If the impact investing market is only 10% as large as it’s likely to be in 10 years, then 90% of the action is yet to come.

Impact investors to date have been remarkably satisfied. At least 88% of respondents to the annual survey by the Global Impact Investing Network report that their impact investments have met financial expectations. Fully 99% say the same about impact expectations.

From a high-water mark of 99%, there’s only one way to go: down. Impact investing therefore sits at a critical juncture. Financial performance will ebb and flow, as in any market. The greater risk is to impact.

How best to influence the integrity and impact performance of such future investments?

The answer starts with fund formation, where the first steps are taken to develop new investment solutions, long before capital is put to work.

The formation of a fund is the crucible of impact investing, where a clear market opportunity meets a great team and a receptive investor base (at least in theory). The challenge is that a great many stars need to align for a fund to be brought to life, which is why the process can be so difficult, as Tideline has shared previously.

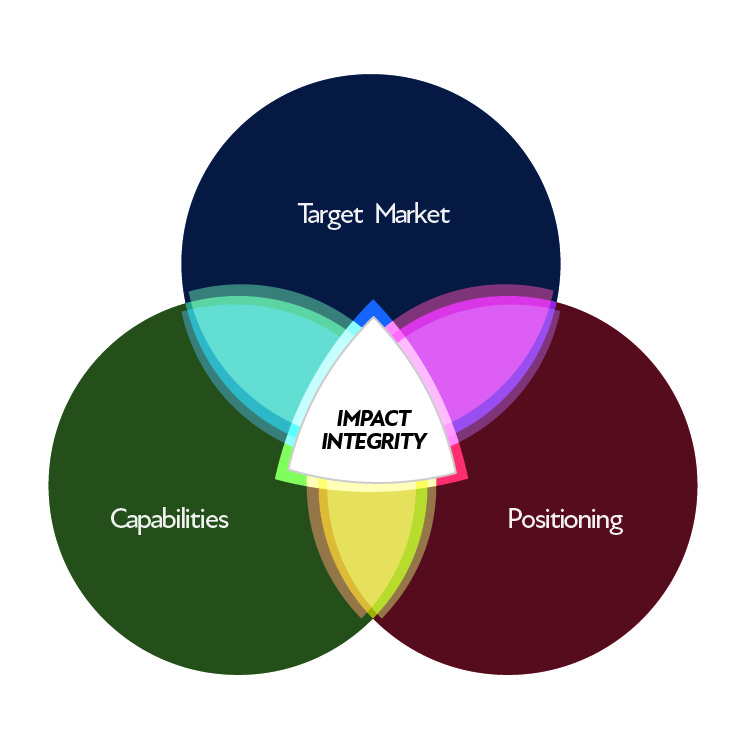

Sweet spot

Each fund-formation process features three key pillars that are essential to maintaining impact integrity: identifying the impact characteristics of the target market in which a fund is investing; developing the capabilities of the investor to deliver and demonstrate impact; and choosing the positioning of the fund.

When all three pillars are aligned, investors have hit the impact integrity sweet spot. When they are not, investors will be at an increased risk of impact-washing. By using these pillars as a design and assessment framework, future investments will be more likely to meet impact expectations.

Target market. The first pillar describes the impact outcomes that are possible through a particular investment opportunity and strategy. Depending on a myriad of factors, investors will be constrained in how much impact they and their investees can realistically deliver, whether they like it or not. These limiting factors include asset class, investee type, stage and amount of investment, structure and share of ownership, risk and return expectations, sector, geography, policy environment, and the list goes on.

An investor must understand exactly what type of impact the target market enables, and over what time period. There are many tools available to help make such an assessment, most notably the Impact Management Project (IMP) and its five dimensions. Consistent with the IMP framework, investors should ask themselves the following questions:

- What positive and negative effects can investees generate in this market?

- What are the additive contributions to impact we can make as an investor?

Capabilities. The second pillar describes the investor’s skill, experience, and track record in managing for net positive social and environmental outcomes. These capabilities include an investor’s ability to articulate a robust impact thesis, and then to screen, diligence, plan, optimize, monitor, and report against transparent impact objectives.

Here the market is also becoming increasingly institutionalized and investors should look to emerging standards for guidance, most notably the Operating Principles for Impact Management, where Tideline plays an active role as an independent verifier. Key questions include:

- Is optimizing for net positive social or environmental outcomes in this market part of our DNA as an investor?

- Do we have (or have access to) the skills and internal buy-in needed to rigorously measure and manage impact?

Global investment firms adopt IFC principles seeking a market standard for impact investing

Positioning. The final pillar is about truth in labeling. To be sure – and this is a critical point — there are no “right” approaches to having impact. The Impact Management Project has done a tremendous service by establishing that impact can be created along a continuum, including by avoiding harm (A), benefiting stakeholders (B), or contributing to solutions (C). Whether a fund avoids, benefits, or contributes, appropriate positioning means communicating its place on the continuum with clarity and precision.

This can be challenging given there is less guidance for investors (notwithstanding the new EU taxonomy). On one hand a more inclusive and mainstream understanding of “sustainable investing” has helped fuel market growth. On the other hand, a narrower definition of the specific term “impact investing” has emerged, setting a higher bar than many investors might realize, with large doses of intentionally, investor contribution, and measurement.

Impact integrity hinges on the willingness and ability of investors to properly self-identify, consistent with their target market and capabilities. IMP’s impact classes – building on Tideline’s earlier work – and the new IMP+ACT Alliance are emerging as helpful resources. Investors should ask:

- Does the name and description of our investment strategy imply a focus on screening, ESG integration, sustainable themes, or impact (i.e., the Impact Management Project’s ABCs)?

- Should we position what we do as laser-focused on one of these approaches, or as a more diversified strategy?

What could go wrong?

The fund formation framework also provides insight into what can go wrong. For example:

-

- When an investor knows the limitations of their own target market (check);

- and has the capabilities to deliver on the market’s modest impact potential (check);

- yet mislabels a fund, by characterizing it as more deeply impactful that it actually is (fail)…

Then, there will be an increased risk of impact-washing (defined as knowingly promising and claiming credit for more impact than it’s possible to deliver).

-

- When an investor inaccurately overestimates the impact potential of a target market (fail);

- but does a great job managing for the impact that’s actually possible (check);

- and positions the fund in accordance with their naively optimistic market assessment (check)…

Then, the risk is more about underperformance than impact-washing. Given the impossibility of generating the promised social and environmental outcomes, funders and beneficiaries are likely to be left disappointed.

-

- When an investor knows their target market (check);

- and labels their fund accordingly (check);

- but lacks the capabilities to provide evidence of impact (fail)…

Then, the investor risks patronizing its funders and beneficiaries, by forcing them to blindly trust that impact is being delivered as promised, without the necessary proof or verification.

Getting to alignment on all three pillars of fund formation is no easy task. Knowing a target market’s impact characteristics, having the capabilities to manage for impact and positioning a fund in a way that clearly conveys what the strategy is and what it isn’t requires deep analysis, introspection, and humility.

By doing the work even before capital is deployed, we can have greater confidence that future investments will help deepen and not diminish the integrity of the impact investing market.

Ben Thornley is a managing partner at Tideline and leads the firm’s work in strategy design and impact management.