Achieving net-zero emissions requires transitioning from a fossil-fueled economy to one energized through metals and materials. Nearly $2 trillion in investment in mining and production of key metals will be needed in a scenario that keeps warming below 2 degrees Celsius.

We are in a new commodity “supercycle” focused on “green” materials such as copper, lithium, nickel, and cobalt that are central to the low-carbon transition. A single wind turbine requires 4.7 tons of copper, according to the World Bank, while EV batteries use copious amounts of lithium, nickel and cobalt.

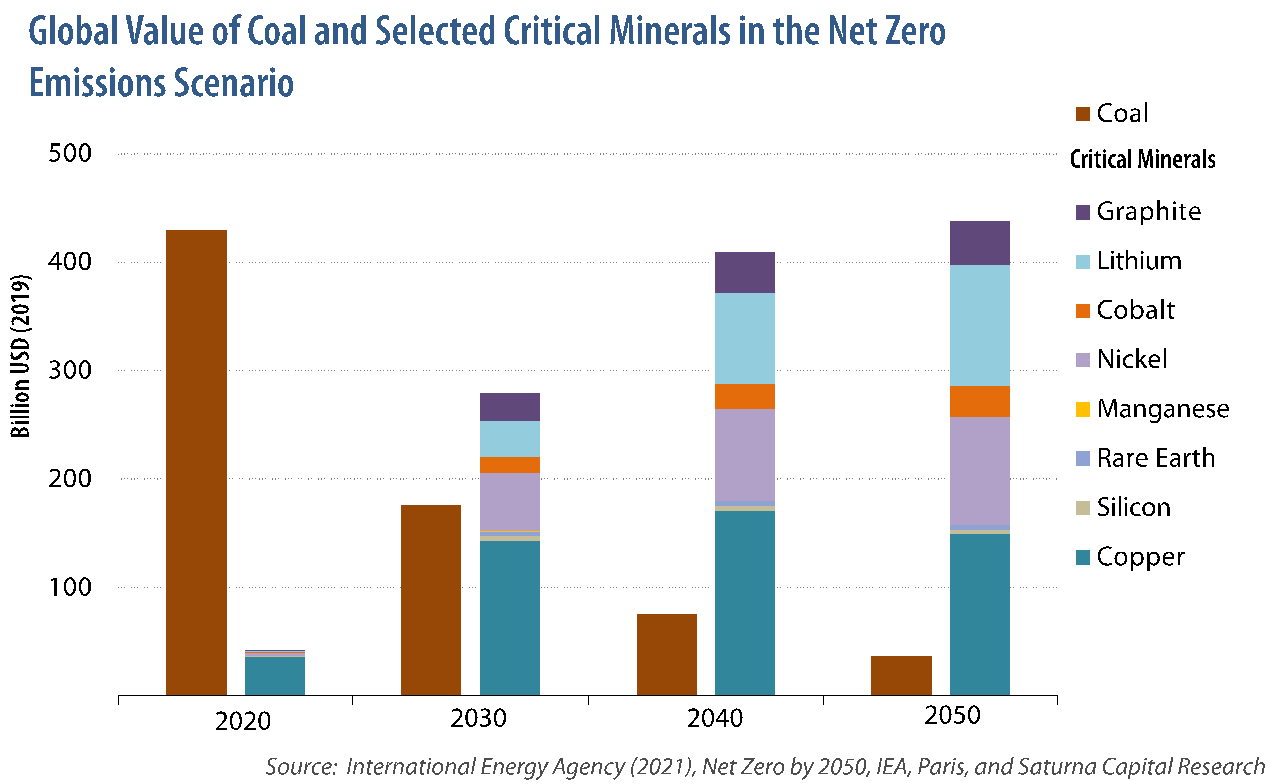

As the world transitions to a low-carbon economy, demand for these clean tech metals will need to increase seven-fold by 2030, with revenues from these materials expected to exceed those of coal. That has set off a global scramble to secure supplies.

The transition will be marked by long mine development lead times, high capital intensity, and price volatility. These factors are likely to create bottlenecks in the shift to a low-carbon economy.

Looming over it all is concerns about regional impact. Mining is rife with case studies of safety issues, environmental degradation, and human rights violations. Regardless, the industry is booming and set to escalate at a fast and furious pace, underscoring the importance of environmental, social and governance due diligence and holding companies accountable for their operations and contributions to positive change.

Supply Side

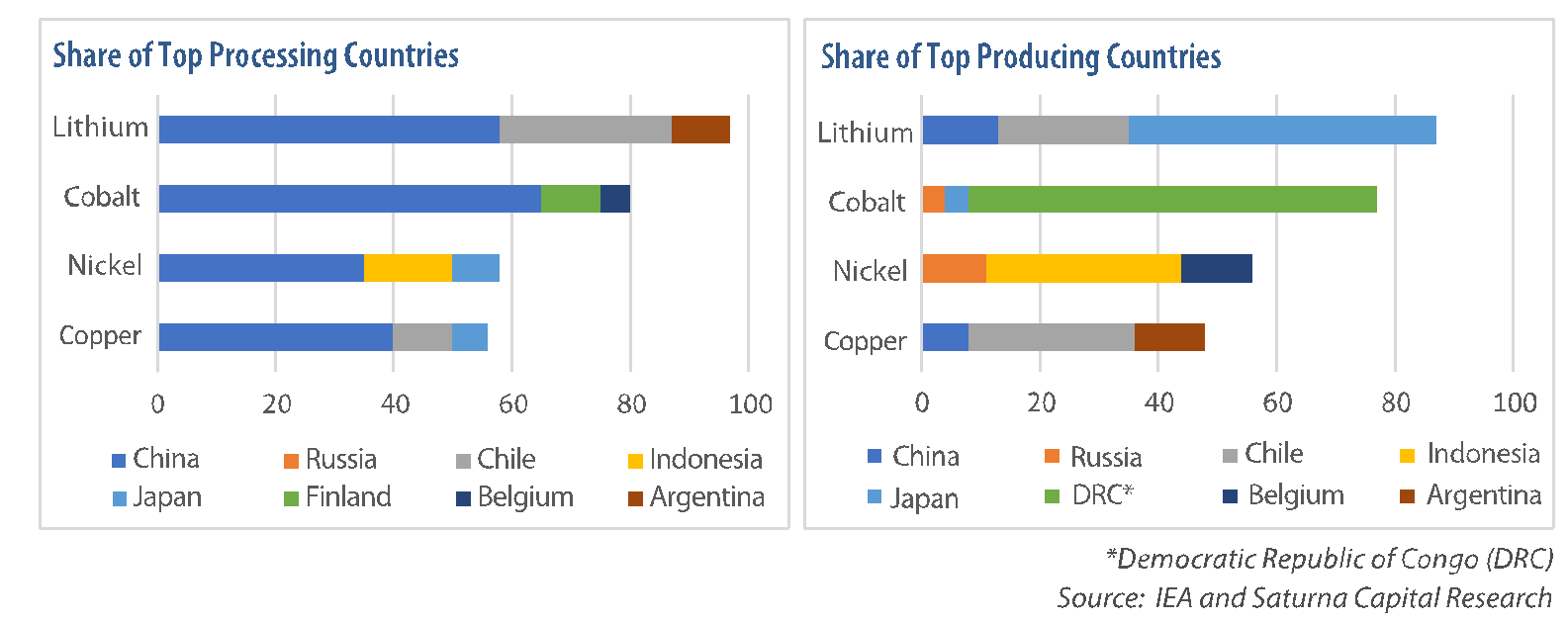

Copper has the largest market across green materials, but lithium, cobalt, and graphite are expected to experience the fastest growth in the coming decades. Cobalt is expensive, and much of its supply is concentrated in Democratic Republic of the Congo and Russia, leading many manufacturers to seek alternatives such as nickel. Similarly, graphene and silicon can serve as substitutes for graphite.

A variety of alternative sourcing methods is actively being pursued as battery developers work to increase electric vehicle range and lower charging times.

Most green elements, except for copper, had less prior industrial use and, until recently, have lacked adequate investment. The torrid uptick in renewable energy projects and EV demand exposed volatility in smaller, more nascent commodity markets.

Here, the old commodity adage, “the cure for high prices is high prices” held once again. As the adage implies, the rapid increase in lithium, nickel, and cobalt prices from 2020 to 2022 spurred a rapid increase in production. The production ramp up in turn caused prices to plummet in 2023.

To date, high demand, and prices, for green metals have been met with expanded supply and materials substitution. What’s yet to be seen, but likely coming down the pike, is technologic improvements to mining and material processing.

Direct lithium extraction, or DLE, for example, is one such advancement that stands to increase lithium yields while decreasing environmental effects of mining. Current extraction methods recover only 40% to 50% of the lithium in a brine. DLE has the potential to nearly double yields while reducing both the land and water use associated with current techniques, an important consideration as most brine resources lie in water-stressed regions.

Geopolitical Risks

Where does this modern gold rush lead? There is tremendous geopolitical risk tied to the green metals surge, with countries vying for supply supremacy.

Regions that feature poor governance currently dominate the production and processing of green materials. Half of all production of green materials in 2040 is expected to occur in autocracies, according to The Economist. The concentration of resources in poorly governed countries makes understanding local and geopolitics fundamental to assessing investment opportunities.

Fortunately, reserves are more broadly distributed, with Australia standing out as a likely winner. Already the largest lithium producer, Australia is tied with Indonesia for the largest nickel reserves (22% of global reserves) and has 20% of global cobalt reserves.

Environmental and Social Risks

In addition to governance concerns, mining presents an environmental and social conundrum. The industry has long been shunned by sustainability-focused investors for its negative effects on employees, local societies, and environments.

But how do we address climate change without mining? The mining sector produces 4% to 7% of global greenhouse gas emissions, underscoring the paradox.

Water use presents another major environmental risk, especially in drought-prone regions. While metals mining is far less water-intensive than fossil fuel production, water scarcity remains an important consideration. More than half of the world’s lithium and copper production occurs in areas with “high water stress.” A battle is also brewing over deep sea mining for critical minerals, which scientists warn could harm sealife.

On the positive side, metals and minerals essential to the energy transition can be recycled, unlike fossil fuels.

Mining presents a case study for why ESG considerations matter. Along with its effects on local environments, mining has a history of social challenges. All companies must uphold a social license to operate. But with governments often granting miners leases to public lands, the need to maintain this license is fundamental to the industry.

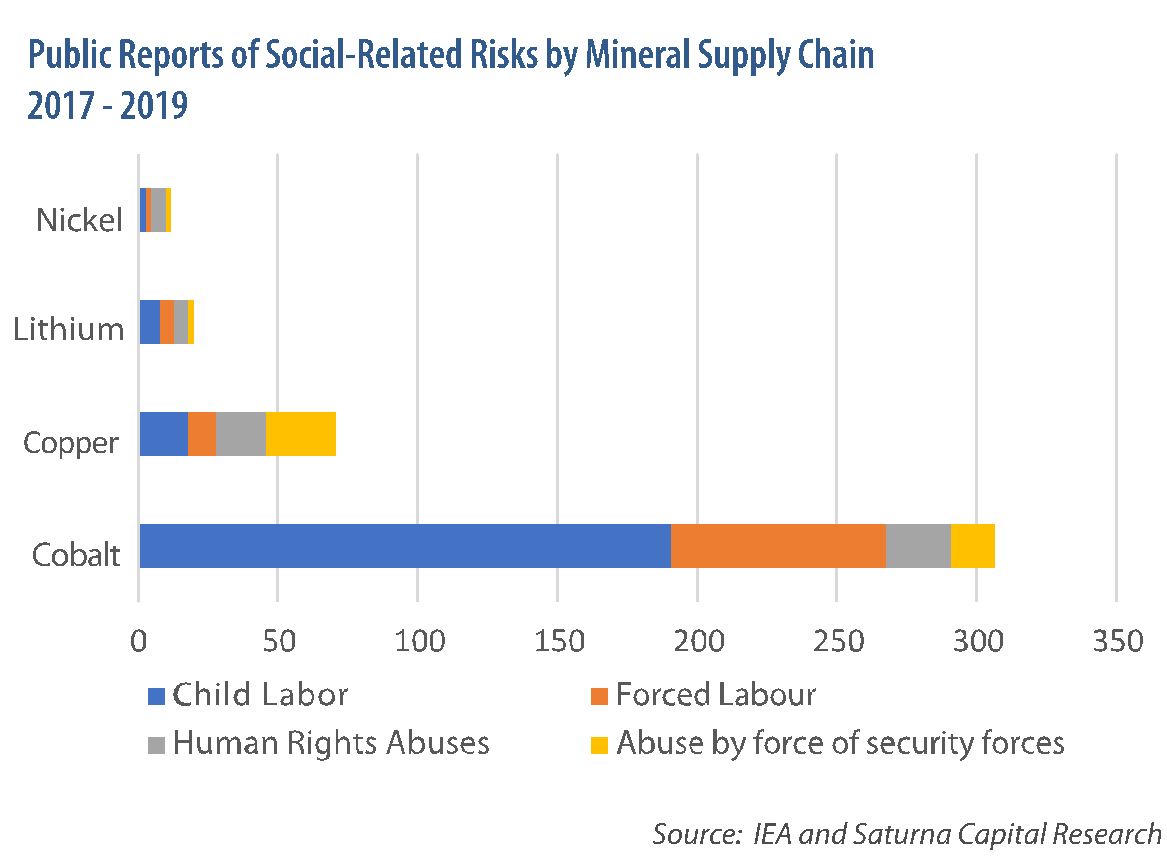

As shown in the IEA’s “Public reports of social-related risks by mineral supply chain, 2017-2019,” social risks vary widely by material. But cobalt stands out for its heightened exposure. Mining in Democratic Republic of the Congo is rife with reports of forced labor and toxic runoff. Copper, a market many times larger than the other green elements, also has a high incidence of governance risks.

Over the past five years, miners have increased their efforts to address ESG concerns, with many discussing strategies and performance on quarterly and semi-annual earnings calls.

In this critical era of transformation, we are pivoting from fossil fuels to a materials-based, low-carbon economy. While the path is strewn with financial, environmental, and ethical obstacles, the surge in ‘green’ materials presents an unprecedented opportunity. To ensure a future that is both sustainable and equitable, meticulous ESG oversight and innovative sourcing are key.

The challenge ahead demands concerted global effort, transparency, and a commitment to environmental stewardship and human rights. Embracing these principles will not only steer us towards net-zero emissions but also towards a more just and responsible mining sector.

____________________

Levi Zurbrugg is a senior analyst at Saturna Capital, a Bellingham, Washington-based investment advisor.