for additional information on this effort).

In summary, tackling material sustainability issues as part of business strategy is just good management. It drives operational efficiencies, innovation and growth, risk mitigation, employee retention and productivity, marketing and sales, in addition to societal benefits. Investors interested in improving the bottomline and societal benefits (and most impact investors are interested in both) now have the tools they need to hold their asset managers accountable for delivering profit and purpose.

Tensie Whelan is Distinguished Professor Emerita, NYU Stern, and Senior Advisor, NYU Stern Center for Sustainable Business