Editor’s Note: Community Finance Brief is a newsletter from Matt Posner of Court Street Group, occasionally syndicated on ImpactAlpha.

In the fight against climate change, innovative financial models will be critical to success. The Environmental Protection Agency’s (EPA) Greenhouse Gas Reduction Fund (GGRF) envisions a new ecosystem of green lenders across the country that, if communicated properly, could look to public finance markets for guidance. As an infrastructure portfolio manager said recently in a conversation when GGRF came up, “What is the use of a fleet of electric buses if they have no roads to drive on?”

The answer, from a public finance mindset, is to design financing structures that help green our existing infrastructure so that electric buses, for example, can improve the operational efficiency of public transit in the US.

As public finance market participants for nearly two decades, we are both apt to make light of the opaque nature of the marketplace and its tendency to be an afterthought when it comes to major policy for the country.

With the GGRF, the Biden Administration has focused on creating leverage, and could likely end up leaning heavily on traditional US public finance markets and activities. It is time to lead this effort, not wait for it to come to the doorsteps of state and local governments nationwide.

State-level lenders

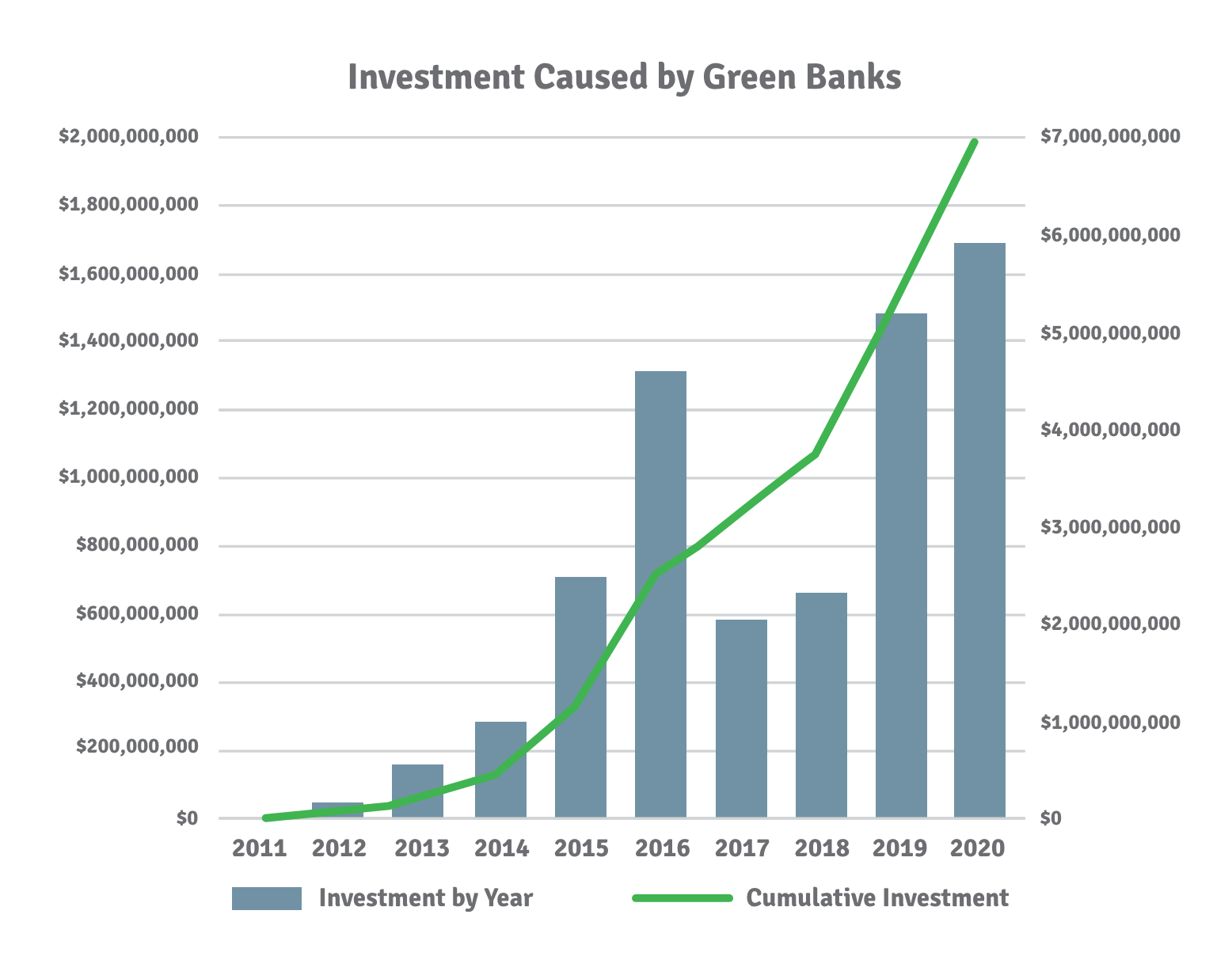

In the last few years, an entirely new ecosystem of lenders have emerged across the country. Green banks and infrastructure banks have been codified by state legislatures at a quicker clip than ever before. There were green/infrastructure banks operating in 26 states as of 2021, with more in the works (see chart, below). That’s up from zero in 2009.

As a result, we now have state-level, legislatively-codified lenders in over half of US states and territories. Their mandates vary, but in nearly all cases they are prepared to engage in the GGRF in different capacities. Some of these entities have experience in public finance but most are freshly minted, smaller in size and with minimal experience in what is required to be active market participants.

The GGRF, to recap, is encouraging a coordination of local lenders and climate banks to originate loans to support qualifying projects that marry environmental stewardship with racial equity. The $27 billion allocated to the program is expected to be leveraged and recycled.

We believe securitizations will be critical to extending the impact of the program and in making a dent in the nation’s current carbon footprint. However, in some cases, the state-level apparatus has little experience in the process of securitization. Currently, there are no guardrails in place for future capitalization and it would seem prudent to think through what currently exists and how some innovative tweaks would fit extremely well into the GGRF vision and accommodate new and existing actors well.

The emerging model that looks to be best placed for GGRF involves leveraging pooled loan funds, a strategy that already happens to be gaining traction with municipal and state agencies as a means to fund initiatives aimed at reducing greenhouse gas emissions.

Historically, pooled loan funds have been utilized by municipal entities, such as state housing finance agencies, bond banks, and clean water State Revolving Funds (SRFs). These entities aggregate loans from multiple borrowers, creating a diversified pool that can enhance credit quality and reduce borrowing costs. By applying this model to greenhouse gas reduction initiatives, state and municipal entities can mobilize substantial financial resources to address climate change.

Pooled loan funds

State housing finance agencies have long used pooling to finance single-family and large-scale housing projects by bundling mortgages and selling bonds backed by these loans. Similarly, state bond banks consolidate loans for various municipal projects, improving market access for smaller entities that might otherwise struggle to secure financing. State clean water SRFs operate on a similar principle, funding water quality projects through pooled municipal loans. These frameworks provide a blueprint for financing greenhouse gas reduction initiatives.

The success of pooled loan funds hinges on the homogenization of credit risk. By standardizing underwriting criteria and pooling loans with similar risk profiles, these funds can mitigate individual borrower risks through diversification. This approach mirrors the model used by Government-Sponsored Enterprises (GSEs) in housing finance, such as the “DUS” (Delegated Underwriting and Servicing) system employed by Fannie Mae, which allows more precise risk assessment and management.

Credit enhancement techniques, vital in these models, include over-collateralization, subordination, reserve funds, and insurance mechanisms, which collectively buffer investors from potential defaults. These strategies are integral in appealing to a broader range of investors, particularly when dealing with projects aimed at environmental sustainability, which may carry unique risks and longer payback periods.

One of the challenges in funding greenhouse gas reduction projects is the often small scale of individual loans, which may not be cost-effective to process individually. Here, the seller services model, akin to loan servicing in the mortgage industry, plays a crucial role. By pooling small loans and servicing them collectively, efficiencies are gained that reduce overall costs and simplify the funding process for small-scale projects.

Pooling loans for climate projects

To meet the ambitious goals of greenhouse gas reduction, innovative financing models can be adapted from established municipal finance systems in the United States. Pooled loan funds, which have proven effective in sectors such as housing and infrastructure, are a viable model for financing environmentally focused projects. Each of the following implementation models are widely used and trusted in US public finance and will be expected to extend into GGRF because of their approach to risk, pooling options and ability to lever.

Connecting the dots:

- State housing finance agencies (HFAs): These agencies have traditionally used pooled loan funds to issue mortgage revenue bonds that finance affordable housing. For instance, MassHousing, Massachusetts’ quasi-public housing finance agency, has issued multi-million-dollar bonds backed by pools of single family and multifamily mortgages. MassHousing also includes the Massachusetts Community Climate Bank, a new green bank focused on decarbonizing affordable housing. Housing bonds often feature leverage ratios of up to 10:1, allowing the agency to amplify its lending capacity significantly.

- State bond banks: Often utilized by smaller municipalities, state bond banks consolidate loans for a variety of local projects and generally pool them under a state-level entity, from public facility upgrades to infrastructure repairs. The Maine Municipal Bond Bank, for example, has issued bonds with a leverage ratio typically around 4:1, providing smaller entities with enhanced access to capital markets at competitive rates.

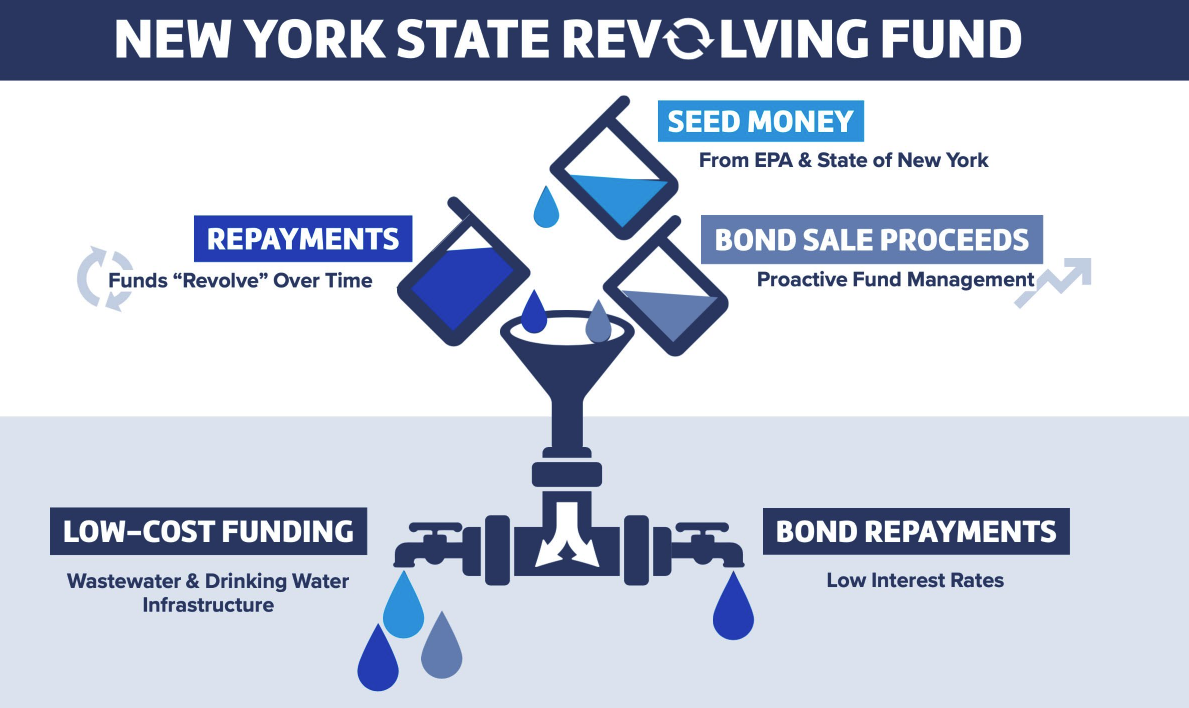

- State revolving funds, or SRFs (see image, below): These funds generally support water quality protection projects, including wastewater treatment and stormwater management, through low-interest loans to municipalities seeded with capital from the federal market and/or a state — which is very similar to GGRF. The California State Water Resources Control Board administers one of the largest SRFs, leveraging federal and state contributions to extend its reach. The leverage ratio here varies, but it can go as high as 20:1, depending on federal contributions and repayment terms.

Credit enhancement

Pooling loans requires rigorous risk modeling to ensure that the aggregated portfolio maintains a high credit quality. This is achieved by standardizing underwriting criteria across the pool, thus homogenizing the credit risk. Detailed statistical analysis and historical data are used to predict defaults and adjust the pool’s composition accordingly, balancing higher-risk loans with more secure ones to maintain an acceptable risk profile for investors.

To attract investment, particularly for projects with environmental goals that might carry higher perceived risks, credit enhancement is critical. Techniques include:

- Over-collateralization: Issuing bonds for less than the total value of the pooled loans.

- Subordination: Utilizing junior and senior tranches, where losses are first absorbed by junior tranches, protecting senior investors.

- Reserve funds: Setting aside cash reserves to cover potential loan defaults.

- Insurance: Purchasing bond insurance to cover losses, thereby improving the bond rating and reducing the cost of borrowing.

These enhancements help maintain investor confidence and stabilize the bond ratings, which are crucial for accessing lower-cost capital.

Scaling through seller services

The seller services model is particularly pertinent when managing numerous small loans, such as those for small-scale renewable energy installations or retrofits for energy efficiency. This model involves a third-party servicer handling loan administration duties, such as billing and collections, which reduces overhead costs and allows for the scalability of the program. By bundling these smaller loans, issuers can achieve economies of scale, making the financing of green initiatives more practical and appealing.

Perhaps the intersectionality will come at the state level with issuers that serve a dual function of climate and leveraged finance, like, for example, the Illinois Finance Authority, the California iBank, or MassHousing. All of these issuers have worked with pooled loan programs and will likely soon have leverageable dollars that can be used to de-risk lending structures. By working with partners on standardized program creation, and developing the lending ecosystem in state, these issuers can work with local lenders to create programs for origination.

For the local lenders, these bond programs create liquidity and ability to grow programs through the availability of scaled capital with hopefully better terms. In the case of these issuers, perhaps it is about greening existing models, not inventing new ones.

Call to action

By adapting the pooled loan fund model used in other municipal finance sectors to fund greenhouse gas reduction projects, the United States can harness the power of collective investment to drive meaningful environmental change. This approach not only capitalizes on proven financial mechanisms but also aligns with broader fiscal policies aimed at sustainability and environmental responsibility. This model’s scalability and adaptability make it an exemplary strategy in the global effort to combat climate change, providing a replicable framework for other nations as well.

As the urgency to address climate change intensifies, the adaptation of pooled loan funds for greenhouse gas reduction projects represents a strategic evolution in municipal finance. In the last 12 months engaging with GGRF awardees, the gaps of knowledge and connective tissue between experts in public finance, community development and commercial banks (not to mention the federal government) is glaring. GGRF faces an uphill battle on a lot of fronts. Engaging with public finance using these paradigms as a starting place will help.

Editor’s Note: Community Finance Brief is a newsletter from Matt Posner of Court Street Group, occasionally syndicated on ImpactAlpha.

Matt Posner is a principal at Court Street Group.

James McIntyre is an expert in municipal, affordable housing, and clean energy finance. The opinions expressed in his writing or any other media publication are his own and do not necessarily represent the views of his employer or any affiliated organizations.