ImpactAlpha, Oct. 21 – Embattled World Bank chief David Malpass made an about-face last week, copping to manmade global warming and the need to fund global climate action at the bank’s annual meetings that wrapped up Tuesday. The Trump appointee, who has come under withering criticism for his earlier refusal to acknowledge climate change and for the bank’s underwhelming climate response, may have been trying to save his job.

But the dust up underscores a deeper truth: development finance, from the World Bank and International Monetary Fund down to the regional development banks, are not meeting the complex, intertwined challenges of the 21st century, marked by a rapidly changing climate and cascading food and energy crises sparked by a new war on European soil.

The question is how to reform and scale up the banks’ work and mobilize private capital.

A recent report from an independent G20 panel identified a number of strategic opportunities for multilateral development banks, or MDBs, to usher additional capital to low and middle-income countries, including a reframing of investment risk assessment and flexibility for financial innovation in these markets.

U.S. Treasury chief Janet Yellen has called for “changes to incentives, operating models, and uses” of MDBs, and for the World Bank to develop an “evolution roadmap” by December.

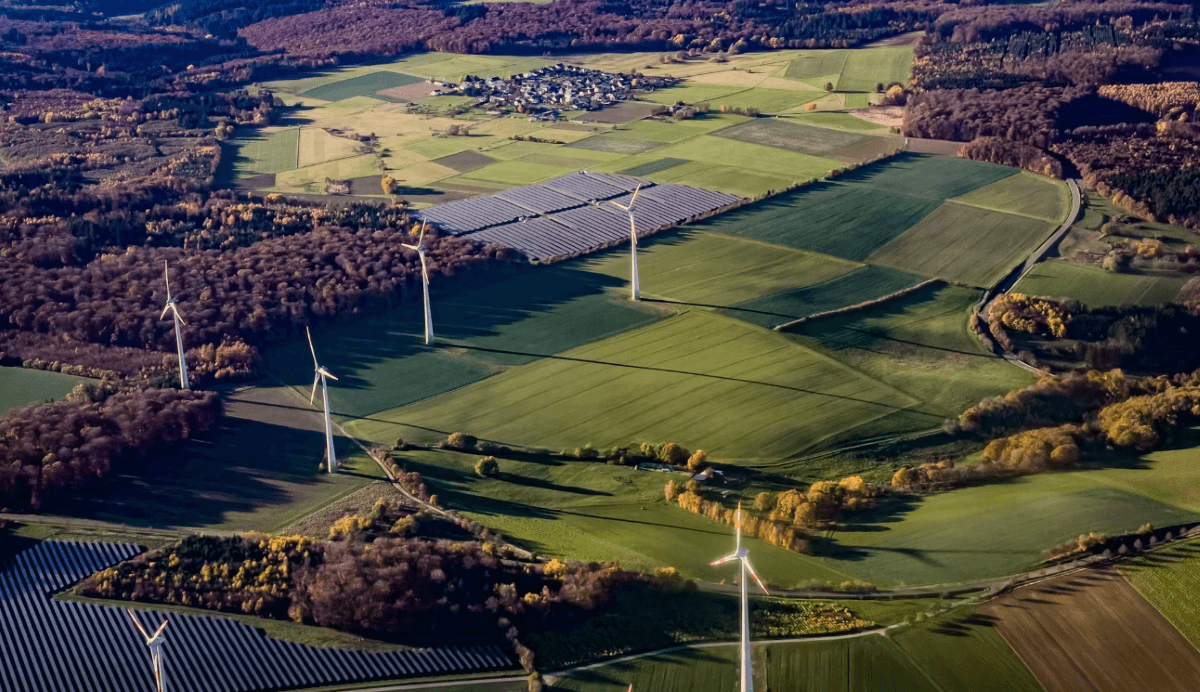

One model: The Just Energy Transition Partnership being developed by G7 nations to align domestic, public, private, and philanthropic resources in support of the fight against climate change.

Funding resilience

Barbados Prime Minister Mia Mottley has emerged as a strong voice calling for a transformation of Bretton Woods-era institutions and an acknowledgment of their role in indebting developing nations at the front lines of climate change. Mottley’s “Bridgetown Agenda” urges longer term concessional financing, a $1 trillion increase in MDB lending capacity for climate resilience, and the mobilization of up to $4 trillion for climate mitigation and adaptation for developing nations.

Nearly 60% of the poorest countries were already in or at high risk of debt distress before Russia invaded Ukraine, according to the World Bank’s own estimates. Its latest world economic outlook predicts a broad deceleration in economic growth.

“The time is now for much more ambitious and creative financing from the World Bank and the entire MDB system to support global economic resilience in the face of compounding health, food, fuel, and climate crises,” said The Rockefeller Foundation’s Mike Muldoon, in announcing a new grant fund aimed at addressing the disconnect.

The foundation, along with The Bill & Melinda Gates Foundation and Open Society Foundations, has launched the MDB Challenge Fund with an initial $5.3 million to prod global development banks institutions into increasing their funding and impact.

The fund will solicit proposals for technical assistance, operational funding and policy analysis to support innovative reforms that can scale development finance lending.

Yet another proposal came from a group of organizations including NRDC and the research group E3G. Among other things, they call for shifting the billions of dollars that the World Bank invests in fossil fuel projects towards climate mitigation and adaptation.

“The World Bank is in a position to ease suffering and create opportunity – but only if it ramps up its climate action,” said NRDC’ Jake Schmidt. The bank, he added, “could unleash tens of billions of dollars each year, if it moved more assertively to finance projects addressing climate change.” Instead, it “is sitting on capital that could make a real difference in people’s lives and livelihoods.”

Signs of change

“Dealing with the climate crisis is a huge public good,” the IMF’s Kristalina Georgieva said at the IMF’s annual meeting in Washington, D.C. “We should not shy away from thinking about how we use public money to remove obstacles for private money to move on the scale and in the time frame that is necessary.”

The framing of tackling climate change as a “public good” is a new development for the international financial organizations. “Using targeted lending to leverage private finance and going into the areas that the private finance won’t – to de-risk it to bring in larger institutional capital – is something I’ve heard over and over again this week, but not before,” Danny Scull of climate change think tank E3G told ImpactAlpha.

The IMF earlier this year stood up a $45 billion trust to provide affordable, long-term financing to improve climate resilience in emerging and frontier economies. The facility aims to be catalytic by requiring recipient countries to source additional financing and support from other backers.

Barbados and Costa Rica will likely be the first beneficiaries of the the Resilience and Sustainability Trust and are slated to receive more than $350 million combined. However, the IMF’s stringent conditions for accessing funds through the program could present obstacles for many low-income or distressed nations.

Achieving the climate goals set under the Paris agreement will require an investment of $3 trillion to $6 trillion a year, which means scaling funding by 5-10x. “If we do not shift our trajectory this decade,” said the IMF’s Georgieva, “we are cooked.”

Simon Stiell of the UN Framework Convention on Climate Change, speaking at the same event as Georgieva, expressed frustration with global leadership. “We’ll sit in these plenary and breakout sessions for the next two weeks negotiating at an incremental pace, when…the crisis that we face is exponential. It just isn’t enough. And it just isn’t fast enough – we are running out of time.”

Dan Keeler contributed reporting to this article.